Is it getting safer or more dangerous for investors?

Global Macro Updates

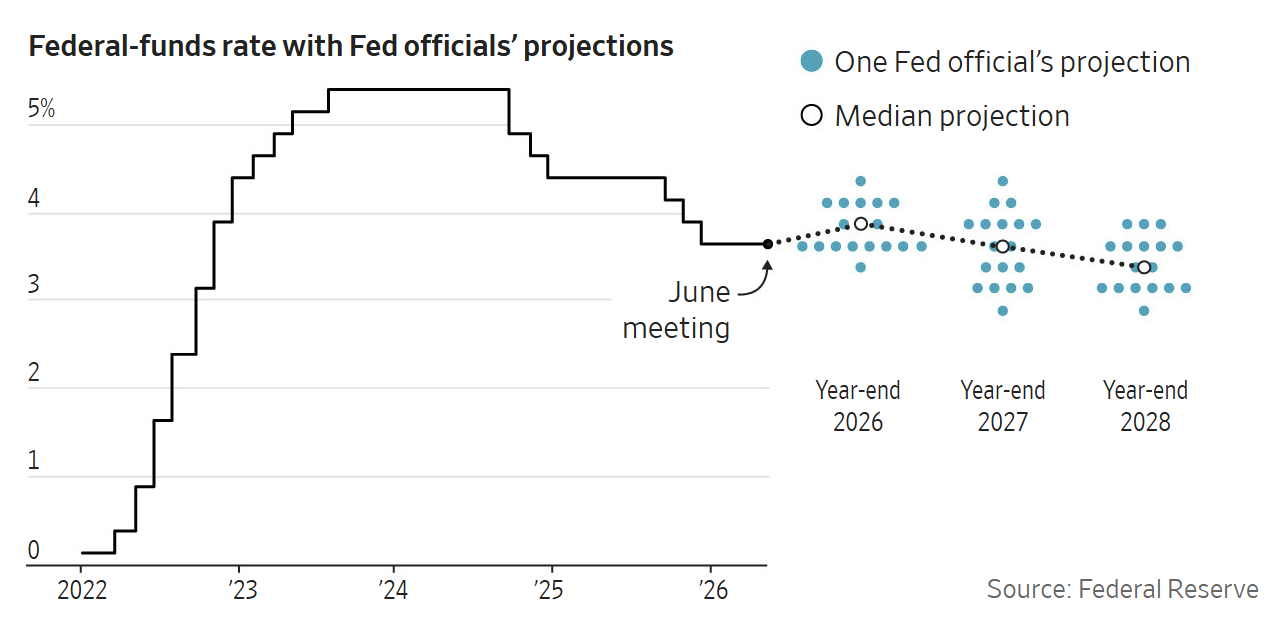

Warsh’s not so subtle moves. The June FOMC meeting concluded with the Fed holding rates steady at 3.50% – 3.75%, a decision in line with expectations, but accompanied by a statement far more consequential than its brevity suggested.

The Fed's updated Summary of Economic Projections revealed a committee in motion. The median dot now implies 12.5 basis points of additional tightening by year-end, a striking reversal from the 25 basis points of cuts projected as recently as March. Nine of eighteen participating officials are pencilling in at least one rate hike in 2026, six of them anticipating multiple, while only one forecasts a cut. Fed Chair Warsh himself declined to submit a projection.

The inflation outlook has deteriorated materially. Policymakers revised their 2026 headline PCE forecast to 3.6%, up sharply from 2.7% in March, with core PCE revised to an equally uncomfortable 3.3%. The drivers are familiar, but intensifying: an energy shock tied to the Iran conflict and a structural surge in demand fuelled by the AI boom have reignited price pressures that the committee had previously believed were fading. GDP growth was trimmed modestly to 2.2%, while the unemployment rate forecast was nudged lower to 4.3%, a labour market more resilient than officials had feared, and one that offers the Fed little cover to remain on hold.

What made the meeting notable was less the data and more the messenger. Warsh was President Trump's hand-picked choice, selected with the explicit expectation of a rate-cutting disposition. His debut press conference delivered the opposite signal. With a tone that carried a degree of confidence that some observers found striking given the considerable uncertainty still surrounding the outlook, Warsh declared that the Fed has ‘the capability and commitment to deliver on our price stability objective’, echoing his long-held view, repeated again on Wednesday, that inflation is a choice. The rhetoric, while resolute, sat uneasily alongside the committee's own acknowledgment of elevated uncertainty stemming from the Iran conflict.

