Who will control Hormuz?

What to look out for today

Companies reporting on Tuesday, 14 April: BlackRock, Citigroup, Johnson & Johnson, JPMorgan Chase & Co., Wells Fargo & Co.

Key data to move markets today

EU: Spanish Harmonised Index of Consumer Prices and speeches by ECB Chief Economist Philip Lane, ECB Executive Board Member Piero Cipollone and, ECB President Christine Lagarde

UK: BRC Like-for-Like Retail Sales and speeches by BoE External Members Catherine Mann and Megan Greene and BoE Governor Andrew Bailey

US: ADP Employment Change 4-week Average, PPI and speeches by Chicago Fed President Austan Goolsbee, Fed Governor Michael Barr, Boston Fed President Susan Collins and Philadelphia Fed President Anna Paulson

CHINA: Imports, Exports and, Trade Balance

GLOBAL: IMF and World Bank Spring Meeting

Global Macro Updates

Do they or don’t they? Despite unsuccessful negotiations over the weekend and the implementation of a US blockade at the Strait of Hormuz, discussions between Washington and Tehran reportedly remain ongoing.

According to Axios, there continues to be progress in US - Iran dialogue, with both parties actively engaged. Unconfirmed reports from Israeli media indicate that President Trump is seeking to initiate another round of negotiations prior to any potential escalation.

These developments follow the weekend talks, which concluded on Sunday without a permanent ceasefire agreement. Iran has declared that it will reopen the Strait of Hormuz only as part of a comprehensive peace deal, and has refused President Trump's demand to relinquish its enriched uranium. In response, President Trump ordered a blockade of the strait and is reportedly considering further military actions against Iran.

During the weekend negotiations, the US proposed a 20-year moratorium on uranium enrichment, while Iran countered with a significantly shorter, single-digit timeline. Mediators from Pakistan, Egypt, and Turkey are currently working to bridge the gap between the parties and secure an agreement ahead of the 21 April ceasefire deadline, as reported by Axios.

The US blockade of Iranian oil exports has been identified as a new risk for global energy markets. Analysts noted that Iran has continued to export approximately 2 million barrels per day during the conflict, but a full blockade would halt these flows and further constrain global supply.

The conflict provides a short-term boost to the petrodollar. As noted in a The Wall Street Journal opinion piece by well-known China expert and founder of Enodo Economics, Diana Choyleva, America's military re-engagement in the Gulf strikes back against China's patient, structural challenge to dollar oil supremacy, reinforcing the core 1970s bargain that Gulf oil flows in dollars, secured by US force projection. A decisive US outcome would set back Beijing's mBridge platform and yuan-settlement channels that have been quietly eroding that architecture for years.

Yet the underlying pressures on the dollar have not disappeared. Central banks now hold more gold than US Treasuries in reserve, a first since the mid-1990s, having bought over 1,000 tonnes annually since 2022. There has been deliberate diversification away from dollar assets amid sanctions risk and de-dollarisation concerns.

Additionally, US federal debt has surpassed $38 trillion, with interest costs now exceeding defence spending, raising long-term sustainability questions. So although force can delay structural erosion, it cannot resolve the fiscal arithmetic that increasingly tests the dollar's reserve status.

