Just how confident is the labour market?

Key data to move markets today

EU: Spanish, Italian, German and Eurozone’s HCOB Manufacturing PMIs, Eurozone Harmonised Index of Consumer Prices and Core Harmonised Index of Consumer Prices and speeches by ECB President Christine Lagarde, ECB Vice President Boris Vujčić, ECB Chief Economist Philip Lane and ECB Executive Board member Piero Cipollone

UK: A speech by BoE Governor Andrew Bailey

USA: ADP Employment Change, ISM Manufacturing PMI, Employment and New Orders Indices and Prices Paid and a speech by Fed Chair Kevin Warsh

Global Macro Updates

US data mixed as labour market holds steady, confidence softens. May JOLTS job openings rose slightly to 7,594,000, above consensus of 7,300,000 and April’s 7,585,000. The reading marked the highest level since November 2024, while the job openings rate was unchanged m/o/m at 4.6%.

Labour turnover metrics were similarly steady. The hiring rate was unchanged at 3.3%, the quit rate held at 1.9% and the total separations rate remained at 3.2%. Layoffs and discharges increased modestly to 1.1% from 1.0%.

Consumer confidence was softer than expected in June, coming in at 91.2 versus consensus of 94.7 and May’s revised 90.6. The Present Situation Index declined to 116.4 from 119.4, while the Expectations Index improved to 74.4 from 71.4. The report noted that lower oil prices provided some relief to consumers’ inflation concerns.

However, consumers’ assessment of the labour market deteriorated. The share of respondents saying jobs were ‘plentiful’ was essentially unchanged at 24.9%, compared with 24.8% in May, while the share saying jobs were ‘hard to get’ rose to 22.5% from 19.8%.

Separately, the June Chicago PMI declined to 56.7, below consensus of 58.1 and May’s 62.7. The decrease was driven by weaker New Orders and Production, partly offset by increases in Supplier Deliveries, Order Backlogs and Employment. Prices Paid rose to the highest level since May 2022.

