Does data back higher for longer?

Key data to move markets today

EU: Speeches by ECB Vice President Boris Vujčić and German Bundesbank President Joachim Nagel

UK: Speeches by BoE Deputy Governor for Financial Stability Sarah Breeden and BoE External Member Swati Dhingra

USA: Michigan Consumer Expectations and Consumer Sentiment Indices, UoM 1- and 5-year Consumer Inflation Expectations and speeches by New York Fed President John Williams and Minneapolis Fed President Neel Kashkari

Global Macro Updates

US data supports resilience. US macroeconomic data presented a broadly resilient picture, with core PCE inflation matching expectations, personal spending and income exceeding forecasts, initial jobless claims declining, Q1 GDP revised higher and preliminary durable goods orders broadly in line with consensus.

Core PCE rose 0.3% month over month in May, in line with consensus and matching April’s increase. On an annualised basis, core PCE advanced 3.4%, slightly above the 3.3% consensus estimate and April’s 3.3% reading, reaching its highest level since October 2023.

Headline PCE increased 0.45% m/o/m, compared with expectations for a 0.5% rise and April’s 0.4% gain. The annualised headline measure rose to 4.1%, matching consensus and accelerating from 3.8% in April to its highest level since April 2023.

Household activity also showed strength. Personal spending increased 0.7% month over month, above the 0.6% consensus forecast and April’s 0.4% rise. Personal income also grew 0.7%, exceeding expectations for a 0.4% increase and improving from April’s flat reading.

Labour market data remained firm. Initial jobless claims fell to 215,000, below the 225,000 consensus estimate and the prior week’s upwardly revised 227,000, marking the lowest level since the end of May. Continuing claims totalled 1.821 million, above the 1.800 million consensus estimate and the prior week’s downwardly revised 1.800 million.

Growth figures were revised higher. The second estimate of Q1 GDP showed a 2.1% expansion, above both the 1.6% consensus forecast and the prior 1.6% estimate. The GDP chain price index was revised to 3.6%, slightly above expectations of 3.5% and the previous estimate of 3.5%.

Durable goods data was mixed, but contained encouraging underlying details. Preliminary headline orders declined 4.5% month over month in May, in line with consensus, while April’s headline figure was revised higher to an 8.5% gain from 7.9%. Core durable goods orders, defined as non-defence capital goods excluding aircraft, rose 1.6% m/o/m, well above expectations for a 0.6% increase and reversing April’s revised 0.7% decline.

