How far can central banks drift apart?

Key data to move markets today

EU: German Producer Price Index (PPI) and a speech by Bundesbank President Joachim Nagel

Global Macro Updates

ECB holds rates, warns of inflation risks amid Middle East unrest. The ECB, as anticipated, kept its key interest rates unchanged and reiterated its commitment to a data-driven, meeting-by-meeting approach without pre-committing to a specific rate trajectory. Despite this steady stance, the central bank cautioned about mounting upside risks to inflation and downward pressures on growth, primarily stemming from the ongoing Middle East conflict. Updated macroeconomic projections revealed that headline inflation will remain above target in 2026, nearing the target in subsequent years, while core inflation is expected to stay above target throughout the forecast horizon. These projections may strengthen expectations for a rate hike later this year. Furthermore, staff projections were finalised on 11th March, later than usual. The growth outlook is somewhat softer, with forecasts of 0.9% for 2026, 1.3% for 2027, and 1.4% for 2028. The ECB emphasised that the medium-term effects of higher energy prices will depend on the conflict’s intensity and duration, as well as the scale of indirect and secondary impacts from a more persistent energy shock.

Internally, the ECB is increasingly considering tighter policy measures, with sources cited by Reuters suggesting that discussions around rate hikes could begin as soon as the 29th – 30th April meeting. Although an April move is possible, June is viewed as a more likely timeframe, allowing policymakers greater clarity on energy prices and their overall economic repercussions. The shift in tone reflects how the intensifying Middle East conflict has substantially altered the inflation and growth outlook by driving up energy costs. According to sources, the ECB’s baseline projections may already be outdated, having assumed Brent crude at approximately $81 this year and around $70 in the future, whereas current prices are near $110. An earlier rate hike would likely require a further spike in oil prices, with one source suggesting that levels around $200 per barrel could prompt action. Scenario analysis by the ECB also indicates that a jump to $150 by June would necessitate tighter monetary policy.

BoE signals readiness to act on inflation risks. The BoE maintained its Bank Rate at 3.75%, with a unanimous 9-0 vote, defying market expectations of a 7-2 split. This decision comes amid a significant rise in global energy and commodity prices. The Bank's communication led to a steepening of rate hike expectations, with markets now pricing in 50 bps of increases by the end of the year. The BoE emphasised its readiness to act to ensure that CPI inflation remains aligned with its 2% target, noting that while it cannot control global energy prices, it can facilitate an economic adjustment that achieves sustainable inflation outcomes.

BoE staff estimated that energy prices could add approximately 0.75 percentage points to inflation in Q3, based on oil and gas futures as of 16th March. Should these increases pass through rapidly, including any indirect effects, the CPI could rise to as much as 3.5% in Q3. The Bank continues to anticipate a modest GDP growth of 0.1% to 0.2% for Q1. Members of the Monetary Policy Committee agreed that developments over the next six weeks, particularly regarding the scale and duration of the ongoing conflict and early indications of its economic impact, will be crucial.

The next policy meeting on 30th April will include updated macroeconomic projections. Within the MPC, Governor Andrew Bailey highlighted that the recent period of high inflation has made households and businesses more sensitive to new economic shocks. Other officials pointed to the recent tightening of financial conditions, though uncertainty remains as to whether these measures are sufficient to mitigate upside risks to price stability. While some members saw value in pausing, more dovish members expressed openness to faster rate cuts should inflation risks diminish.

