Corporate Earnings Calendar 17 July - 23 July 2025

Thursday: Abbot Laboratories, PepsiCo, Taiwan Semiconductor Manufacturing, Netflix, Novartis, US Bancorp., Marsh & McLennan, Snap-On

Friday: 3M, American Express, SLB, Charles Schwab

Monday: Verizon, Domino’s Pizza, Steel Dynamics, NXP Semiconductors

Tuesday: GE Aerospace, Coca-Cola, General Motors, Philip Morris International, Intuitive Surgical, Texas Instruments, SAP, Lockheed Martin, Chubb Ltd, Sherwin-Williams, Northrop Grumman, Baker Hughes

Wednesday: Tesla, Alphabet, AT&T,CME Group, Thermo Fisher Scientific, GE Vernova, IBM, QuantumScape, ServiceNow

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +1.01% MTD and +9.02% YTD

Dow Jones Industrial Average -0.16% MTD and +3.48% YTD

NYSE +0.28% MTD and +7.27% YTD

S&P 500 +0.95% MTD and +6.50% YTD

The S&P 500 is +0.01% over the past week, with 8 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is -1.10% over this past week and +4.32% YTD.

The S&P 500 Information Technology is the leading sector so far this month, +2.92% MTD and +10.85% YTD, while Communication Services is the weakest sector at -1.72% MTD and +8.72% YTD.

Over this past week, Information Technology outperformed within the S&P 500 at +0.94%, followed by Real Estate and Consumer Discretionary at +0.84% and +0.56%, respectively. Conversely, Materials underperformed at -2.54%, followed by Energy and Healthcare at -2.11% and -1.03%, respectively.

The equal-weight version of the S&P 500 was +0.40% on Wednesday, underperforming its cap-weighted counterpart by 1.11 percentage points.

