Has business turned a corner?

Key data to move markets today

EU: German IFO Business Climate, Current Assessment and Expectations and a speech by ECB Executive Board Member Piero Cipollone

UK: Speeches by BoE Deputy Governor for Financial Stability Sarah Breeden and BoE External Member Swati Dhingra

USA: New Home Sales

Global Macro Updates

Eurozone PMIs show early stabilisation after year-long weakness. Eurozone private-sector contraction eased more than expected in June, with the S&P Global flash composite PMI rising to 49.5 from 48.5 in May, above the 49.2 consensus estimate. Although the index remained below the 50 threshold for a third consecutive month, the reading marked a three-month high and signalled a clear moderation in the pace of decline.

Over the past 12 months, the composite index has followed a downward trend, moving from expansion into sustained contraction, with the weakest readings concentrated between February and May. However, the past three releases suggest that the deterioration has stalled and may be approaching a trough.

Price pressures continued to moderate, as input-cost inflation fell to its weakest level since February and output-price growth eased to a three-month low. Supply-chain strains persisted, but became less severe. Employment recorded its smallest decline since February. Business confidence also improved for a second consecutive month, although it remained subdued by historical standards.

Germany remained the principal laggard, with its composite PMI falling to an 18-month low amid weaker services activity. Overall, the data still point to a subdued second quarter. It also indicates lower near-term inflation risks, reducing the likelihood of further aggressive ECB tightening.

UK PMI highlights services-led slowdown in activity. The UK flash PMI for June showed that weaker services-sector activity continued to weigh on overall output. The composite reading fell to a 14-month low of 49.4, below the 50.5 consensus estimate and the prior reading of 49.7. Services activity declined to a 41-month low of 48.7, compared with the 50.1 forecast and the previous 49.3 reading. Manufacturing was more resilient at 53. This still represented a three-month low and was below the 53.5 consensus and the prior 53.9 reading.

This was the second consecutive month in which activity contracted, with new business volumes declining at the fastest pace in 14 months and contributing to a sharper fall in backlogs of work. The downturn in services was attributed to domestic political uncertainty and the impact of the Middle East conflict. In manufacturing, expansion continued to rely partly on anecdotal reports of strategic stockpiling, which may fade after providing temporary support.

From a policy perspective, the data suggest that softer demand may be helping to contain inflationary pressures. Input prices remained elevated, but declined for a second consecutive month. Output prices eased somewhat as services providers cited strong competition and fee reductions. Manufacturing cost pressures were comparatively stronger. Employment trends diverged, with headcounts falling sharply in services, but rising in manufacturing.

Businesses were more optimistic about the outlook, with confidence supported by expectations for sales investment, activity in high-growth sectors, stronger capital inflows and reduced supply-disruption risks. Some firms also noted that pent-up demand could emerge if the Middle East conflict is fully resolved.

US Flash PMIs signal faster activity growth, but softer employment. US flash PMI data for June pointed to a further acceleration in business activity, although employment softened and price pressures remained elevated. The manufacturing PMI rose to 55.7, above the 54.2 consensus estimate and May’s 55.1 reading, marking its highest level since May 2022. The services PMI also improved, reaching 51.3, above the 51.2 consensus and May’s 50.7 reading. It is the strongest reading since February 2026.

The report indicated that US business activity growth accelerated for a third consecutive month, though it remained below levels seen earlier in the year. Employment declined for a second month as firms sought to control costs amid elevated input prices and broader economic uncertainty.

Supply-chain delays worsened in June, reflecting disruptions to Middle East shipping routes and the impact of tariffs. At the same time, input-cost inflation stayed high, while selling-price inflation remained at its strongest pace since July 2025. Services inflation also accelerated to an 11-month high.

Elsewhere, the June Richmond Fed Index declined to +4.0, below the +8.0 consensus estimate and May’s +13.0 reading, although the index remained positive for a fourth consecutive month.

New orders, shipments and employment all fell in June, although shipments and new orders remained in expansionary territory. Price pressures strengthened during the month, but firms continued to expect input-cost inflation to moderate over the next year.