Warsh also used the occasion to announce five independent task forces tasked with reviewing the Fed's communications strategy, balance sheet management and inflation framework, with most expected to report by year-end. Forward guidance, he stated, is no longer suited to the current policy environment. The scope of the initiative signals genuine institutional ambition. Yet the announcement raised as many questions as it answered: the membership of these task forces has not been disclosed, leaving markets and policymakers uncertain about whose analytical lens will shape the Fed's next chapter. This opacity, given the breadth of the review, warrants close attention in the weeks ahead.

Can Europe really protect itself from China? European Council leaders are meeting this evening and it appears that a definite item on the agenda will be whether to impose tariffs on China to protect EU industries. Europe’s trade deficit with China amounted to €360bn in 2025. The EU is China’s second-largest trading partner. As noted by Politico, EU trade chief Maroš Šefčovič said after a meeting of EU foreign ministers on Monday, that “Our trading relationship with China has reached a point that requires a reset — not confrontation but rebalancing. The status quo is not sustainable — not economically or politically.” In May EU Executive Vice-President for Prosperity and Industrial Strategy Stephane Sejourne said Brussels would broaden import quotas and tariffs against China to shield certain industrial sectors from an "existential" threat from Chinese imports. It is clear that the EU fears the dominance of Chinese companies in the automobile sector in terms of electric vehicles (EVs), in chemical production and in “green” technologies. Even Germany, previously hesitant to upset China, has, due to its sluggish growth due to a drop in industrial growth, particularly in the automobile sector, started to shift its position, leaving Spain as the last major opponent of a tougher EU trade policy toward China.

Last week French officials indicated that they hope the G7 summit will result in a plan to tackle that Chinese trade threat. Germany, Poland, the Netherlands, Belgium and others have, according to the Financial Times, backed a French proposal for new EU powers to impose tariffs swiftly on China, according to four EU diplomats. The European Commission is pursuing a twin-track strategy: intensifying dialogue with Beijing while signalling it’s ready to strike if needed. The EU’s existing anti-coercion instrument, which has never been used, is considered “difficult to implement”, and therefore a new trade defence tool may be needed. Possible measures could include the wider use of import quotas for industries hit hardest by Chinese competition. Another is a new “diversification instrument” that would require companies in sensitive industries to source inputs from at least three international suppliers so that companies would be shielded from general supply chain disruptions and government policies such as the export restrictions that China has imposed on certain rare earth metals. There are already EU policies encouraging companies to diversify if they relied on one source for 40% of certain supplies, but this is not enforced. An extreme measure would be, as noted by Politico, the creation of an “overcapacity instrument” that would effectively impose sweeping tariffs on Chinese products. However, such an instrument may come into conflict with existing World Trade Organization rules.

European Commission president Ursula von der Leyen is expected to open tonight’s dinner with a presentation on macroeconomic imbalances. However, given that internal EU consensus remains fractured due to fears that China may retaliate by imposing strict export controls on rare-earth elements and critical tech materials necessary for European industries, there will likely be limited immediate movement against China.

Global market indices

US Stock Indices Price Performance

Nasdaq 100 -2.18% MTD and +17.51% YTD

Dow Jones Industrial Average +1.90% MTD and +8.19% YTD

NYSE +0.76% MTD and +6.66% YTD

S&P 500 -2.11% MTD and +8.39% YTD

The S&P 500 is +2.11% over the past seven days, with 6 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is +1.15% over this past week and +8.72% YTD.

The S&P 500 Financials is the leading sector so far this month, +4.70% MTD and -1.61% YTD, while Consumer Discretionary is the weakest sector at -6.40% MTD and -2.78% YTD.

Over the past seven days, Industrials outperformed within the S&P 500 at +5.83%, followed by Materials and Information Technology at +5.13% and +3.71%, respectively. Conversely, Energy underperformed at -6.21%, followed by Real Estate and Consumer Staples at -2.38% and -2.10%, respectively.

The equal-weight version of the S&P 500 was -1.52% on Wednesday, underperforming its cap-weighted counterpart by 0.31 percentage points.