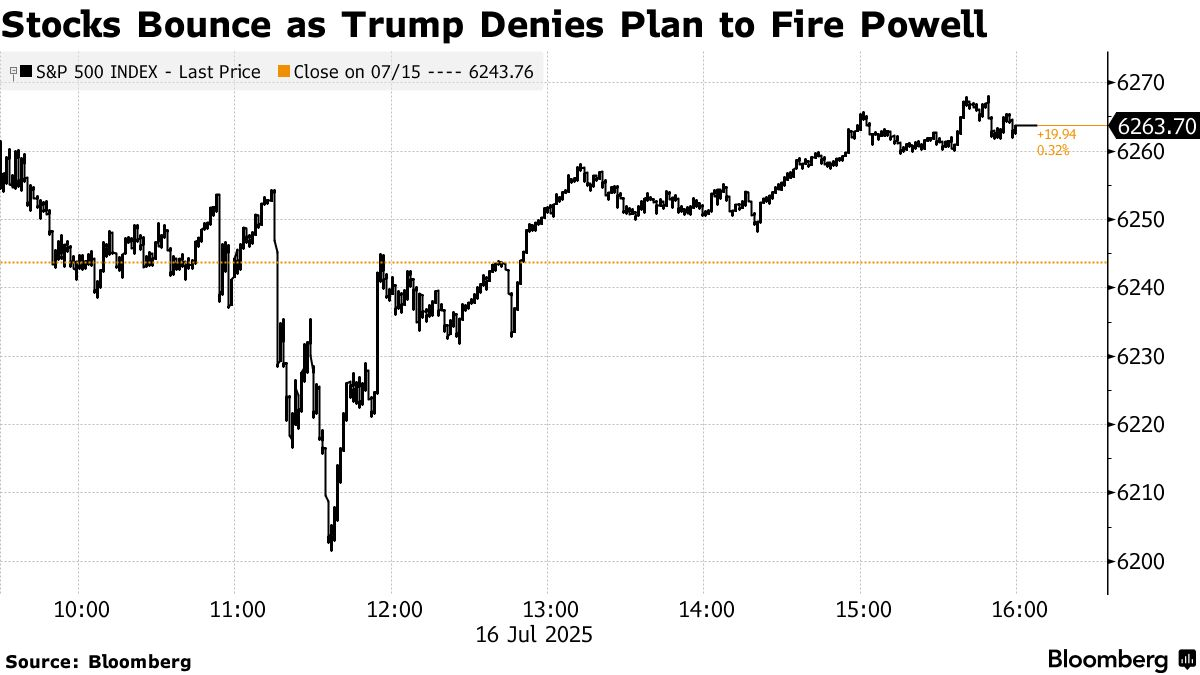

US equities fell on Wednesday after a Bloomberg report suggested that President Trump was looking to fire Fed Chair Jerome Powell. Stocks managed to bounce back after a second report stating that President Trump said he is “not planning on doing anything” to remove Fed Chair Jerome Powell. The Nasdaq Composite closed at 20,730.49, up 52.69 points, or +0.26%. It was the fifth session in six that the technology-heavy index posted a record high. The Dow Jones Industrial Average rose 231.49 points, or +0.53%, to 44,254.78, and the S&P 500 gained 19.94 points, or +0.32%, at 6,263.70.

According to LSEG I/B/E/S data, 2025 Q2 y/o/y earnings are expected to be 6.5%. Excluding the Energy sector, the y/o/y earnings estimate is 8.3%. Of the 36 companies in the S&P 500 that have reported earnings to date for 2025 Q2, 80.6% reported above analyst expectations. This compares to a long-term average of 67%. The 2025 Q2 y/o/y blended revenue growth estimate is 4.0%. If the Energy sector is excluded, the growth rate for the index is 5.3%.

In corporate news, on Wednesday Alphabet said it will debut new Pixel-branded hardware powered by the company’s AI technology at an event on 20 August in New York, with the lineup expected to include several smartphones and a smartwatch.

United Airlines Holdings reported a second-quarter profit, ahead of expectations, and grew both earnings and pre-tax margin in the first half of 2025 versus the first half of 2024. It increased its full-year adjusted earnings of $9 to $11 a share as travel demand has picked up since the beginning of July due to fewer flight disruptions, less geopolitical and macroeconomic uncertainty.

Goldman Sachs reported that profits beat Q2 estimates with its equities division revenues rising 36% to a new record. It also reported a pickup in dealmaking. Fixed income, currencies, and commodities hauled in $3.47 billion, 9% higher than a year ago. JPMorgan Chase and Citigroup also reported strong growth in investment banking fees, while Morgan Stanley and Bank of America posted declines.

Johnson & Johnson beat quarterly sales expectations and raised its full-year outlook. The pharmaceutical industry faces the dual threats of tariffs as high as 200% if they don’t shift more of their manufacturing to the US over the next year to 18 months and regulatory action on drug pricing. The White House has threatened to impose a policy that would force drug companies to charge the US government the lowest prices they offer to other wealthy countries for some patients. Johnson & Johnson Chief Executive Officer Joaquin Duato said the company is already in the process of shifting its manufacturing so that all the drugs consumed by Americans are made in the US.

Mega caps: The Magnificent Seven had a mixed performance this week. Nvidia shares benefitted from the news that it would be allowed to sell its H2O chips in China. However, Meta platforms saw its stock prices fall as an $8 billion trial by Meta Platforms shareholders against Mark Zuckerberg and others present and past company leaders over claims they illegally harvested the data of Facebook users in violation of a 2012 agreement with the US Federal Trade Commission started on Wednesday. This week Nvidia is +5.21%, Microsoft +0.42%, Meta Platforms -4.08%, Amazon +0.29%, Apple -0.46%, Alphabet +3.60%, and Tesla +8.72%.

Energy stocks had largely negative performance this week, with the Energy sector itself -2.11%. WTI and Brent prices are -2.92% and -2.12%, respectively, this week. Over this past week Hess -2.21%, APA -11.30%, Occidental Petroleum -6.45%, Chevron -2.03%, Phillips 66 -5.24%, Marathon Petroleum -3.85%, ExxonMobil -1.38%, Halliburton -3.63%, Shell -0.72%, ConocoPhillips -3.19%, and Baker Hughes -1.65%, while BP +2.99% and Energy Fuels +47.45%.

