What’s the true state of the US labour market?

Key data to move markets today

EU: Eurozone Unemployment Rate, speeches by ECB Executive Board members Frank Elderson and Piero Cipollone and a speech by Banco de España Governor José Luis Escrivá

UK: A speech by BoE External Member Catherine Mann

USA: Nonfarm Payrolls, Average Hourly Earnings, Initial and Continuing Jobless Claims, Labour Force Participation Rate, U6 Underemployment Rate, Unemployment Rate, Factory Orders and a speech by San Francisco Fed President Mary Daly

Global Macro Updates

Preview: June nonfarm payrolls. The June nonfarm payrolls report is scheduled for release at 8:30 am EDT today, one day earlier than usual due to the US Independence Day holiday weekend. Consensus expectations point to a headline payrolls gain of around 115,000, following May’s stronger-than-expected increase of 172,000. That was supported by leisure and hospitality hiring as well as local government employment. The unemployment rate is expected to remain unchanged at 4.3%, while average hourly earnings are forecast to rise 0.3% m/o/m.

On potential revisions, JP Morgan noted that May payrolls have tended to be revised lower in recent years, although revisions have been positive in three of the past four months.

Analyst previews generally point to continued solid employment growth in June, albeit at a slower pace than in May. Several notes cited firm weekly ADP private employment estimates and still-low jobless claims, while Goldman Sachs also highlighted recent seasonal strength in initial June payroll prints.

Some analysts attributed part of May’s strength to World Cup-related hiring and noted that June could receive an additional temporary boost. Goldman Sachs estimated a contribution of 40,000 jobs before these positions begin to unwind later in the summer. However, Citi observed that state-level data did not show a disproportionate increase in leisure and hospitality employment in states hosting games, while JP Morgan suggested that May may have been affected by early Memorial Day timing, potentially creating some payback in June.

Citi maintained a more cautious view of labour-market momentum, forecasting only 25,000 headline job gains and arguing that recent payroll data does not indicate sustainably strong labour demand. The firm pointed to rising initial claims during the June reference period, a still-low hiring rate, declining labour-force participation and weaker small-business hiring plans.

Analysts broadly expect the unemployment rate to hold at 4.3% for a fourth consecutive month. Some previews noted that the recent decline in labour-force participation could distort the rate lower, although Jefferies observed that prime-age participation remains near its highest level since 2000. JP Morgan also argued that recent increases in continuing jobless claims appear to reflect residual seasonality.