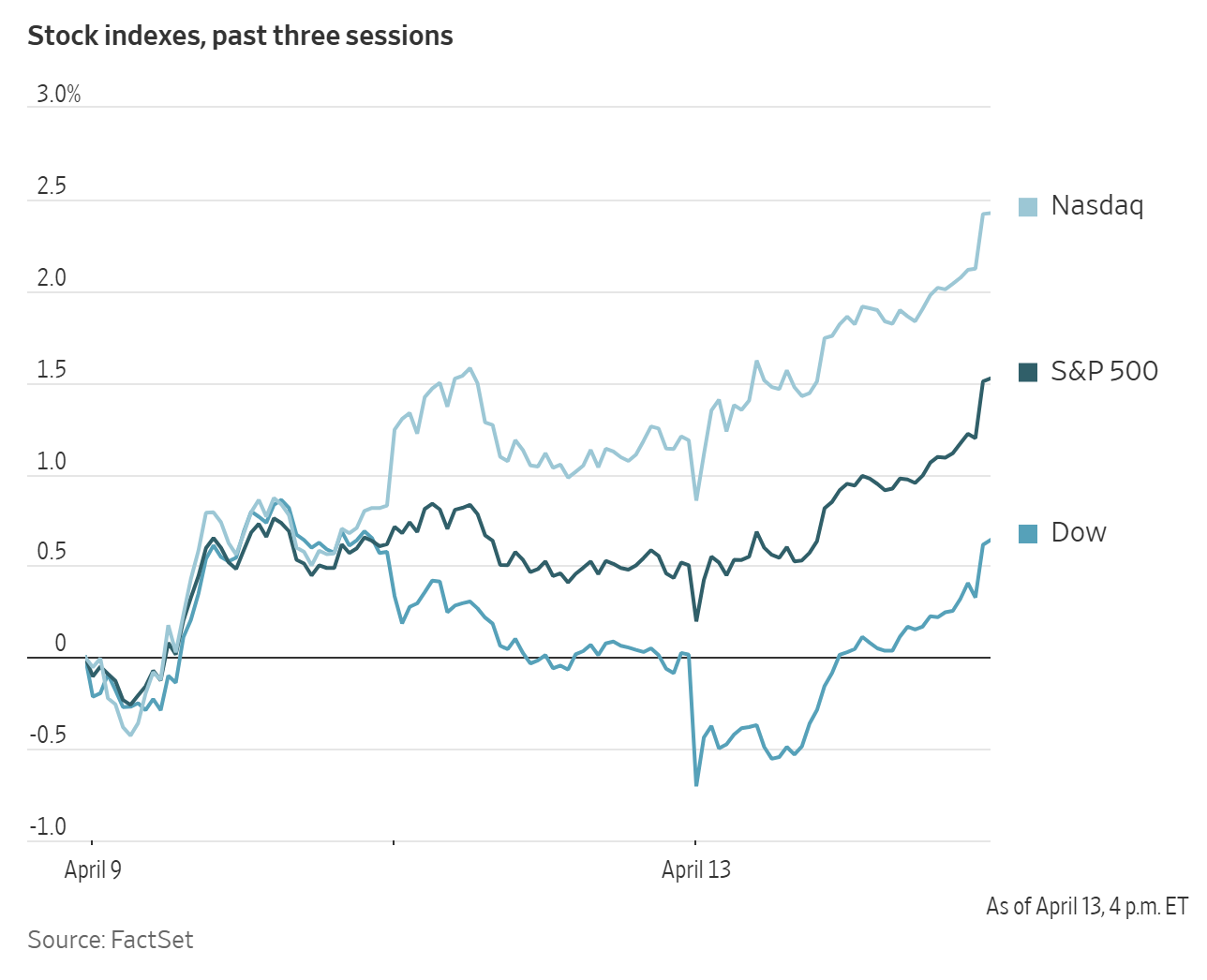

US Stock Indices

Dow Jones Industrial Average +0.63%

Nasdaq 100 +1.06%

S&P 500 +1.02%, with 9 of the 11 sectors of the S&P 500 up

US markets were up on Monday after US President Trump said that Iran wants to make a deal but that he will not come to any agreement that allows Tehran to have a nuclear weapon.

By Monday's close the S&P 500 had erased all its losses after the war with Iran began as it closed 0.1% above its 27 February level. The S&P 500 was +1.02% to 6,886.24, the Dow Jones Industrial Average +0.63% to 48,218.25, and the Nasdaq Composite Index +1.23% to 23,183.74.

In corporate news, Somnigroup International agreed to buy bedding company Leggett & Platt in an all-stock transaction worth about $2.5 billion.

On Monday, Baker Hughes said it will sell its unit, Waygate Technologies, to Sweden-based Hexagon for about $1.45 billion in cash as part of its shedding of non-core assets as it shifts its focus away from traditional oilfield service.