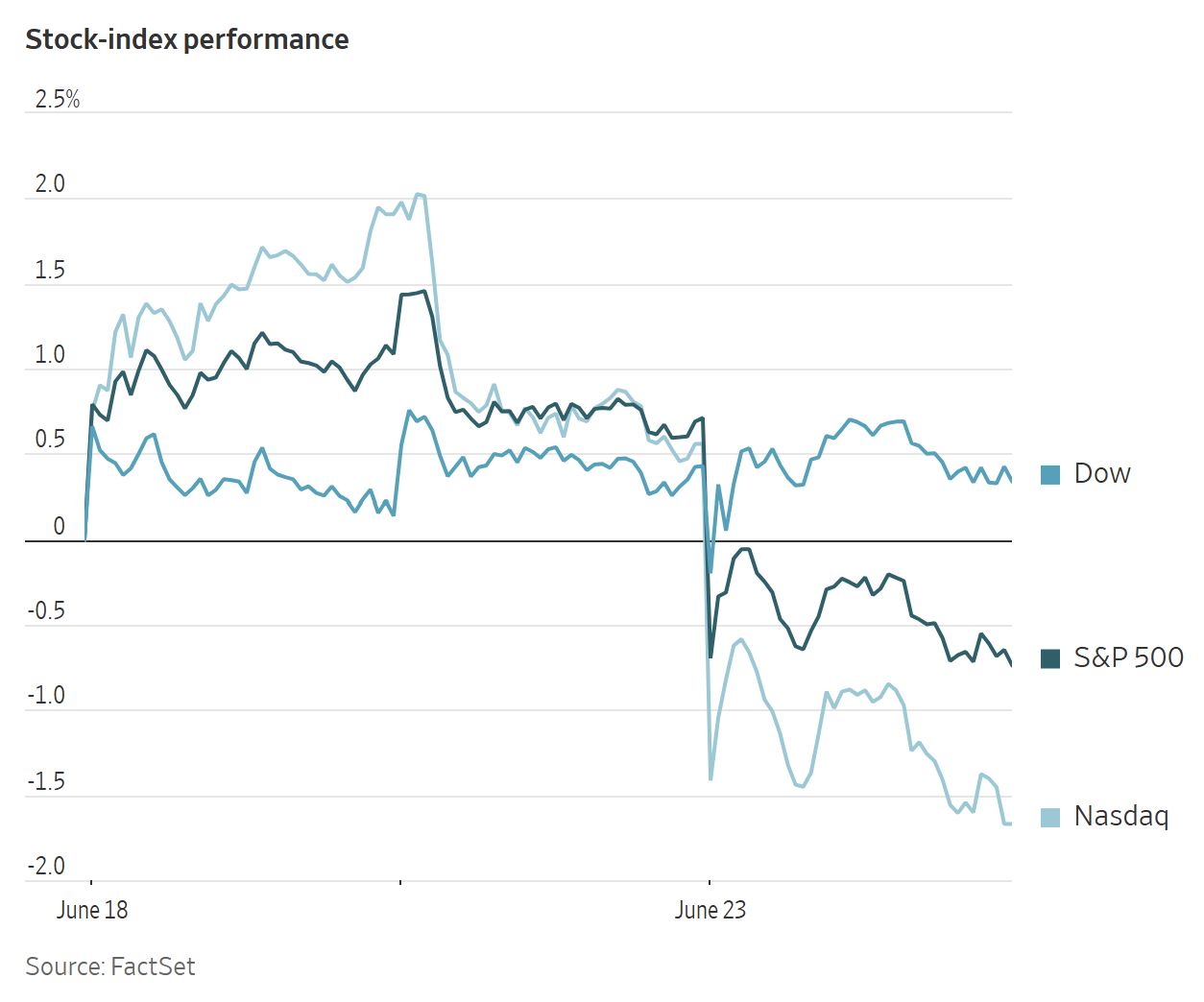

US Stock Indices

Dow Jones Industrial Average -0.09%

Nasdaq 100 -3.29%

S&P 500 -1.44%, with 5 of the 11 sectors of the S&P 500 down

US equities declined on Tuesday as selling pressure in technology shares intensified. The Nasdaq Composite fell -2.21%, while the S&P 500 lost -1.44%. The Dow Jones Industrial Average was comparatively more resilient, slipping -0.09%, or 45.87 points.