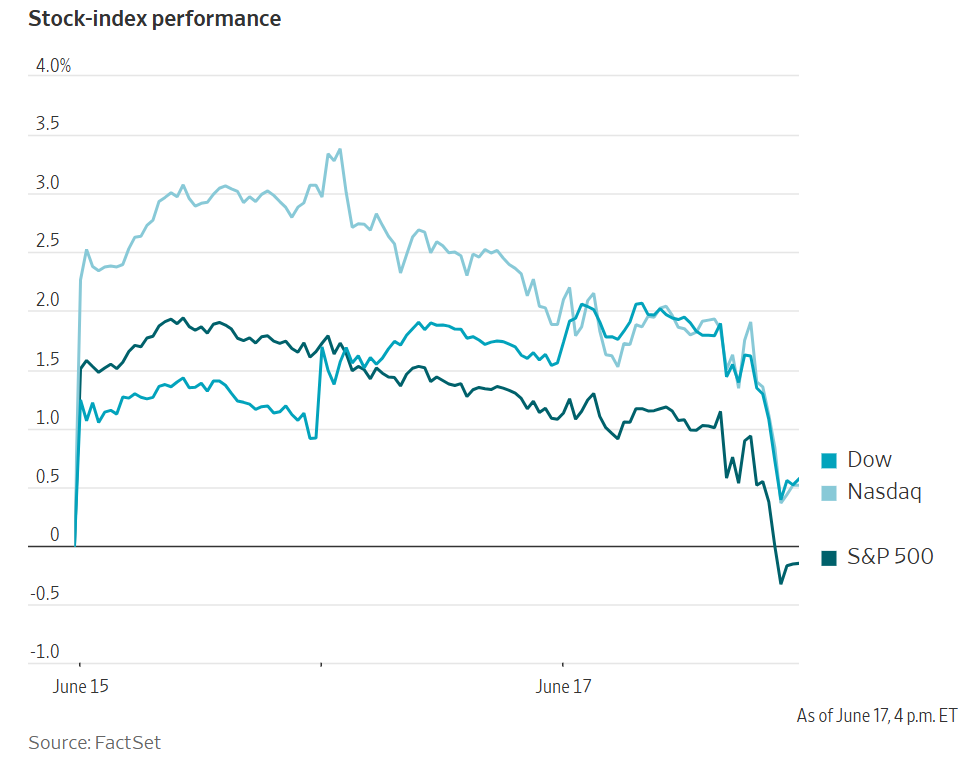

On Wednesday, the S&P 500 was -1.21%, or down 91.25 points, to 7,420.10. The Dow Jones Industrial Average was -0.98%, or down 507.12 points, to close at 51,492.55. The Nasdaq Composite was -1.34%, or down 354.69 points, to 26,021.66. Over the past seven days, the S&P 500 was +2.11%, the Dow Jones Industrial Average was +4.17% and the Nasdaq Composite was +3.39%.

In corporate news, Blue Origin has already begun rebuilding the Florida launch site where its New Glenn rocket exploded last month, paving the way for the company to resume flights later this year as it seeks to revive its challenge to SpaceX.

At CME Group, Chief Executive Officer Terry Duffy will step down on 1 March after more than 25 years leading the world’s largest derivatives exchange and will transition to the role of executive chairman. Chief Financial Officer Lynne Fitzpatrick will succeed him as CEO.

A potential merger between Tesla and SpaceX appears to be drawing nearer. Elon Musk increased his voting power at Tesla to nearly 20% by converting a portion of his stock options into shares that he can vote immediately but cannot sell until 2028.

Following last week’s SpaceX IPO, Musk executed an April agreement with Tesla to convert options on roughly 300 million shares that were granted under his 2018 compensation package, according to securities filings. Rather than receiving ordinary common stock, he was issued restricted shares that will vest on 19 January 2028, the date on which the options were originally due to expire.

The instruments, however, carry voting rights that may be exercised immediately, the filings stated. To fund the exercise, Musk surrendered 17.5 million shares to cover the approximately $7.1 billion cost. Following the transaction, he held about 700 million Tesla shares, including those owned through a trust, representing roughly 19.9% of the company’s outstanding stock. Musk has previously said that he would like to control 25% of Tesla in order to feel comfortable advancing the company’s artificial intelligence ambitions. His ownership stake in 2025 was about 15%.

Mega caps: The Magnificent Seven had a mixed performance over the past week. Over the last seven days, Tesla +3.88%, Nvidia +2.11%, Alphabet +2.08% and Apple +1.50%, while Amazon -0.21%, Meta Platforms -0.60% and Microsoft -4.64%.