Materials and Mining stocks also had a largely negative performance this week, with the Materials sector -2.54%. Over the past seven days, CF Industries -6.23%, Albemarle -0.54%, Yara International -1.13%, Nucor -1.37%, Freeport-McMoRan -3.53 %, Mosaic -4.82%, Celanese Corporation -6.34% and Newmont Corporation -0.51%, while Sibanye Stillwater +14.63%.

European Stock Indices Price Performance

Stoxx 600 +0.09% MTD and +6.74% YTD

DAX +0.42% MTD and +20.59% YTD

CAC 40 +0.73% MTD and +4.62% YTD

IBEX 35 +0.08% MTD and +19.76% YTD

FTSE MIB -0.76% MTD and +16.78% YTD

FTSE 100 +2.02% MTD and +9.36% YTD

This week, the pan-European Stoxx Europe 600 index is -1.48%. It was -0.57% on Wednesday, closing at 541.84.

So far this month in the STOXX Europe 600, Basic Resources is the leading sector, +2.94% MTD and -5.58% YTD, while Retail is the weakest at -3.98% MTD and -4.58% YTD.

This week, Basic Resources outperformed within the STOXX Europe 600, at +0.80%, followed by Financial Services and Oil & Gas at +0.10% and -0.49%, respectively. Conversely, Retail underperformed at -3.36 %, followed by Banks and Chemicals at -2.99% and -2.77%, respectively.

Germany's DAX index was -0.21% on Wednesday, closing at 24,009.38. It was -2.20% for the week. France's CAC 40 index was -0.57% on Wednesday, closing at 7,722.09. It was -1.98% over the past week.

The UK's FTSE 100 index was +0.80% over the past week to 8,938.32. It was -0.66% on Wednesday.

In Wednesday's trading session, the STOXX Europe 600 index was -0.57%. The Technology sector was one of the biggest decliners, led by ASML Holding, which was down sharply despite a strong Q2 beat. The decline was triggered by a cautious 2026 outlook due to geopolitical risks. The sector experienced downward pressure due to ongoing concerns regarding tariffs and escalations in trade-related rhetoric originating from the United States.

The Autos & Parts sector also saw major declines, with Renault as the biggest laggard after it cut its margin guidance. Weak first-half volumes and pricing pressures spooked investors. Chemicals was similarly weak, with Resco slumping after a disappointing financial update and EGM plans, and BRG also falling after its second-quarter earnings per share missed expectations.

Chemicals likewise exhibited weakness, as Borregaard lost ground after its Q2 EPS fell short of expectations. Basic Resources were down sharply amid mixed updates. Antofagasta's second-quarter production was underwhelming, but Rio Tinto saw a 13% rebound in its second-quarter Pilbara iron ore shipments following weather disruptions. Meanwhile, Barclays rating downgrades hit both ArcelorMittal and Outokumpu.

Conversely, Financials benefited from a wave of positive earnings updates and resilient sentiment. While Svenska Handelsbanken missed its earnings forecast, its positive cost control was noted by the market. Luxury and Consumer Goods also helped prop up the Personal & Household Goods sector, with a focus on Compagnie Financière Richemont after it beat expectations on first-quarter sales, driven by its Jewellery Maisons.

Other Global Stock Indices Price Performance

MSCI World Index +0.35% MTD and +9.48% YTD

Hang Seng +1.85% MTD and +22.22% YTD

The MSCI World Index is -0.35% over the past 7 days while the Hang Seng Index is +2.62% over the past 7 days.

Currencies

EUR -1.24% MTD and +12.42% YTD to $ 1.1641.

GBP -2.27% MTD and +7.26% YTD to $1.3413.

The dollar fell 1.2% against a basket of major currencies on Wednesday immediately after reports came from Bloomberg news and CBS saying the US president had asked a group of Republican lawmakers whether he should sack Fed chief Jay Powell. It subsequently pared losses against the euro and yen after President Trump said it was “highly unlikely” he would imminently fire the Fed chair. The dollar had hit multi-week highs on Tuesday. The dollar index ended a six-day winning streak and fell -0.32% on Wednesday to 98.30. It is +0.76% this week and +1.47% so far MTD. However, it remains -9.39% year-to-date.