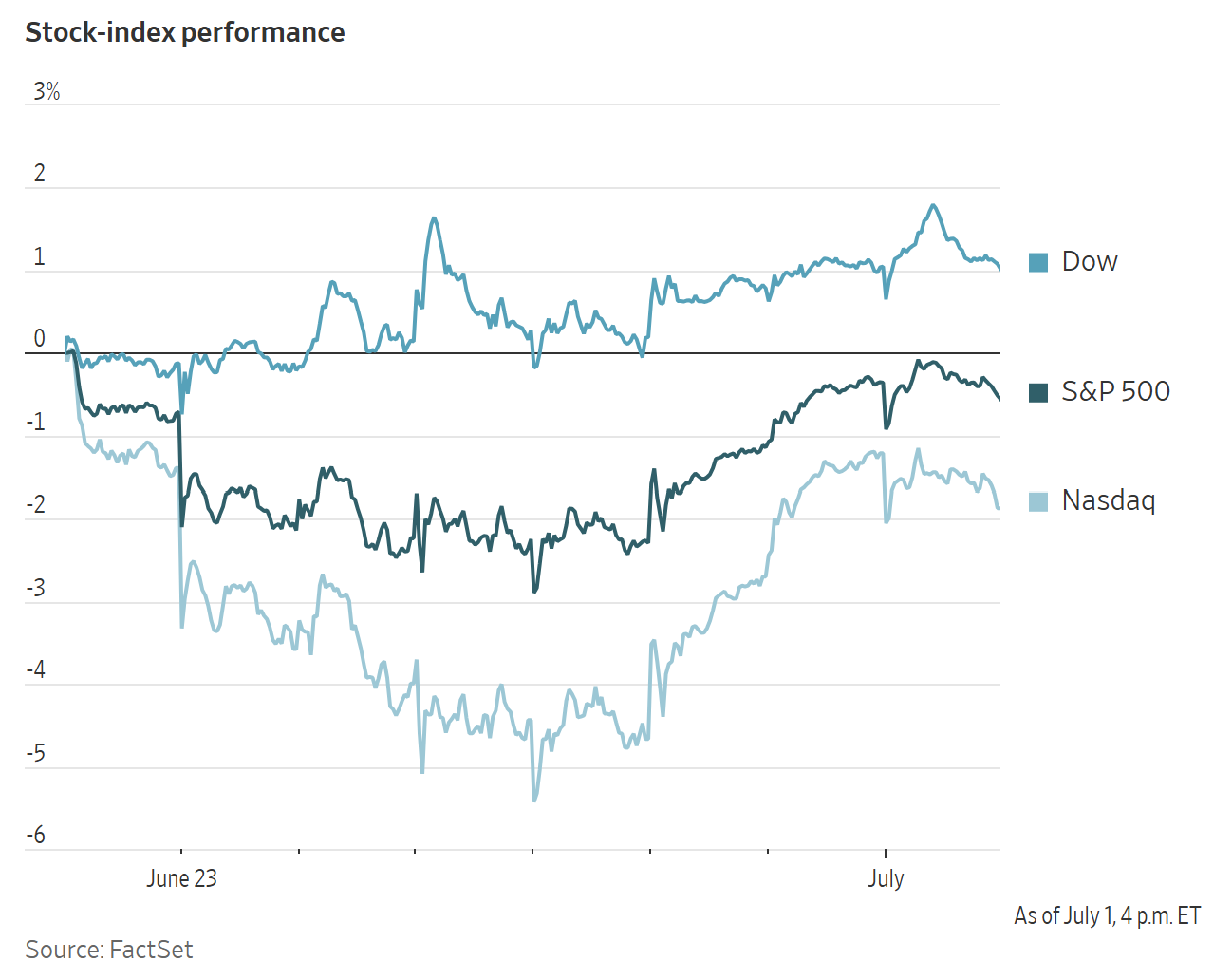

US Stock Indices

Dow Jones Industrial Average -0.03%

Nasdaq 100 -1.54%

S&P 500 -0.22%, with 5 of the 11 sectors of the S&P 500 down

Strong manufacturing data and comments from new Federal Reserve Chair Kevin Warsh lifted economically sensitive stocks on Wednesday.

Weakness in high-flying chipmaker shares weighed on the Nasdaq Composite, which fell -0.66%, while the S&P 500 declined -0.22% even as most sectors advanced. The Dow Jones Industrial Average slipped -0.03% from Tuesday’s record close.

US stock and bond markets will close on Friday in observance of Independence Day, which falls on Saturday this year. The bond market will also close early on Thursday at 2 pm EDT.

In corporate news, Meta Platforms is exploring a cloud infrastructure business that would sell access to AI computing power and models, putting it in competition with Amazon Web Services and Google Cloud. The proposed Meta Compute initiative would offer developers access to hosted AI models, including Meta’s Muse Spark models, as well as raw computing capacity. The effort is led by Santosh Janardhan, Meta’s head of infrastructure; Daniel Gross of Meta Superintelligence Labs and Meta President Dina Powell McCormick.

Alcoa agreed to acquire South32’s bauxite, alumina and aluminium assets in Australia, Brazil and South Africa for up to $5.6 billion. The consideration includes $3.1 billion in cash, 17.0 million Alcoa shares and the assumption of about $750 million in net debt and lease liabilities. The sale allows South32 to focus on higher-margin copper, zinc, silver and lead operations.

Bloomberg news reported that Apple is negotiating to buy chips from Chinese semiconductor makers ChangXin Memory Technologies and Yangtze Memory Technologies to ease the impact of a global memory shortage. Both companies are on a Pentagon blacklist of Chinese entities alleged to support Beijing’s military, prompting Apple to seek help from Trump administration officials to reduce potential political backlash.

Mega Caps

Alphabet +1.29%, Amazon +1.41%, Apple +1.73%, Meta Platforms +8.81%, Microsoft +3.02%, Nvidia -1.25% and Tesla +1.12%

European Stock Indices

CAC 40 -0.79%

DAX +0.18%

FTSE 100 -0.18%

Commodities

Gold spot +0.59% to $4,030.69 an ounce

Silver spot +0.96% to $59.14 an ounce

West Texas Intermediate -2.78% to $68.09 a barrel

Brent crude -2.39% to $71.18 a barrel

Gold prices advanced on Wednesday, supported by softer-than-expected US labour-market data and comments from Fed Chair Kevin Warsh indicating that inflation risks have moderated.

Spot gold rose +0.59% to $4,030.69 per ounce after reaching its lowest level since November in the previous session.

Spot silver also gained, adding +0.96% to $59.14 per ounce.

Oil prices declined by more than two percent on Wednesday, reaching their lowest levels since March, as optimism around US - Iran talks eased supply concerns following comments from the US President that discussions in Qatar had gone well.

Brent futures settled $1.74 lower, or -2.39%, at $71.18 per barrel, while US WTI crude fell $1.95, or -2.78%, to $68.09 per barrel. Both benchmarks closed at four-month lows.

The US and Iran held technical discussions in Doha aimed at regulating shipping flows through the Strait of Hormuz and securing a lasting ceasefire, according to a source with direct knowledge of the talks and an Iranian official. However, the two countries have continued to dispute the interpretation of the interim pact publicly, following an exchange of military strikes over the past week.