On Tuesday, stocks opened sharply lower, briefly stabilised and then retested their session lows during afternoon trading.

In corporate news, Alphabet is set to join the Dow Jones Industrial Average beginning Monday, according to index operator S&P Global. Alphabet will replace Verizon Communications, becoming the fifth Magnificent Seven company to enter the price-weighted index.

With its share price above $300, Alphabet will carry a significantly higher weighting in the index than Verizon, whose shares trade below $50. The other Magnificent Seven constituents already included in the Dow are Microsoft, Amazon, Apple and Nvidia.

Oracle disclosed that it reduced its workforce by 21,000 employees, or 13%, over the past fiscal year as part of an AI-focussed reorganisation.

According to The Wall Street Journal, SpaceX finalised terms for a $25 billion bond sale after holding investor calls, with proceeds expected to repay an earlier bank loan and support other spending needs. The offering is divided across five maturities and includes a $6 billion 10-year note priced at a 1.4 percentage-point spread over US Treasuries. Investor demand reached approximately $89 billion, making the deal one of the largest investment-grade transactions of the year.

Apollo Global Management is limiting withdrawal requests from Apollo Debt Solutions, its largest non-traded private credit fund, amid broader concerns about the asset class. The fund capped redemptions at 5% of outstanding shares after investors requested withdrawals totalling 16.8%, exceeding the level recorded in the prior period.

S&P 500 Best performing sector

Consumer Staples +1.78%, with Hershey +4.90%, Conagra Brands +4.51% and Campbell’s +3.97%

S&P 500 Worst performing sector

Information Technology -3.66%, with Micron Technology -13.18%, ON Semiconductor -11.01% and Enphase Energy -9.90%

Mega Caps

Alphabet -0.77%, Amazon +0.57%, Apple -0.91%, Meta Platforms -0.29%, Microsoft +1.80%, Nvidia -4.13% and Tesla -5.79%

Information Technology

Best performer: Intuit +0.11%

Worst performer: Micron Technology -13.18%

Materials and Mining

Best performer: Ball +3.93%

Worst performer: Freeport-McMoRan -6.95%

European Stock Indices

CAC 40 -0.71%

DAX -0.98%

FTSE 100 -0.09%

Commodities

Gold spot -1.96% to $4,108.35 an ounce

Silver spot -5.11% to $61.58 an ounce

West Texas Intermediate -1.72% to $73.05 a barrel

Brent crude -1.44% to $76.86 a barrel

Gold prices declined on Tuesday as the US dollar climbed to its highest level in more than a year, making the metal more expensive for overseas buyers.

Spot gold fell -1.96% to $4,108.35 per ounce, while spot silver dropped -5.11% to $61.58 per ounce.

Oil prices settled more than 1% lower on Tuesday as investors monitored crude flows through the Strait of Hormuz amid signs of progress in US - Iran peace talks.

Brent futures closed down $1.12, or -1.44%, at $76.86 per barrel, while US WTI futures declined $1.28, or -1.72%, to $73.05 per barrel. Both benchmarks touched near four-month lows during the session.

The downward trend followed Monday’s decline of more than two percent, after the US granted Iran a 60-day sanctions waiver following initial peace talks and officials reported a lull in hostilities in Lebanon under a broader agreement.

Oman and Iran agreed on Tuesday to continue discussions on the future administration of navigation in the Strait of Hormuz. US Secretary of State Marco Rubio said Iran would not be permitted to charge tolls in the key waterway under any final agreement with the US, arguing that such an arrangement would violate international law.

Investors are now assessing how quickly Middle Eastern producers can restore oil production and exports after wartime damage, as well as whether additional vessels will return to the region.

An Iranian military source told Fars news agency that a limited number of vessels are being permitted to pass through the strait each day under coordination with Iran’s Revolutionary Guards Navy.

Separately, ship-tracking data showed that three stranded supertankers passed through the strait on Tuesday, while seven empty Qatar-linked liquefied natural gas tankers have entered in recent weeks. The UN shipping agency said an evacuation plan is underway to allow hundreds of ships carrying 11,000 seafarers stranded in the Gulf to sail through the strait following the ceasefire deal.