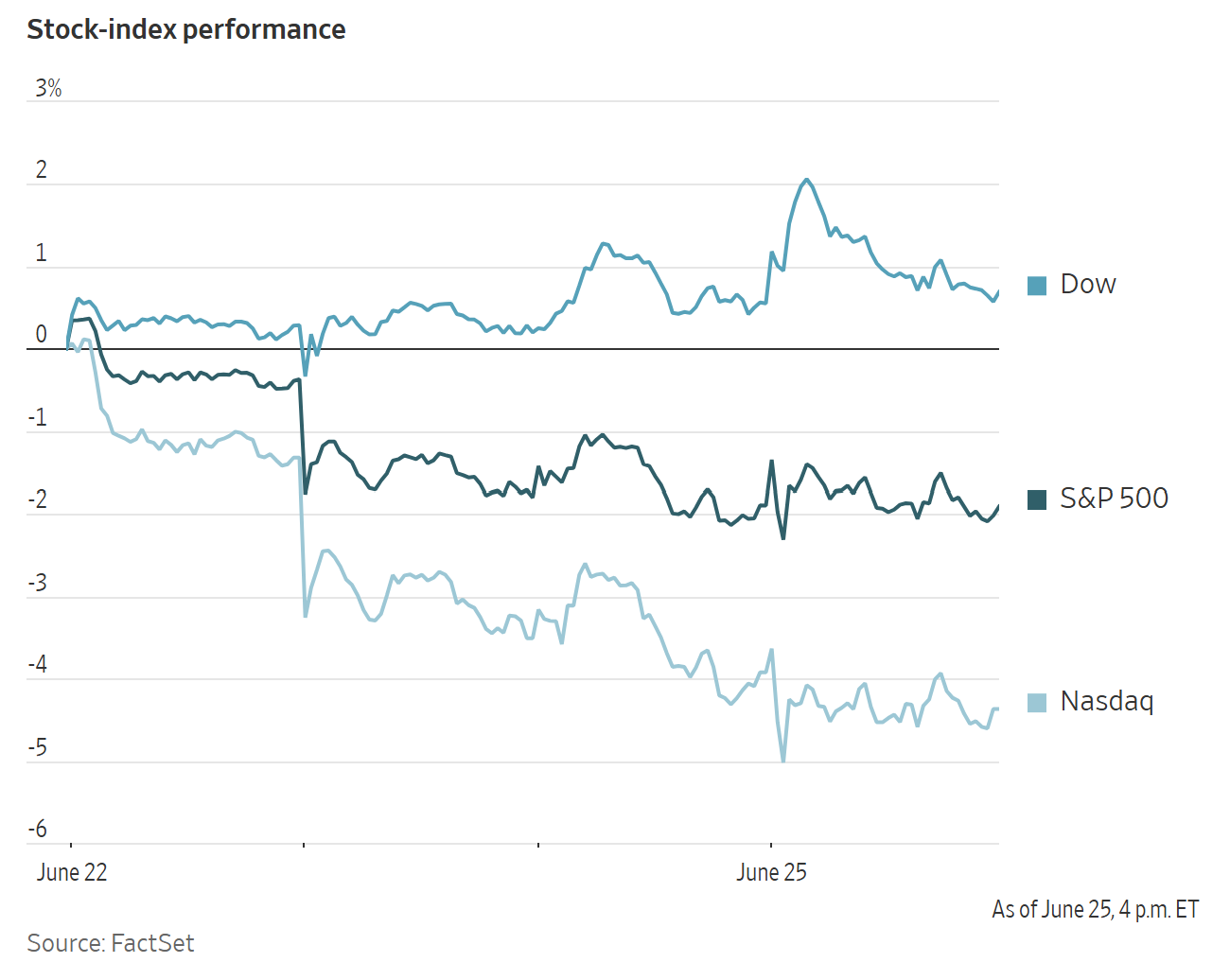

US Stock Indices

Dow Jones Industrial Average +0.14%

Nasdaq 100 +0.75%

S&P 500 -0.01%, with 5 of the 11 sectors of the S&P 500 down

Renewed volatility in technology shares offset broader signs of economic resilience on Wednesday. A selloff across megacap names weighed on the major benchmarks, even as strength in other areas of the market pointed to continued investor rotation.

The Nasdaq Composite declined -0.46%, while the S&P 500 slipped -0.01%. The Dow Jones Industrial Average proved more resilient, rising +0.14%, or 71.72 points.

All Magnificent Seven stocks ended lower, led by Apple. In contrast, the equal-weighted version of the S&P 500, which reduces the influence of the largest companies, advanced +0.67%, underscoring the rotation away from concentrated megacap leadership.

Corporate news added to the cautious tone. Microsoft announced a third significant price increase for its current-generation Xbox consoles, highlighting the impact of persistent component shortages and rising costs across consumer technology products.

Apple raised prices for Mac computers and iPads by 15% to 25% early Thursday, citing sharply higher memory and storage chip costs. According to TechInsights, prices for DRAM and NAND chips have quadrupled over the past 12 months amid strong demand from AI hyperscalers.

Strategy’s funding strain. Strategy, the Bitcoin-focussed company founded by Michael Saylor, closed at its lowest level in more than two years and was the weakest performer in the Nasdaq 100. The stock has now declined for seven consecutive sessions, its sharpest seven-day losing streak since the depths of the crypto downturn in November 2022.

Pressure on the company has intensified as Stretch, its largest dividend-paying preferred stock, slipped below its $100 par value and reached a record low this week. The steep discount limits Strategy’s ability to raise new preferred capital to fund additional Bitcoin purchases and may require the company to increase Stretch’s already elevated 11.5% annual dividend.