The DOE Weekly Petroleum Status Report showed a crude draw of 3.78 million barrels and a gasoline draw of 2.33 million barrels, alongside a distillate build of 2.48 million barrels and a Cushing build of 700,000 barrels. In addition, 5.5 million barrels were released from the Strategic Petroleum Reserve (SPR). The commercial crude draw marked the twelfth consecutive decline, leaving combined commercial crude and SPR stockpiles at more than 43-year lows, while jet fuel production remained above 2.0 million bpd for a ninth consecutive week.

Geopolitical risks also remained in focus, as Ukraine continued to strike Russian refineries. Moscow is still reportedly considering a diesel export ban, while Reuters reported that Russia is importing sizable volumes of gasoline from India and other sources to offset lost domestic supply.

Energy Aspects estimates that global clean-product stockpiles are at their lowest levels in more than 10 years, while onshore crude inventories continue to draw at nearly 4.0 million bpd.

Attention now turns to the OPEC-7 meeting this coming Sunday. Reuters sources indicated that the group is likely to approve an additional production quota increase of 188,000 bpd, although recent reports suggest that Iraq is seeking a larger quota increase on a shorter timeline.

Note: As of 4 pm EDT 1 July 2026

Currencies

EUR -0.40% to $1.1375

GBP +0.11% to $1.3269

Bitcoin +3.77% to $60,762.88

Ethereum +3.96% to $1,631.21

The US dollar gained ahead of the closely watched US jobs report due today. It pared earlier gains after Fed Chair Kevin Warsh said inflation expectations and inflation risks had eased in recent weeks.

The Japanese yen, which had earlier slumped to a 40-year low against the greenback, edged -0.01% lower to ¥162.52.

The dollar has been underpinned by rising expectations of Fed rate hikes this year, as inflation runs well above the central bank's 2% annual target.

The dollar index was up +0.23% at 101.41. The euro declined -0.40% to $1.1375. The British pound advanced +0.11%.

Fixed Income

US 10-year Bond +1.5 basis points to 4.485%

German 10-year Bund +2.0 basis points to 2.884%

UK 10-year Gilt -1.0 basis points to 4.759%

The US Treasury yield curve bull steepened on Wednesday, as short-term yields declined while longer-dated yields moved higher. The 10-year yield rose at the start of July, but eased from earlier highs following softer economic data and remarks from Fed Chair Kevin Warsh.

Speaking on a panel of central bankers in Sintra, Portugal, Warsh said inflation expectations and inflation risks had declined in recent weeks. However, he reiterated that the Fed would remain firmly focused on its 2% inflation target and would disappoint those expecting a shift toward looser monetary policy.

The yield on the US 10-year Treasury note increased +1.5 bps to 4.485%, after earlier reaching 4.501% before Warsh’s remarks, its highest level since 24 June. The two-year US Treasury yield, which typically tracks interest rate expectations for the Fed, declined -1.2 bps to 4.183%, after touching a one-week high of 4.199% earlier in the session. The spread between the US two-year and 10-year Treasury yields stood at 30.2 bps.

The 30-year yield rose +0.9 bps to 4.974%.

Yields had already begun to pare gains after the ADP National Employment Report showed private payrolls rose by 98,000 in June, below the 118,000 consensus estimate, following an unrevised gain of 122,000 in May.

Investors will look to today’s NFP report for further insight into the health of the labour market. US markets will be closed on Friday for the Independence Day holiday on 4 July.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 36.7 bps of rate hikes in 2026, higher than the 33.7 bps priced in a week ago. Fed funds futures traders are now pricing in a 28.3% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 34.2% last week.

Eurozone bond yields edged higher on Wednesday, although shorter-dated yields declined after June inflation slowed more than expected and eased some of the urgency around further monetary tightening. Data released on Wednesday showed eurozone inflation slowed to 2.8% in June, from 3.2% in May, and came in below economists’ expectations of 3.0%.

Germany’s 10-year bond yield rose +2.0 bps to 2.884%. Germany’s two-year yield, which is sensitive to ECB rate expectations, fell -1.4 bps to 2.520%.

During the Sintra panel, ECB President Christine Lagarde said risks to eurozone inflation and economic growth were now more broadly balanced than a few weeks earlier, supported in part by the recent decline in oil prices.

Money markets are pricing in around 16 bps of additional monetary tightening this year, suggesting investors view another rate increase as highly likely, though not fully certain.

ECB policymakers continued to signal differing views. Governor of the Central Bank of Malta, Alexander Demarco, said on Wednesday that the central bank should not rush into another increase, while German Bundesbank President Joachim Nagel maintained that inflation remains too high.

Note: As of 4 pm EDT 1 July 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.