US Stock Indices

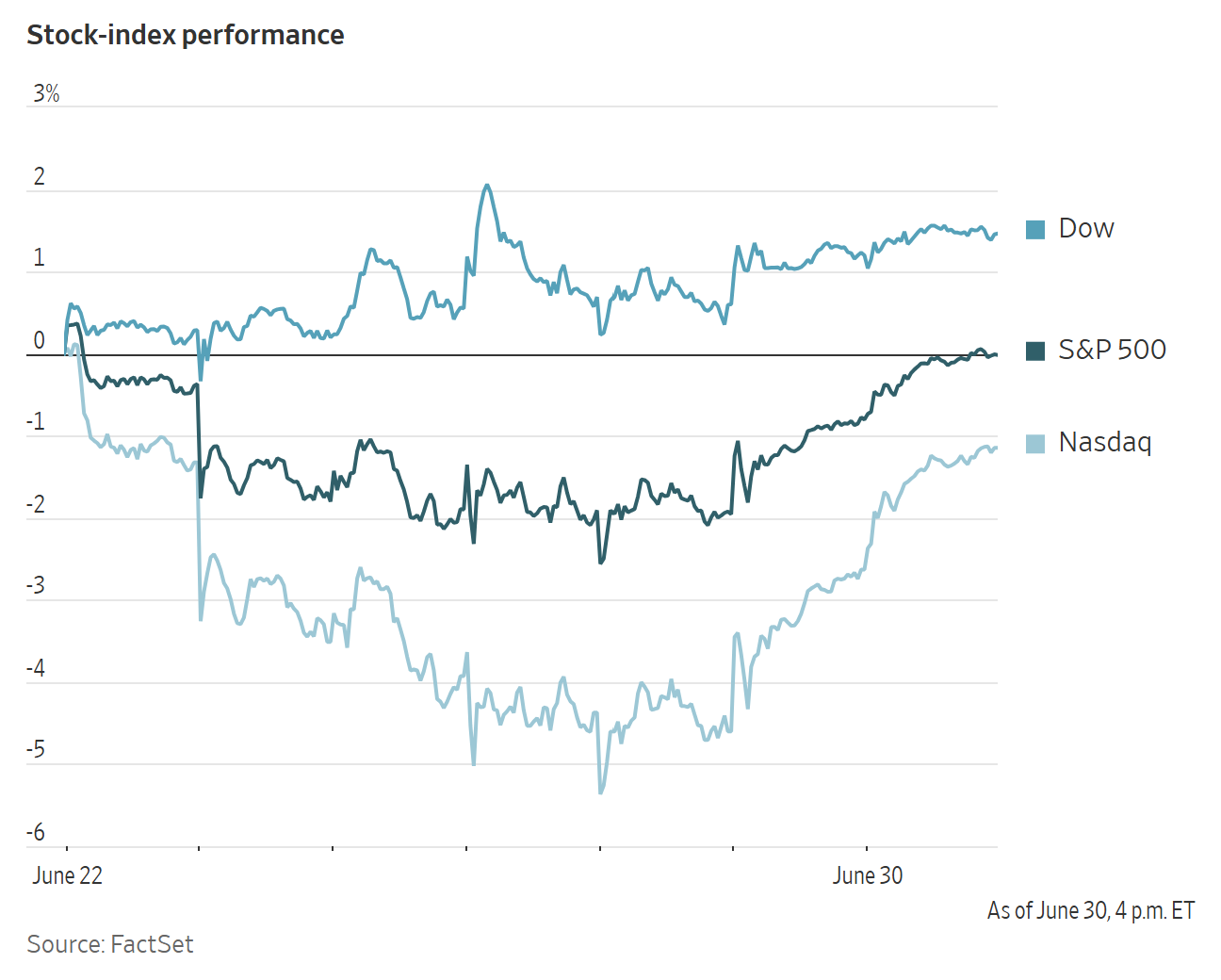

Dow Jones Industrial Average +0.26%

Nasdaq 100 +1.68%

S&P 500 +0.79%, with 4 of the 11 sectors of the S&P 500 up

US equities ended Q2 with renewed momentum. Major indexes posted their best quarterly gains in years. The S&P 500 rose +14.87%, while the Nasdaq Composite climbed +21.41%, marking the strongest quarterly advances for both indices since Q2 2020. The Dow Jones Industrial Average gained +12.90%, its best quarter since 2022.

The rally came despite notable volatility, including last week’s selloff in technology shares, as investors returned to the trade this week.

In H1 2026, the S&P 500 and Nasdaq Composite recorded 24 and 20 record closes, respectively, supported by AI-driven gains among chipmakers tied to the build-out. In the final session of Q2, the S&P 500 rose +0.79%, the Nasdaq gained +1.52% and the Dow advanced +0.26%.

In corporate news, Anthropic PBC is launching software designed to help scientists automate research and reduce repetitive work.

The Supreme Court agreed to hear Apple’s appeal of a contempt ruling in its long-running antitrust dispute with Fortnite maker Epic Games.

Visa, Stripe and Bank of New York Mellon are among dozens of financial firms collaborating to launch a stablecoin, aiming to expand the use of digital money technology.

The Food and Drug Administration authorised Philip Morris International to market Zyn nicotine pouches as less harmful than cigarettes, the first such designation for the category.

Mega Caps

Alphabet +0.58%, Amazon -0.75%, Apple +2.70%, Meta Platforms +0.12%, Microsoft +1.21%, Nvidia +2.63% and Tesla +2.13%

European Stock Indices

CAC 40 +0.44%

DAX +1.50%

FTSE 100 +0.12%

Commodities

Gold spot -0.22% to $4,007.23 an ounce

Silver spot +0.48% to $58.58 an ounce

West Texas Intermediate -0.54% to $70.04 a barrel

Brent crude +0.16% to $72.92 a barrel

Gold edged lower on Tuesday. It experienced its sharpest quarterly decline in 13 years, as inflation concerns linked to the Middle East conflict reinforced expectations that the Fed could raise interest rates.

Spot gold fell -0.22% to $4,007.23 per ounce after earlier touching its lowest level since November. It had its worst quarter since 2013, when the Gulf conflict heightened inflation concerns, after rising across nine of the prior 10 quarters.

Spot silver rose +0.48% to $58.58 per ounce but still recorded its worst quarterly decline since Q1 2020.

Oil prices were little changed on Tuesday. They experienced their largest monthly and quarterly losses since the COVID-19 pandemic in early 2020. Investors continued to monitor potential US - Iran talks in Doha amid a strained interim ceasefire in the four-month conflict.