Energy stocks had a negative performance this week. The Energy sector itself was -6.21%. WTI and Brent prices are -17.64% and -16.92%, respectively, over the past week. Over the last seven days, Energy Fuels +13.31%, while Baker Hughes -4.68%, Shell -6.30%, Chevron -6.44%, ExxonMobil -6.56%, BP -6.60%, Marathon Petroleum -7.09%, Occidental Petroleum -7.11%, ConocoPhillips -7.26%, Phillips 66 -8.01%, Halliburton -8.81% and APA -10.71%.

Materials and Mining stocks had mostly positive performance this week, with the Materials sector itself +5.13%. Over the past seven days, Newmont Corporation +13.91%, Mosaic +13.57%, Albemarle +13.14%, Sibanye Stillwater +11.88%, Freeport-McMoRan +11.24%, Celanese Corporation +1.69% and Nucor +0.84%, while CF Industries -3.12% and Yara International -3.34%.

European Stock Indices Price Performance

Stoxx 600 +2.13% MTD and +7.96% YTD

DAX -0.68% MTD and +1.81% YTD

CAC 40 +3.02% MTD and +3.45% YTD

IBEX 35 +5.77% MTD and +12.21% YTD

FTSE MIB +4.79% MTD and +16.66% YTD

FTSE 100 +0.95% MTD and +5.81% YTD

This week, the pan-European Stoxx Europe 600 index is +3.42%. It was +0.52% on Wednesday, closing at 639.31.

So far this month in the STOXX Europe 600, Banks is the leading sector +6.32% MTD and +12.50% YTD, while Autos & Parts is the weakest at -4.81% MTD and -14.39% YTD.

Over the past seven days, Banks outperformed within the STOXX Europe 600, at +10.19%, followed by Construction & Materials and Basic Resources at +6.82% and +6.15%, respectively. Conversely, Telecom underperformed at -2.59%, followed by Oil & Gas and Food & Beverages at -2.58% and -0.46%, respectively.

Germany's DAX index was +0.10% on Wednesday, closing at 24,934.67. It was +3.06% over the past seven days. France's CAC 40 index was -0.20% Wednesday, closing at 8,430.79. It is +3.30% over the past week.

The UK's FTSE 100 index was +2.47% over the past week to 10,508.61. It was +0.14% on Wednesday.

On Wednesday, European equities traded with a constructive tone, led by gains in technology, banking, retail and industrials, while autos, utilities, energy and basic resources lagged amid lower commodity prices and a rotation away from defensive sectors.

Technology was the strongest-performing sector as markets consolidated following the easing of Middle East tensions and the decline in oil prices. Sentiment was further supported by sustained investor focus on European technological sovereignty and AI investment themes. Among notable movers, AT&S advanced after finalising the terms of its €400 million deeply subordinated perpetual convertible bond, while Indra gained on reports that it is nearing an agreement with Rheinmetall and MAN relating to defence platforms.

Banks also outperformed, supported by an improved economic outlook following the regional de-escalation, which lifted risk appetite ahead of the FOMC decision. HSBC edged higher after announcing a multi-year AI partnership with Google Cloud and DeepMind to accelerate AI deployment across its operations. Industrial Goods & Services likewise traded higher, underpinned by continued strength in defence-related names. Leonardo rose after receiving conditional approval from the Italian government for its unmanned aerial vehicle joint venture with Turkey’s Baykar.

Retail were among the better performers, supported by corporate updates. AUTO1 Group shares traded higher after presenting long-term growth targets and reaffirming its FY 2026 guidance ahead of its capital markets day. Elsewhere in the sector, H&M declined after ABG Sundal Collier downgraded the stock to hold from buy, while AO World traded weaker despite reporting record profits and announcing additional shareholder returns.

Health care was supported by a sharp rally in Straumann Holding shares, which raised its FY26 margin expansion outlook, citing operational efficiencies, improving trends in China and stronger execution. By contrast, Autos & Parts was the weakest-performing segment after BMW issued a profit warning and lowered its automotive margin guidance, pointing to deteriorating conditions in China and the lingering effects of the Middle East conflict. The Financial Times also reported that Volkswagen is seeking sealed bids in the sale of Everllence.