The euro got as high as $1.1721 on Wednesday before settling at $1.1641, as investors reduced their expectations of total rate cuts this year following the release of June PPI data. US producer prices were unexpectedly unchanged in June as an increase in the cost of goods because of tariffs on imports was offset by weakness in services. On Tuesday CPI had come in at its highest level in five months. This resulted in higher expectations of the Fed maintaining rates at their current level. The euro registered a weekly fall of -0.68% against the US dollar.

The ECB is expected to keep rates on hold when it meets next week. However, the stronger euro and the renewal of tariff threats are increasing disinflationary pressures for the eurozone, risking inflation undershooting and increasing the likelihood of more ECB rate cuts later this year.

Sterling was +0.28% against the US dollar on Wednesday, settling at $1.3413. It was -0.1% versus the euro to 86.75 pence on Wednesday after it hit 86.96 pence per euro on Tuesday, its lowest level since 11 April. For the week, the British pound is -1.31% versus the US dollar. Markets are pricing in an 80% chance of a 25 bps rate cut in August, more than 50 bps by year end and 75 bps by April 2026. BoE MPC member Catherine Mann warned on Tuesday that unemployment fears and rising bills are causing cautious consumer behaviour with the economy being held back by savings rates that remain much higher than before Covid.

The dollar was -0.65% to ¥147.89 on Wednesday. The dollar is +1.06% this week against the Japanese currency and +2.68% MTD but -5.93% YTD.

Note: As of 5:00 pm EDT 16 July 2025

Cryptocurrencies

Bitcoin +12.04% MTD and +28.66% YTD to $119,775.

Ethereum +35.89% MTD and +1.42% YTD to $3,380.

Bitcoin is +7.81% and Ethereum +21.87% over the past 7 days. On Wednesday Bitcoin was +1.96% to $119,975. Ethereum was +7.84% to $3,380. Bitcoin surged this week past the $123,000 mark on Monday as institutional investors continued to pile into Spot Bitcoin ETFs and corporates sought to include Bitcoin in their portfolios. Cryptocurrencies overall have risen this week on hopes that the US Congressional ‘crypto week’ will improve the landscape for digital currencies and set a fundamental precedent for future digital asset regulation. The Genius Act would establish a federal regulatory framework for stablecoins, while the other two other crypto bills expected to be voted on this week, the CLARITY Act and Anti-CBDC Surveillance State Act, would, respectively, establish a regulatory framework for digital assets in the US and prevent the Federal Reserve from issuing its own currency.

Ethereum has soared this week as nine Spot Ethereum ETFs saw their most significant daily net inflow on Wednesday, totalling $726.74 million. The inflows were led by $499 million into BlackRock's ETHA, with eight out of nine ether funds reporting positive flows for the day, according to SoSoValue data. It seems that Ethereum may, like Bitcoin, increasingly be seen as a long-term institutional asset as open interest in Ether futures on CME Group hit a high on Wednesday.

Note: As of 5:00 pm EDT 16 July 2025

Fixed Income

US 10-year yield +22 bps MTD and -12 bps YTD to 4.45%.

German 10-year yield +11 bps MTD and +24 bps YTD to 2.69%.

UK 10-year yield +14 bps MTD and +8 bps YTD to 4.64%.

US Treasury yields fell across the curve on Wednesday with the two-year yield most affected following reports by CBS and Bloomberg news that President Trump had suggested to a group of House Republicans that he would fire Fed Chair Jerome Powell. This news caused the spread between two and 10 year yields to widen as much as 61.8 bps, the steepest level since April, as investors suddenly worried about the independence of the Fed and a possible loss of its credibility. However, within an hour, the report was denied by President Trump and he said it was “highly unlikely” he would imminently fire the Fed chair.

The yield on benchmark US 10-year notes ended Wednesday -3 bps, settling at 4.45%. The yield on the interest rate-sensitive two-year note was -5 bps to 3.89%, while the 30-year yield was -1 bp to 5.01%.

Over the past seven days, the yield on the 10-year Treasury note is +11 bps. The yield on the 30-year Treasury bond is +14 bps. On the shorter end, the two-year Treasury yield is +2 bps.