Investor concerns were further amplified by Strategy’s decision to use proceeds from common stock sales to purchase Bitcoin and reinforce its cash reserves. Although the move helps support preferred dividend obligations, it also dilutes common shareholders.

Retail traders target Wendy’s. Wendy’s also saw sharp intraday swings. Shares initially rose fifteen percent in what appeared to be a short squeeze, extending Wednesday’s +25.56% surge, before reversing course and closing down -6.80%.

The move echoed the retail-driven volatility seen in 2021, when online investors targeted heavily shorted stocks such as GameStop and AMC Entertainment, driving sharp rallies and pressuring hedge funds with short positions. According to Vanda Analytics, retail investors bought $15 million of Wendy’s shares on a net basis on Wednesday. That amount was roughly equivalent to their cumulative net purchases of the stock from the start of the year through the previous Friday.

Short sellers remained exposed to the move, with approximately 29% of Wendy’s float sold short at the end of May, according to FactSet. The abrupt rally likely forced some bearish investors to buy back shares in order to limit losses. The activity, which gained momentum on Reddit’s WallStreetBets forum, underscored that speculative enthusiasm remains active in parts of the market.

S&P 500 Best performing sector

Industrials +2.19%, with Caterpillar +6.29%, United Rentals +5.15% and Deere & Co +5.00%

S&P 500 Worst performing sector

Consumer Discretionary -1.78%, with TJX -6.04%, Ross Stores -5.89% and Expedia Group -4.27%

Mega Caps

Alphabet -0.82%, Amazon -3.14%, Apple -6.15%, Meta Platforms -2.68%, Microsoft -3.45%, Nvidia -1.59% and Tesla -0.09%

Information Technology

Best performer: Micron Technology +15.74%

Worst performer: Apple -6.15%

Materials and Mining

Best performer: Mosaic +4.17%

Worst performer: Albemarle -4.59%

European Stock Indices

CAC 40 +0.55%

DAX +1.03%

FTSE 100 +0.65%

Commodities

Gold spot +0.67% to $4,026.00 an ounce

Silver spot +0.75% to $57.87 an ounce

West Texas Intermediate +2.29% to $71.47 a barrel

Brent crude +2.09% to $74.69 a barrel

Gold reversed earlier losses on Thursday after the US May PCE report was broadly in line with expectations, easing concerns over near-term Fed tightening and weighing on both the US dollar and Treasury yields.

Spot gold rose +0.67% to $4,026.00 per ounce, recovering from an intraday decline of as much as 1%. The softer US dollar improved the relative appeal of dollar-priced bullion for overseas buyers.

The move followed Wednesday’s break below the $4,000-per-ounce threshold, the first such decline since November 2025. Spot silver also advanced, gaining +0.75% to $57.87 per ounce.

Oil prices rose more than two percent on Thursday as renewed security concerns around the Strait of Hormuz revived worries over global crude flows.

Brent futures gained $1.53, or +2.09%, to settle at $74.69 per barrel, while US WTI crude advanced $1.60, or +2.29%, to settle at $71.47.

The rally followed reports that several tankers initially bound for the strait reversed course after regional shipping threats, while additional support came from reports that a cargo vessel near Oman had been struck by an unknown projectile. Subsequent media reports cited US officials as saying the vessel had been attacked by the IRGC.

The rebound came after both crude benchmarks settled on Wednesday at their lowest levels since 27 February, after crude shipments through the strait rose to their highest point since the start of the war.

China showed limited urgency to absorb newly available oil cargoes. Bloomberg’s Javier Blas reported that several Chinese companies sold West African crude, with Angolan and Nigerian grades reaching their steepest discount to Dated Brent in 15 years.

Supply risks remained in focus after Ukraine struck two additional Russian refineries overnight.

Separately, Reuters reported that Iraq could consider all options, including leaving OPEC, if its production quota were not increased materially. Iraq’s Ministry of Oil later clarified that exiting OPEC was not the official position of the government, emphasising instead the need to reassess production baselines in line with members’ sustainable production capacity.