US Stock Indices

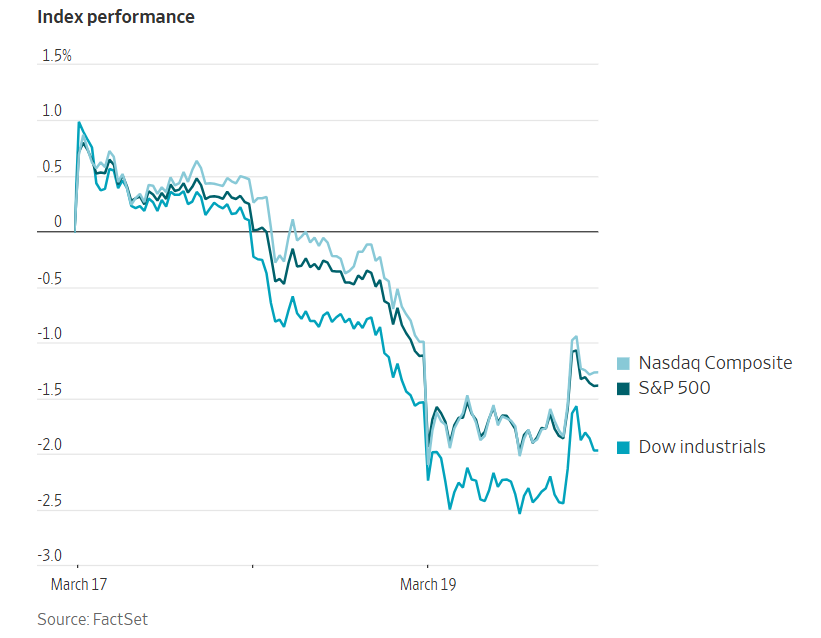

Dow Jones Industrial Average -0.44%

Nasdaq 100 -0.29%

S&P 500 -0.27%, with 8 of the 11 sectors of the S&P 500 down

The sentiment in the stock market continues to deteriorate.

On Thursday, major US indexes declined as investors sharply reduced their expectations for Fed interest rate cuts this year. Renewed attacks on oil and gas facilities in the Middle East heightened concerns that disruptions in energy markets could intensify, thereby driving global inflation higher.

Indexes opened lower and pared losses later in the day. The Dow Jones Industrial Average fell by -0.44%, or 203.72 points, while the Nasdaq Composite and S&P 500 declined by -0.28% and -0.27%, respectively. The Dow now stands approximately 8% below its record high reached in February.

In corporate news, US regulators broadened their investigation into Tesla’s automated driving-assistance system, now covering 3.2 million vehicles.

EcoLab is reportedly close to finalising an acquisition of CoolIT Systems, a data-centre cooling company, from KKR, according to The Wall Street Journal.

A coalition of eight states is seeking to block Nexstar Media’s proposed $6.2 billion acquisition of rival broadcaster Tegna.

Shell announced it is evaluating the extent of damage at its Pearl GTL facility in Qatar after it was targeted by an Iranian attack.

An experimental medicine from Eli Lilly & Co. demonstrated superior weight loss outcomes for diabetic patients compared to any existing drug on the market.

Uber Technologies has revealed plans to invest up to $1.25 billion in Rivian Automotive, in an effort to launch a robotaxi fleet across the US, Canada, and Europe over the next five years.

S&P 500 Best performing sector

Energy +1.48%, with Baker Hughes +5.62%, SLB +5.52%, and APA +3.96%

S&P 500 Worst performing sector

Materials -1.55%, with Newmont -6.89%, Mosaic -5.69%, and International Paper Company -5.29%

Mega Caps

Alphabet -0.19%, Amazon -0.52%, Apple -0.39%, Meta Platforms -1.46%, Microsoft -0.71%, Nvidia -1.02%, and Tesla -3.18%