Insurance and Telecom underperformed as investors rotated out of defensive sectors. Within Telecom, Orange declined after Barclays reinstated coverage with an equal-weight rating, noting that value creation from consolidation and acquisitions may take longer to materialise. Utilities, Basic Resources and Energy also lagged as oil and metal prices retreated, with expectations that a formal US - Iran peace signing on Friday will add further downward pressure to oil price forecasts.

Other Global Stock Indices Price Performance

MSCI World Index -0.43% MTD and +9.33% YTD

Hang Seng -3.46% MTD and -5.14% YTD

Over the past seven days, the MSCI World Index and Hang Seng Index are +3.43% and -0.39%, respectively.

Currencies

EUR -1.33% MTD and -2.06% YTD to $1.1503

GBP -1.29% MTD and -1.43% YTD to $1.3280

The US dollar strengthened against major currencies on Wednesday after the Fed left its benchmark rate unchanged while signalling that borrowing costs could rise later this year, reinforcing concerns that inflation risks remain elevated.

Against the dollar, the euro fell -0.89% to $1.1503, while the yen weakened modestly, leaving the greenback +0.10% higher on the day at ¥160.54. The dollar index rose +0.83% to 100.39. Over the past week, the dollar index is +0.34%. Against the greenback, the euro is -0.25% over the past seven days.

Over the past week, the dollar has strengthened +0.05% against the yen. Against the US dollar, the yen is -0.80% MTD and -2.48% YTD.

Sterling also came under pressure, falling -1.09% to $1.3280 after UK inflation data came in softer than expected and investors looked ahead to today’s BoE MPC meeting. Over the past week, the pound has declined -0.65% against the US dollar.

While the BoE is widely expected to leave rates unchanged, one or two of the nine policymakers, including Chief Economist Huw Pill, are expected to vote in favour of a rate increase. Markets are currently pricing in one additional 25 bps rate increase by the BoE this year.

Note: As of 5:00 pm EDT 17 June 2026

Cryptocurrencies

Bitcoin -12.47% MTD and -26.80% YTD to $64,186.40

Ethereum -13.45% MTD and -41.68% YTD to $1,737.24

Bitcoin was +4.71% over the last seven days and Ethereum was +7.91%. On Wednesday, Bitcoin was -2.32% and Ethereum -3.18%. Cryptocurrencies were up this week due to Bitcoin being supported by record-low exchange supplies, while other cryptocurrencies have been supported by the expansion of tokenised equity shares. The global market capitalisation rose to approximately $2.29 trillion. However, the market fell on Wednesday following the Fed’s monetary policy meeting where the hawkish bent was revealed, erasing a relief rally driven by easing Middle East tensions following the US and Iran agreeing an interim deal that extends their ceasefire. The Fed’s new projections indicated nine officials foresee at least one hike, with six anticipating at least two. The nine others expect the Fed to hold rates this year. In short, the meeting created a general "risk-off" sentiment across risk-on assets. In addition, institutional investors have been drawn in by the SpaceX IPO.

Note: As of 5:00 pm EDT 17 June 2026

Fixed Income

US 10-year yield +5.7 bps MTD and +32.8 bps YTD to 4.500%

German 10-year yield -1.1 bps MTD and +7.1 bps YTD to 2.931%

UK 10-year yield -6.3 bps MTD and +28.0 bps YTD to 4.758%

Short-dated Treasury yields rose to their highest levels in 16 months on Wednesday as investors interpreted the Fed’s decision to leave rates unchanged, together with the first policy meeting under Chair Kevin Warsh, as signalling a more hawkish policy stance.

The 10-year Treasury yield rose +5.5 bps to 4.500%, while the 2-year yield, which is most sensitive to expectations for Fed policy, climbed +12.7 bps to 4.195%, its highest level since February 2025. At the long end, the 30-year yield declined -1.3 bps to 4.933%. US rate markets were pricing in a 44.3% probability of a Fed rate increase by October and an 83.1% probability by December.

The move left the 2s10s curve 9.6 bps flatter at 30.5 bps from last week’s 40.1 bps, reflecting a bear-flattening bias.

Updated quarterly projections showed that nine Fed officials now expect at least one further rate increase by the end of 2026. In addition, the revised policy statement removed language that had previously signalled the possibility of lower borrowing costs later this year.