Note: As of 4 pm EDT 26 June 2026

Currencies

EUR +0.15% to $1.1372

GBP +0.30% to $1.3193

Bitcoin -1.10% to $60,124.24

Ethereum -2.02% to $1,578.55

The US dollar ended a three-session advance on Thursday after a series of US economic releases, including inflation data, reduced expectations for additional Fed rate hikes this year.

The dollar index fell -0.15% to 101.43, marking its largest daily percentage decline in two weeks. The euro gained +0.15% to $1.1372.

The decline interrupted a strong recent run for the greenback, which had risen in three consecutive sessions and five of the previous six, touching a 13-month high on Wednesday.

Sterling strengthened +0.30% to $1.3193, recovering after consecutive declines following Prime Minister Sir Keir Starmer’s resignation on Monday.

Against the Japanese yen, the US dollar was little changed at ¥161.76. BoJ board member Naoki Tamura said the central bank should raise interest rates every few months and remain prepared to accelerate the pace of tightening, citing inflation risks linked to the Middle East conflict.

At the same time, a draft of Japan’s long-term economic blueprint reviewed by Reuters indicated that the government would call for monetary policy that supports private demand, suggesting a preference for lower borrowing costs and the potential for policy tension with the central bank.

Fixed Income

US 10-year Bond +0.4 basis points to 4.395%

German 10-year Bund -0.5 basis points to 2.861%

UK 10-year Gilt +2.1 basis points to 4.706%

US Treasury yields were mixed on Thursday, with short-dated yields declining as Fed-sensitive rate expectations eased, while longer-dated yields finished modestly higher.

The Personal Consumption Expenditures Price Index (PCE), the Fed’s preferred inflation gauge, rose at a seasonally adjusted annual rate of 4.1% in May, the highest reading since April 2023. On a monthly basis, the index increased 0.4%, below economists’ expectations for a 0.5% gain.

Excluding food and energy, the core index rose 3.4% annually and 0.3% month over month, both in line with consensus forecasts.

The 2-year note yield, which typically tracks Fed funds rate expectations, fell -2.3 bps to 4.135%, its lowest level since 17 June.

The US 10-year yield edged +0.4 bps higher to 4.395%, although it earlier reached 4.363%, its lowest level since 8 May. The 30-year yield rose +2.5 bps to 4.865% after earlier falling to 4.823%, the lowest since 18 March.

The 2s10s spread steepened to 26.0 bps from 23.3 bps on Wednesday, even as the broader curve has flattened since the June FOMC meeting.

Auction demand was solid for the Treasury Department’s $44 billion sale of 7-year notes, the final offering in this week’s $183 billion slate of short- and intermediate-dated coupon-bearing debt.

The debt sold at a high yield of 4.26%, close to pre-auction trading levels, with a bid-to-cover ratio of 2.50x. Demand had been softer for Wednesday’s $70 billion sale of 5-year notes, while Tuesday’s $69 billion sale of 2-year notes drew solid interest.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 33.9 bps of rate hikes in 2026, lower than the 38.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 31.0% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 38.5% last week.

Eurozone bond yields were mixed on Thursday but remained near their lowest levels in more than three months.

Several ECB policymakers have pointed to the potential need for another rate increase to prevent higher energy costs from spreading into broader inflation. ECB board member Isabel Schnabel said the central bank would need to continue raising rates and that a Middle East ceasefire should not lead policymakers to lower their guard. Money markets have priced in 28 bps of additional ECB tightening this year, down from around 37 bps a week earlier.

Germany’s 2-year yield, which is more sensitive to rate expectations, fell -2.4 bps to 2.535%. Germany’s 10-year Bund yield slipped -0.5 bps to 2.861%. At the long end of the curve, the 30-year yield edged -0.9 bps lower to 3.404%.

Italy’s 10-year BTP yield rose +0.2 bps to 3.598%, leaving the spread over Bunds at 73.7 bps compared with 73.0 bps on Wednesday. France’s 10-year OAT yield was unchanged at 3.527%, leaving its spread over Bunds at 66.6 bps.

Note: As of 4 pm EDT 25 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.