Brent futures rose $0.12, or +0.16%, to settle at $72.92 per barrel, while US WTI crude fell $0.38, or -0.54%, to settle at $70.04 per barrel.

Both benchmarks were close to their 27 February levels, the day before the start of the US - Israeli war on Iran, when Brent closed at $72.48 per barrel and WTI closed at $67.02.

Top US envoys who arrived in Doha will not hold a high-level meeting with Iran, a Qatari official said on Tuesday, casting doubt on progress toward a lasting halt to the conflict and a full reopening of the Strait of Hormuz. Before the war, roughly twenty percent of global oil supplies passed through the strait.

Instead, technical talks are expected this week on issues including regional security, which could later be elevated to a senior level, according to Qatar Foreign Ministry spokesperson Majed Al Ansari.

The lack of price movement left both crude benchmarks in technically oversold territory, with Brent there for 13 consecutive sessions and WTI for 11.

In June, Brent fell -20.73%, its largest monthly decline since the record 55.0% drop in March 2020 during COVID-related demand destruction. US WTI declined -20.19% over the month.

On supply, Argus sources said Kuwait production has recovered to about 1.9 million bpd from a low of less than 600,000 bpd in April and May. Iraq production is rising across several oilfields. Kpler estimated UAE crude and condensate exports at a record 3.7 million bpd in June.

Demand signals from China remained weak. Traders told Bloomberg news that Unipec offered Forties, a key North Sea crude grade, at its deepest discount to Dated Brent in more than six years. Separately, Beijing reportedly informed several state refiners that they may export fuels, including gasoline and diesel, to a wider group of countries, easing restrictions introduced at the start of the Iran war.

Note: As of 4 pm EDT 30 June 2026

Currencies

EUR -0.03% to $1.1421

GBP -0.01% to $1.3254

Bitcoin -3.06% to $58,558.14

Ethereum -3.04% to $1,569.03

The US dollar strengthened on Tuesday, pushing the yen to its weakest level since 1986 and increasing expectations that Japanese authorities could be nearing direct intervention.

The dollar rose as high as ¥162.66 yen and was up +0.38% at ¥162.51 on the day. Japanese Finance Minister Satsuki Katayama reiterated that authorities were prepared to respond appropriately at any time, though she stopped short of more forceful rhetoric.

The dollar index rose +0.06% to 101.17 and recorded a +2.25% gain in June.

Japanese authorities intervened in April and May, spending ¥11.7T to support the currency, though the effect of that support has since faded.

The euro edged down -0.03% to $1.1421, remaining near the one-year low reached last week.

Sterling slipped -0.01% to $1.3254.

Fixed Income

US 10-year Bond +9.0 basis points to 4.470%

German 10-year Bund -0.2 basis points to 2.684%

UK 10-year Gilt +4.5 basis points to 4.769%

US Treasury yields rose on Tuesday, although the 10-year yield ended a three-month streak of gains following labour-market data and as investors monitored potential peace talks between the US and Iran.

The 10-year Treasury yield increased +9.0 bps to 4.470%.

Adding to a recent series of Fed comments emphasising inflation risks, Cleveland Fed President Beth Hammack said she could still support higher interest rates if inflation pressures do not moderate.

The 30-year yield rose +9.8 bps to 4.965%, while the 2-year yield advanced +8.0 bps to 4.115%.

The US Treasury yield curve, measured by the spread between 2-year and 10-year yields, stood at a positive 27.5 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 34.7 bps of rate hikes in 2026, lower than the 37.7 bps priced in a week ago. Fed funds futures traders are now pricing in a 33.7% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 36.3% last week.

In the UK, gilts were up on Tuesday due to stronger-than-expected economic growth data, which reduced the likelihood of imminent interest rate cuts by the Bank of England. The UK benchmark 10-year was +4.5 bps to 4.769%.

Eurozone bond yields were mixed on Tuesday.

Germany’s 10-year yield declined -0.2 bps to 2.864%, remaining near its highest level in a week.

Germany’s 2-year yield, which is sensitive to ECB deposit-rate expectations, slipped -3.3 bps to 2.534%.

Money markets are pricing in one additional 25 bps rate hike from the ECB this year, following its rate increase earlier this month.

Note: As of 4 pm EDT 30 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.