The shorter policy statement, reflecting a format more reminiscent of the Alan Greenspan era, was approved unanimously by the FOMC in a 12 - 0 vote. Investors viewed the overall message from the meeting as clearly hawkish.

Over the week, the US yield curve flattened as shorter-dated yields moved higher while longer-dated yields declined. At the front-end, the 2-year yield was +3.7 bps higher over the past seven days, the 10-year yield declined by -5.9 bps and, at the longer end, the 30-year yield traded -9.9 bps lower.

US retail sales rose 0.9% in May, following a downwardly revised 0.4% increase in April, according to the Commerce Department’s Census Bureau.

The data pointed to continued resilience in the US consumer despite ongoing pressure on real purchasing power. Although higher fuel prices have weighed on household budgets, there is still limited evidence of a material slowdown in consumer spending.

Part of the increase in headline sales reflected stronger receipts at service stations, driven by higher gasoline prices. Fuel prices were pushed to four-year highs by disruption linked to the Iran conflict.

Retail sales excluding autos, gasoline, building materials and food services rose 0.7% in May, following an unrevised 0.5% gain in April. These core retail sales are the measure most closely aligned with the consumer spending component of US GDP.

According to CME Group's FedWatch Tool, Fed funds futures traders are now pricing in a 29.9% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 10.4% from last week. Fed funds futures traders are pricing in 32.2 bps of rate hikes in 2026, higher than the 23.4 bps of rate hikes priced in a week ago.

Across the Atlantic, in the UK, Britain’s 10-year Gilt yield declined by -3.4 bps to 4.939%. On a weekly basis, the 10-year Gilt yield is -18.1 bps lower.

Long-term eurozone government bonds extended their rally for a fifth consecutive session on Wednesday, marking the longest run of gains since February, as moderating inflation expectations continued to support the asset class.

Germany’s 10-year Bund yield fell by -0.4 bps to 2.931%, with Bund prices posting their longest advance since mid-February, before the onset of the Iran conflict.

At the front end of the curve, the two-year Schatz yield, which is more sensitive to changes in inflation and rate expectations, rose by +1.9 bps to 2.595%. Further out the curve, the 30-year yield declined by -1.5 bps to 3.481%.

Market pricing continues to imply one additional 25 bps rate increase by the ECB this year, following last Thursday’s 25 bps move. By comparison, a week earlier, markets had priced in a cumulative 75 bps of tightening for 2026.

In the periphery, Italy’s 10-year BTP yield fell by -1.6 bps to 3.629%, leaving the spread over the German Bund largely unchanged at 69.8 bps, or 5.9 bps lower than last week’s 75.7 bps. Over the past seven days, the 10-year BTP yield has decreased by -20.7 bps.

During the past week, the German yield curve bear-flattened, by 1.7 bps to 33.6 bps from last week’s 35.3 bps. Over the course of the past seven days, the two-year Schatz yield traded -13.1 bps lower, while yield on the 10-year bund declined by -14.8 bps. At the longer end, the 30-year German yield was -12.9 bps lower throughout the week.

The yield spread between German Bunds and 10-year UK gilts reached 182.7 bps on Wednesday, a decrease of 3.3 bps over the past seven days.

The spread between US 10-year Treasuries and German Bunds is now 156.9 bps, reflecting an expansion of 8.9 bps from last week’s 148.0 bps.

Commodities

Gold spot -6.13% MTD and -1.31% YTD to $4,257.68 per ounce

Silver spot -10.08% MTD and -5.04% YTD to $67.67 per ounce

West Texas Intermediate crude -13.80% MTD and +31.77% YTD to $75.65 a barrel

Brent crude -14.44% MTD and +29.22% YTD to $78.71 a barrel

Gold fell more than one percent on Wednesday after the Fed left rates unchanged but signalled the possibility of higher borrowing costs later this year, lifting the US dollar and weighing on bullion prices.

Spot gold declined -1.67% to $4,257.68 per ounce. On a weekly basis, spot gold was +4.52% higher.

The stronger US dollar following the Fed decision made dollar-denominated bullion more expensive for overseas buyers.

Silver fell -3.22% to $67.67 per ounce. However, it advanced +6.23% over the past week.

Oil prices declined on Wednesday as concerns over a potential supply surplus next year outweighed geopolitical uncertainty surrounding the proposed US-Iran ceasefire agreement.