Ship owners and operators will require assurances that mine-related threats have been fully eliminated. Damaged ports, debris in the water and congestion remain additional obstacles to an unconditional ramp-up in traffic.

Elsewhere, supply increases remained uneven. Saudi Arabia, OPEC’s top exporter, saw crude exports fall for a second consecutive month in April to a record low, according to data from the Joint Organizations Data Initiative.

Note: As of 4 pm EDT 23 June 2026

Currencies

EUR -0.39% to $1.1383

GBP -0.35% to $1.3199

Bitcoin -2.69% to $62,522.17

Ethereum -3.81% to $1,665.01

The US dollar advanced to its highest level in more than a year on Tuesday.

The dollar index rose +0.38% to 101.38 after reaching 101.42, its highest level since May 2025. The euro fell -0.39% to $1.1383 after touching $1.1374 earlier in the session, its lowest level since June 2025.

Sterling weakened -0.35% to $1.3199 as the UK government began its transition following the resignation of Prime Minister Keir Starmer.

Against the Japanese yen, the dollar was little changed, down -0.01% at ¥161.52. A move above ¥161.96 per dollar would take the yen to its weakest level since 1986.

Japanese Finance Minister Satsuki Katayama held an online meeting with US Treasury Secretary Scott Bessent late on Monday, a source told Reuters, as concerns over sharp currency swings intensified.

The discussion focussed on policy responses to the historically weak yen, potentially including currency intervention. Japanese financial authorities have kept markets uncertain about possible intervention, with the absence of clear signals suggesting a shift in communication tactics.

Fixed Income

US 10-year Bond -1.4 basis points to 4.502%

German 10-year Bund -3.6 basis points to 2.924%

UK 10-year Gilt -5.7 basis points to 4.759%

US Treasury yields declined on Tuesday, although short-dated yields remained near 16-month highs as traders continued to assess the prospect of a more hawkish Fed.

The 2-year note yield, which typically tracks Fed funds rate expectations, fell -3.2 bps to 4.207%. It reached 4.236% on Monday, its highest level since February 2025.

The yield on US 10-year notes declined -1.4 bps to 4.502%.

The yield curve between 2- and 10-year notes steepened by 1.8 bps to 29.5 bps, while the 30-year yield declined -0.2 bps to 4.948% at the long end of the curve.

The Treasury Department saw solid demand for a $69 billion auction of 2-year notes on Tuesday, the first sale in this week’s $183 billion offering of short- and intermediate-term coupon-bearing notes.

The notes sold at a high yield of 4.189%, the highest auction yield since January 2025 and less than 1 bp below the pre-auction trading level. The bid-to-cover ratio was above its recent average at 2.64x.

The US Treasury is also scheduled to sell $70 billion in 5-year notes today and $44 billion in 7-year notes tomorrow.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 38.2 bps of rate hikes in 2026, higher than the 19.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 37.4% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 8.5% last week.

Eurozone sovereign bond yields fell for a second consecutive day on Tuesday as investors pared expectations for further ECB rate increases.

The 2-year Schatz yield declined -2.8 bps on the day to 2.589%.

Germany sold €3.087 billion of 2-year Schatz debt on Tuesday at an average yield of 2.57%, the lowest level for this maturity since April, with a bid-to-cover ratio of 1.9x, the highest since January.

Money markets indicated that traders expect eurozone rates to end the year roughly 30 bps above current levels, with the next hike priced for October. Last week, markets had priced in two hikes.

The 10-year Bund yield fell -3.6 bps to 2.924%, while the Italian 10-year BTP yield declined -2.2 bps to 3.636%, leaving the spread over Bunds at 71.2 bps.

German 2-year bond prices rallied sharply in late trading on Monday, sending yields down by the most in two weeks, after ECB President Christine Lagarde told the European Parliament there was no evidence of an inflation pickup that would warrant more forceful policy action.

French 10-year OAT yields declined -3.2 bps to 3.568%, leaving the spread over Bunds at 64.4 bps.

Note: As of 4 pm EDT 23 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.