Information Technology

Best performer: Seagate Technology +6.84%

Worst performer: Fair Isaac -7.52%

Materials and Mining

Best performer: Air Products and Chemicals +0.97%

Worst performer: Newmont -6.89%

European Stock Indices

CAC 40 -2.03%

DAX -2.82%

FTSE 100 -2.35%

Commodities

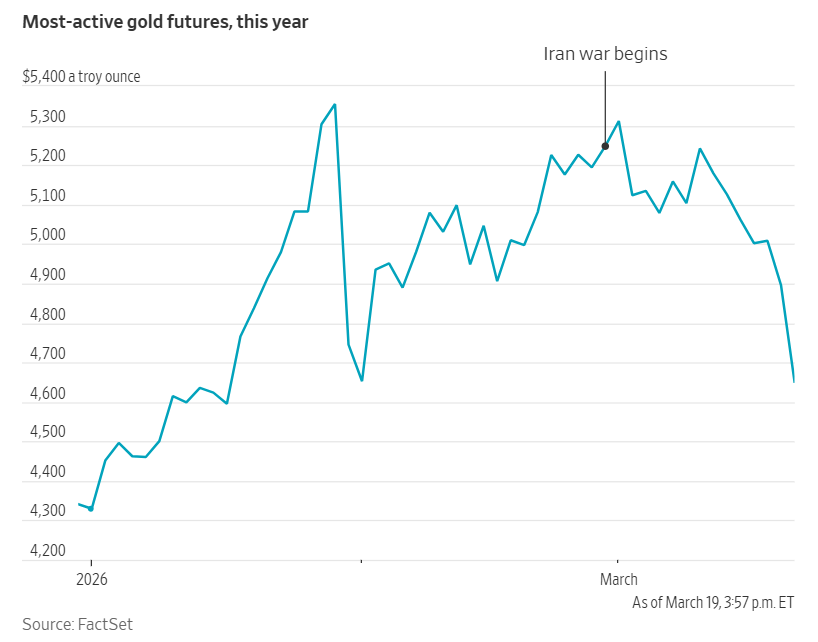

Gold spot -3.42% to $4,652.75 an ounce

Silver spot -3.65% to $72.61 an ounce

West Texas Intermediate -4.73% to $95.10 a barrel

Brent crude -1.72% to $107.76 a barrel

Gold prices declined by more than three percent on Thursday, marking their seventh consecutive day of losses.

Spot gold dropped -3.42% to $4,652.75 per ounce, reaching its lowest level since early February.

Spot silver also declined, falling -3.65% to $72.61 per ounce.

Brent crude declined on Thursday, retreating from session highs of $119 per barrel. US crude futures closed with losses after briefly surpassing $100 per barrel earlier in the day.

Trading was notably volatile following overnight attacks by Iran on energy targets in the Middle East, prompting the US government to implement measures aimed at expanding supply.

Brent futures settled at $107.76 per barrel, down $1.89, or -1.72%. Earlier in the session, Brent had reached $119.13, approaching the three-and-a-half-year peak previously touched on 9th March. US WTI crude ended at $95.10 per barrel, a decrease of $4.72 or -4.73%. Earlier trades saw WTI at $100.02, marking its widest discount to Brent in over a decade.

Trade sources and Reuters data indicated that premiums for Middle East benchmark Dubai and Oman crude reached record highs, approximately $65 per barrel.

Treasury Secretary Scott Bessent stated that the US may soon lift sanctions on Iranian oil currently stranded on tankers, totaling around 140 million barrels. He also noted the possibility of an additional release from the US Strategic Petroleum Reserve.

Israel launched an attack on Iran's South Pars gas field. President Trump clarified late Wednesday that neither the US nor Qatar were involved. South Pars represents the Iranian sector of the world's largest natural gas deposit, which Iran shares with Qatar across the Gulf.

The US President further remarked that Israel would refrain from targeting Iranian facilities in South Pars unless Iran initiated action against Qatar. He warned that any Iranian aggression toward Doha would prompt a US response.

On Wednesday, QatarEnergy reported that Iranian missile strikes on Ras Laffan, the site of Qatar's primary LNG plants and the world's largest, caused significant damage. The attack also impacted Shell’s 140,000 barrel-per-day Pearl gas-to-liquids plant, halting production. As a result, European gas prices surged to their highest levels in more than three years.

Saudi Arabia announced it intercepted four ballistic missiles and thwarted a drone attack targeting a gas facility.

Saudi Aramco’s SAMREF refinery, partly owned by Exxon, located in the Red Sea port of Yanbu, was also subjected to an aerial attack on Thursday. Although oil loadings at the port were temporarily disrupted, operations have since resumed.

Kuwait Petroleum Corporation reported that its Mina al-Ahmadi refinery was struck by a drone, resulting in a limited fire.

Note: As of 4 pm EDT 19 March 2026

Currencies

EUR +1.03% to $1.1582

GBP +1.22% to $1.3428

Bitcoin -1.51% to $70,229.18

Ethereum -2.84% to $2,142.14

On Thursday, the Japanese yen and the euro appreciated while the US dollar weakened against major currencies. This movement occurred as the ECB, BoE, and BoJ maintained their interest rates in response to growing inflation concerns driven by rising oil prices following the conflict in the Middle East.

The US dollar index declined by -1.07% to 99.22, while the euro strengthened by +1.03% against the dollar, reaching $1.1582.

Despite this recent decrease, the index remains close to its ten-month high, attained late last week as the ongoing conflict and surging oil prices prompted investors to seek safety in US assets.

The BoJ opted to keep interest rates unchanged but continued to signal a preference for tighter monetary policy. Consequently, the yen rose +1.31% against the dollar, trading at ¥157.66 per dollar.