Brent crude futures settled down 78 cents, or 0.98%, at $78.71 a barrel, while US WTI fell by 97 cents, or 1.27%, to $75.65. Over the past week, WTI has declined -17.64%, while Brent is down -16.92%.

Market volatility persisted as uncertainty remained over the timing and finalisation of the proposed agreement between Iran and the US, which is expected to be signed on Friday, although reports suggested that a virtual signing could take place sooner. Sentiment was further unsettled after the US President said the agreement was not yet final and warned that military action could resume if the terms proved unsatisfactory.

Shipping conditions also remained in focus. Reports on Wednesday, following similar updates earlier in the week, indicated that a full return to normal traffic through the Strait of Hormuz will take time, although tanker-tracking data suggested that transits through the waterway have increased over the past several days.

The IEA’s June Oil Market Report lowered its 2026 global demand forecast by 700,000 bpd to 103.29 million bpd. Global supply for 2026 is now expected to decline by 3.9 million bpd year on year to 102.4 million bpd.

Looking further ahead, the agency expects the market to move into a significant surplus in 2027 as the reopening of the Strait of Hormuz supports supply growth of 8.0 million bpd, more than offsetting projected demand growth of 2.0 million bpd. Total supply in 2027 is forecast to rise to 110.3 million bpd.

EIA report. The latest US Energy Information Agency (EIA) report, released on Wednesday, showed that US crude inventories fell for a 10th consecutive week, as stronger demand reduced total stockpiles to their lowest level in more than 40 years.

Total crude inventories, including commercial stocks and the Strategic Petroleum Reserve, fell by 17.2 million barrels to 758.5 million, the lowest level since March 1985. Since the start of the Iran conflict, combined inventories have declined by 96.25 million barrels as global buyers have turned to US crude and refined products to help offset supply disruptions.

Commercial crude stocks, excluding the government’s emergency reserve, fell by 8.3 million barrels in the week to 12 June, to 418.2 million barrels. At the Cushing, Oklahoma delivery hub, crude inventories declined by 1.6 million barrels to 20.03 million, their lowest level since 2014 and close to operational minimums.

Refinery crude runs increased by 230,000 bpd, while refinery utilisation rose by 1.4 percentage points to 96.7%.

US gasoline inventories fell by 906,000 barrels to 214.2 million. Refinery utilisation in both the Midwest and the West Coast rose to its highest level since 2023. Total product supplied, a proxy for demand, rose by 85,000 bpd to 20.685 million bpd, while gasoline supplied increased by 481,000 bpd to 9.21 million bpd. Distillate inventories, including diesel and heating oil, increased by 1.0 million barrels to 103.1 million barrels.

Net US crude imports fell by 241,000 bpd over the week, while US crude exports declined by 513,000 bpd to 4.33 million bpd.

Note: As of 5:00 pm EDT 17 June 2026

Key data to move markets

EUROPE

Thursday: German Buba Monthly Report and speeches by Bundersbank President Joachim Nagel, ECB Executive Board members Frank Elderson and Piero Cipollone and ECB Chief Economist Philip Lane

Friday: German PPI and speeches by ECB Executive Board members Frank Elderson and Piero Cipollone and ECB Chief Economist Philip Lane

Monday: Eurozone Consumer Confidence

Tuesday: French, German and Eurozone HCOB Composite, Manufacturing and Services PMIs

Wednesday: German IFO Business Climate, Current Assessment and Expectations

UK

Thursday: BoE Interest Rate Decision, BoE’s Minutes, Monetary Policy Summary and MPC Vote, Average Earnings, Claimant Count Change and Rate, Employment Change, ILO Unemployment Rate and GfK Consumer Confidence

Friday: Retail Sales and Retail Sales ex-Fuel

Tuesday: S&P Global Composite, Manufacturing and Services PMIs and speeches by BoE External Members Alan Taylor and Swati Dhingra

Wednesday: Speeches by BoE Deputy Governor for Financial Stability Sarah Breeden and BoE External Member Swati Dhingra

USA

Thursday: Initial and Continuing Jobless Claims; US markets will be closed in observance of Juneteenth

Tuesday: ADP Employment Change 4-week Average, S&P Global Composite, Manufacturing and Services PMIs

Wednesday: New Home Sales

JAPAN

Thursday: BoJ Monetary Policy Meeting Minutes, National CPI and Core CPI

CHINA

Sunday: PBoC Interest Rate Decision

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.