S&P 500 Best performing sector

Financials +1.73%, with KKR & Co +7.59%, Fidelity National Information Services +7.06% and Factset Research Systems +7.00%

S&P 500 Worst performing sector

Utilities -1.19%, with Edison International -4.40%, PG&E -4.32% and Sempra -2.62%

Mega Caps

Alphabet +1.07%, Amazon +0.63%, Apple -0.49%, Meta Platforms +0.74%, Microsoft +3.64%, Nvidia +0.30% and Tesla +0.98%

Information Technology

Best performer: Oracle +12.69%

Worst performer: First Solar -1.53%

Materials and Mining

Best performer: Celanese +8.06%

Worst performer: Newmont -3.64%

Corporate Earnings Reports

Posted on Monday, 13 April

Goldman Sachs +19% quarterly revenue to $17.23 bn vs $16.97 bn estimate

EPS at $17.55 vs $16.49 estimate

David Solomon, Chairman and CEO of Goldman Sachs, said, “Goldman Sachs delivered very strong performance for our shareholders this quarter, even as market conditions became more volatile. Our clients continue to depend on us for high quality execution and insights amid the broader uncertainty, and we remain confident in how we’ve positioned our businesses. The geopolitical landscape remains very complex – so disciplined risk management must remain core to how we operate.”— see report.

European Stock Indices

CAC 40 -0.29%

DAX -0.26%

FTSE 100 -0.17%

Commodities

Gold spot -0.15% to $4,740.57 an ounce

Silver spot -0.40% to $75.58 an ounce

West Texas Intermediate +1.62% to $97.18 a barrel

Brent crude +3.86% to $98.09 a barrel

Gold prices experienced a modest decline on Monday, extending losses from Friday.

Spot gold edged down -0.15% to $4,740.57 ounce despite the US dollar index declining -0.33% to 98.37.

Spot silver declined -0.40% to $75.58 an ounce.

Oil prices climbed during Monday’s trading session, driven by the US military’s implementation of a blockade in the Strait of Hormuz, which intensified concerns about supply disruptions.

Brent crude futures increased by $3.65, or +3.86%, to $98.09 per barrel, while US WTI crude rose by $1.55, or +1.62%, reaching $97.18 per barrel.

After reaching session highs, crude benchmarks moderated following the US President’s statement that Iran had contacted US officials in pursuit of a deal. This development eased the sharp overnight rally, during which WTI had surged over eight percent in premarket trading. The rally had been fuelled by Washington’s commitment to initiate a comprehensive naval blockade of the Strait of Hormuz and his warning of retaliation should Iran resist, subsequent to the breakdown of peace negotiations over the weekend.

In response, Iran threatened to target ports in Gulf-bordering nations, following the collapse of diplomatic talks in Islamabad aimed at resolving the ongoing crisis.

At the ARDA Conference in Cape Town, Vitol, the world’s biggest oil merchant, reported that the US - Israel conflict with Iran has reduced global refining capacity by more than 5 million barrels per day (bpd), with approximately 3 million bpd offline in the Middle East Gulf and an additional 2 – 3 million bpd idled outside the region, largely due to diminished Mideast Gulf crude supplies. Asia-Pacific throughput has been most significantly affected.

In the physical oil market, Gulf tankers have attempted renewed transits through Hormuz by navigating closer to the Iranian coast, while supertankers carrying Iranian crude have anchored off Indian ports, marking the first such arrivals in nearly seven years. According to data and trade analytics firm Kpler, several empty tankers bound for the Persian Gulf reversed course overnight and this morning, opting to avoid the Strait entirely. Bloomberg news reports that Saudi Arabia’s crude shipments to China are expected to decline by roughly half next month as a direct result of the disruption in Hormuz.

According to OPEC’s April Monthly Oil Market Report (MOMR), the organisation reduced its global oil demand forecast for Q2 2026 by 500,000 bpd to 105.07 million bpd, citing the impact of the conflict in Iran. The downward revision affected both OECD and non-OECD regions, while estimates for full-year demand growth in 2026–2027 remained unchanged. OPEC+ output fell sharply in March to 35.06 million bpd as Middle Eastern producers curtailed supply.

Russian crude output remained nearly steady in March at 9.167 million bpd, compared to a downwardly revised 9.164 million bpd in February. This ended three consecutive months of declines, as Ukrainian attacks on oil infrastructure continued to disrupt seaborne exports and crude processing. The figure, which excludes condensate, is 407,000 bpd below Russia’s March OPEC+ quota.

International Energy Agency (IEA) Executive Director Fatih Birol stated that the agency stands ready to draw upon global oil reserves again if necessary, although he expressed hope that a second release could be avoided. This follows last month’s record coordinated release of 400 million barrels, including 172 million barrels from the US Strategic Petroleum Reserve (SPR).