On Wednesday PPI in June was reported as unexpectedly unchanged compared with expectations for a 0.2% rise, while core or underlying prices were flat. The unchanged reading in the PPI, a result of the increase in the cost of goods because of tariffs on imports being offset by weakness in services, followed an upwardly revised 0.3% rise in May, the Labor Department's Bureau of Labor Statistics said. In the 12 months through June, the PPI increased 2.3% after advancing 2.7% in May.

The weakness in the cost of services, if sustained, may indicate that a tariff-induced rise in inflation may not result in broader-based price pressures, thereby allowing the Federal Reserve to resume cutting interest rates later this year.

Fed funds futures traders are now pricing in a 2.6% probability of a July cut, down from 6.2% last week, according to CME Group's FedWatch Tool. A rate cut at September’s Fed meeting now is seen as the next most likely, with a 56.2% probability. Traders are currently pricing in 47 bps of cuts by year-end, less than last week’s 53.1bps.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt was +1 bp to 4.64%. The UK 10-year yield is +1 bp over the past 7 days. On Wednesday it was reported that headline inflation rose to its highest level since January 2024, with consumer price inflation coming in at 3.6% in June. Services inflation held at 4.7%, higher than expected.

Eurozone government bond yields were slightly lower on Wednesday as market participants considered the US inflation figures and latest tariff developments.

Germany's 10-year bond yield experienced a drop of -2 basis points to 2.69%, hovering just below a nearly four-month high of 2.737% reached on Monday. The 30-year yield was +1 bp to 3.21%, having risen to its highest level since October 2023 on Monday at 3.26%. The German 2-year yield was flat at 1.86%.

Over the past seven days week, the German 10-year yield is -1 bp. Germany's two-year bond yield is -2 bps, and on the longer end of the curve, Germany's 30-year yield is -1 basis point.

The spread between US 10-year Treasuries and German Bunds is now about 176 bps, +10 bps more than last week’s 166 bps.

Similarly, Italy's 10-year yield, which serves as the benchmark for the eurozone's periphery, -4 bps to 3.54%. This spread between Italian and German 10-year yields at approximately 85 basis points.The Italian 10-year yield is -1 bp over the past 7 days.

Market participants the ECB to lower rates at its upcoming policy meeting on 24th July, with only bps of easing currently priced in by the end of the year, implying one additional quarter-point reduction.

Commodities

Gold spot +1.76% MTD and +27.51% YTD to $3,352.56 per ounce.

Silver spot +5.43% MTD and +30.41% YTD to $38.14per ounce.

West Texas Intermediate crude +0.15% MTD and -8.34 % YTD to $66.40 a barrel.

Brent crude +2.94% MTD and -7.96% YTD to $68.70 a barrel.

Gold prices are +1.24% this week and +27.51% YTD. On Wednesday, gold prices rose +0.68% to $3,352.56 per ounce as investors worried about US monetary policy following reports that President Trump was going to fire Fed chair Jerome Powell. This worried investors that the Fed would lose independence and hence credibility.

This week, WTI and Brent are -2.92% and -2.12%, respectively. Oil prices were mixed on Wednesday. Brent crude futures concluded the trading session -0.26%, settling at $68.70 per barrel. Similarly, WTI crude was -0.24, closing at $66.40 per barrel. Oil prices have been pressured this week by concerns over the economic impact of US tariffs and growing uncertainty over monetary policy following a Bloomberg report that Trump is likely to fire Powell soon. However, they have been supported by China's better-than-expected economic data and the US' larger-than-expected oil inventory drawdown. US crude inventories fell more than expected by 3.9 million barrels to 422.2 million barrels last week according to the latest Energy Information Administration report. This suggests stronger refinery activity, tighter supply, and increased demand. However, larger than expected builds in gasoline and diesel inventories limited price gains as concerns were raised over weakening demand from summer travel.

EIA weekly report. The latest report showed that US crude oil stockpiles fell by 3.9 million barrels last week, following two large stock builds in the prior weeks. However, gasoline and distillate fuel inventories rose by 3.4 million barrels and 4.2 million barrels, respectively, pointing to weaker demand in the world’s largest oil consumer during the summer travel season.

US crude oil refinery inputs averaged 16.8 million barrels per day during the week ending 11, which was 158 thousand barrels per day less than the previous week’s average. Refineries operated at 93.9% of their operable capacity last week. Gasoline production decreased last week, averaging 9.1 million barrels per day. Distillate fuel production decreased by 109 thousand barrels per day last week, averaging 5 million barrels per day.

Note: As of 5:00 pm EDT 16 July 2025

Key data to move markets

EUROPE

Thursday: Eurozone Harmonised Index of Consumer Prices.

Friday: German Producer Price Index.

Tuesday: ECB Bank Lending Survey.

Wednesday: Eurozone Consumer Confidence.

UK

Thursday: Average Earnings, Claimant Count Rate, Claimant Count Change, ILO Unemployment Rate, and Employment Change.

USA

Thursday: Initial and Continuing Jobless Claims, Philadelphia Fed Manufacturing Survey, Retail Sales, and speeches by Fed Governor Adriana Kugler, San Francisco Fed President Mary Daly, Fed Governor Lisa Cook, and Fed Governor Christopher Waller.

Friday: Building Permits, Housing Starts, Michigan Consumer Expectations Index, UoM 1-year Consumer Inflation Expectations, and UoM 5-year Consumer Inflation Expectations.

Wednesday: Existing Home Sales Change.

CHINA

Monday: PBoC Interest Rate Decision.

JAPAN

Thursday: National CPI.

GLOBAL

Thursday and Friday: G20 Meeting.

Global Macro Updates

Trump’s tariffs haul may mean no TACO. President Trump has been accused of always ‘chickening out’ from his threats, hence the use of the term TACO (Trump always chickens out). He paused the majority of the ‘liberation day’ tariffs after promising as many as 90 deals in 90 days. The 90-day mark came and went a week ago, and there has been just one deal, with Great Britain, and some suggestions of deals with Vietnam and Indonesia. However, he has since stepped up his tariff war. President Trump has now sent letters to more than 20 countries to inform them of new tariff rates that will be applied as of 1 August unless they are willing to negotiate. On Wednesday he stated that he intends to send a single letter telling more than 150 countries what tariff rate they will face.

However, the willingness of the US to actually negotiate lower tariffs may be questioned. As noted by the Wall Street Journal, despite the absence of deals, Trump’s tariffs have shown signs of success for the US President. US revenues from customs duties hit a record high of $64bn in the second quarter, $47bn more than over the same period last year, according to data published by the US Treasury. In June alone, the Treasury collected $27 billion in customs revenue, up $20 billion from a year earlier, a pace that would imply $240 billion more a year.

The threats of retaliatory tariffs have thus far come to little. As noted by the Financial Times, China’s retaliatory tariffs on American imports have not had the same effect, with overall income from custom duties only 1.9% in May 2025 than the year before. There has been limited retaliation from Canada while Mexico has simply decided to go the path of negotiation. The European Union has planned counter-tariffs, but has repeatedly deferred implementation, preferring to negotiate instead. EU trade chief Maros Sefcovic headed to Washington on Wednesday for tariff talks with US Commerce Secretary Howard Lutnick and Trade Representative Jamieson Greer. President Donald Trump has threatened a 30% tariff on imports from the EU from 1 August. EU steel and aluminium imports are already facing a 50% US tariff and cars 25%. When the European Commission published its latest list of potential retaliatory targets on €72bn of goods on Tuesday, it put no specific tariff rates against individual products. There is an apparent unwillingness to rile President Trump further, despite European Commissioner Ursula von der Leyen stating that the threatened level of tariff rates were unacceptable and would end normal trade between two of the world's largest markets.

Some other US trading partners have also decided against responding in kind while negotiating with Trump to avoid even higher threatened tariffs. After all, despite agreeing with the UK and potentially others, over lowering the threatened tariff rates, he has never actually relinquished his 10% “baseline” tariff on almost all imports. Although there continues to be skepticism over whether the new tariff rates will take effect 1 August because of the potentially negative impact they could have on the economy and ultimately Trump’s approval ratings, it seems that President Trump may already be winning the game.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.