Note: As of 4 pm EDT 13 April 2026

Currencies

EUR +0.31% to $1.1755

GBP +0.29% to $1.3497

Bitcoin +0.01% to $73,218.35

Ethereum -0.18% to $2,251.33

On Monday, the dollar extended its decline for a sixth consecutive session, as financial markets weighed the risks posed by a US blockade of Iranian shipping in the Strait of Hormuz against the potential for a diplomatic resolution between Washington and Tehran.

The dollar index fell -0.33% on Monday, reaching 98.37, its lowest level since 2 March.

The euro appreciated +0.31% to $1.1755, following a +1.77% gain last week. Sterling similarly advanced +0.29% to $1.3497 after posting a +2.04% increase last week, marking its strongest weekly performance since March 2025. In contrast, sterling was little changed against the euro, trading at 87.02 pence.

Money market futures now indicate nearly two quarter-point interest rate hikes by the BoE in 2026. Prior to the onset of the conflict with Iran, investors had anticipated two rate cuts within the year.

The yen edged -0.03% lower to ¥159.34 per dollar. The Japanese currency remains susceptible to selling pressure as concerns grow that Japan's trade balance may deteriorate amid the persistent risk of elevated crude oil prices.

Furthermore, prospects for an interest rate increase this month by the BoJ, previously considered likely, have diminished as waning optimism for a resolution to the Iran conflict continues to fuel market volatility and cloud the economic outlook. Interest rate swaps on Monday reflected a 40% probability of a BoJ rate hike this month, down from 57% recorded on Friday, according to data from Tokyo Tanshi.

Fixed Income

US 10-year Bond -4.7 basis points to 4.293%

German 10-year Bund +3.8 basis points to 3.099%

UK 10-year gilt +4.3 basis points to 4.817%

US Treasuries moved higher across the curve on Monday amid volatile trading, recovering from earlier losses. Market participants appeared largely indifferent to renewed tensions in the Middle East following the US blockade of the Strait of Hormuz.

The blockade was implemented after ceasefire negotiations between Washington and Tehran collapsed over the weekend. In retaliation, Iran threatened to launch strikes against ports in neighbouring Gulf states.

Initially, Treasury yields rose alongside oil prices; however, this momentum later faded. Treasury movements were muted, with analysts noting market fatigue from ongoing headlines.

During afternoon trading, the yield on the 10-year Treasury note declined -4.7 bps to 4.293%, while the 30-year yield fell -1.8 bps to 4.899%.

At the shorter end of the yield curve, the 2-year Treasury yield, closely tied to expectations for the Fed funds rate, also declined, dropping -2.7 bps to 3.783%.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 8.6 bps of rate cuts in 2026, higher than the 0.2 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.5% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 1.0% probability.

On Monday, eurozone government bond yields advanced following the failure of the US and Iran to reach a ceasefire agreement over the weekend. This development prompted traders to increase their expectations that the ECB may raise interest rates in 2026.

Money markets reflected a heightened probability of a 25 bps rate increase in April, rising to 44% from 25% at the close of trading on Friday. The ECB’s deposit facility rate currently stands at 2.0%.

Traders are now projecting an ECB deposit facility rate of approximately 2.68% by year-end, suggesting the likelihood of two rate hikes and a 70% chance of a third, up from 2.60% late last Friday.

German two-year bond yields, sensitive to ECB policy rate expectations, increased +3.9 bps to 2.648%.

Germany’s 10-year government bond yield rose +3.8 bps to 3.099%, approaching the late March peak of 3.130%, which marked the highest level since June 2011.

Boris Vujcic, the incoming ECB vice president, stated on Monday that current energy prices remain closely aligned with the ECB’s baseline scenario and should not significantly impact inflation or growth, according to N1 regional television.

Current ECB Vice President Luis de Guindos emphasised that any future rate increases by the ECB will depend on the extent to which war-driven increases in the cost of crude oil and certain chemicals affect broader price trends.

Italy’s 10-year BTP yields climbed +5.6 bps to 3.886%. The yield spread between Italian BTPs and German Bunds stood at 78.7 bps.

The French spread of 10-year OATs reached 65.1 bps, with the French 10-year yield trading +5.2 bps higher at 3.750%. Fitch reaffirmed its A+ rating for France, maintaining a stable outlook as of Friday.

Note: As of 4 pm EDT 13 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.