Sterling also advanced on Thursday after the BoE decided to leave interest rates steady. The Monetary Policy Committee (MPC) unanimously voted to maintain current borrowing costs, with some members indicating that further rate increases may be considered.

The pound rose by +1.22% against the dollar, reaching $1.3428, after hitting its lowest level since early December during the previous week.

Meanwhile, the euro was slightly weaker against sterling, trading at 0.8628 pence.

The BoE's decision was largely anticipated. According to staff forecasts, the MPC expects inflation to rise as high as 3.5% over the next two quarters and remains vigilant regarding the risk of sustained higher inflation expectations within the economy.

Fixed Income

US 10-year Bond -0.1 basis points to 4.264%

German 10-year +1.5 basis points to 2.963%

UK 10-year gilt +10.4 basis points to 4.784%

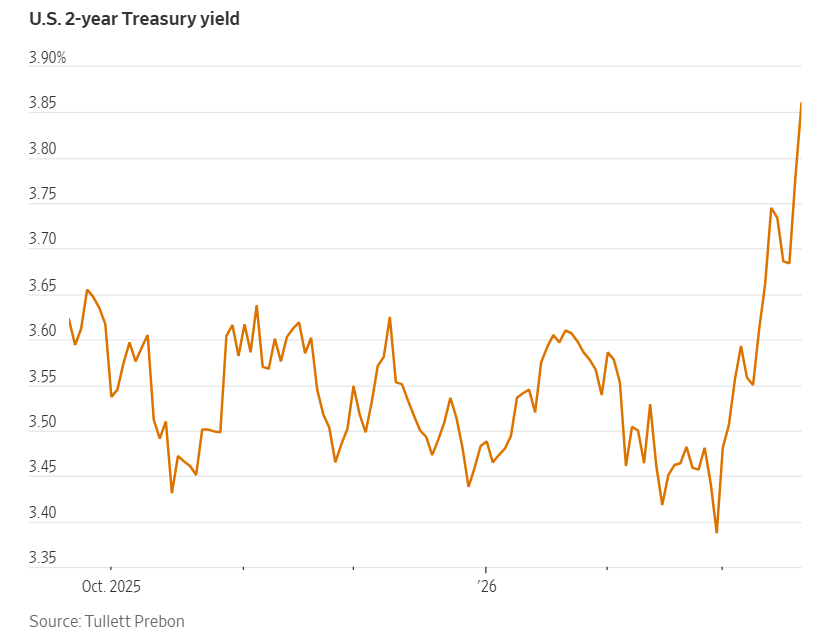

On Thursday, yields on short-term US Treasury securities rose amid volatile trading, reflecting heightened investor expectations regarding the Fed's monetary policy trajectory.

According to the Summary of Economic Projections released on Wednesday after its two-day policy meeting, the Fed anticipates implementing a 25 bps rate cut later this year, with an additional reduction forecasted for 2027.

The two-year Treasury yield, sensitive to shifts in inflation and interest rate expectations, reached 3.960%, marking its highest level since August 2025. However, it subsequently moderated, ending the day up +2.8 bps at 3.807%. In contrast, the 10-year yield edged down by -0.1 bps to 4.264%, after earlier touching its highest point since late August. The US 30-year yield declined by -4.3 bps to 4.843%.

The US yield curve continued to flatten for the fourth consecutive session, with the spread between two-year and 10-year yields narrowing to 45.7 bps from 48.6 bps late on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in just 1.2 bps of cuts in 2026, lower than the 17.5 bps priced in the previous week. Fed funds futures traders are now pricing in a 7.2% probability of a 25 bps rate hike at the 29th April FOMC meeting, up from 0.1% a week ago.

On Thursday, yields on short-dated eurozone government bonds surged as traders anticipated additional interest rate hikes from major central banks. This development occurred alongside a sharp rise in energy prices, driven by the ongoing conflict involving Iran, even as the ECB opted to maintain its borrowing costs unchanged.

The yield on Germany’s two-year Schatz, sensitive to ECB policy expectations, climbed by +19.3 bps to 2.581%.

Money market data indicated that traders have now priced in nearly 70 bps of rate increases for 2026, up from approximately 50 bps on Wednesday. Furthermore, there is a 60% probability of a rate hike being implemented by April.

The ECB, in its Thursday announcement, kept rates steady at 2% and acknowledged that the conflict in the Middle East would likely drive inflation higher in the short term. However, the central bank emphasised that the medium-term effects, its primary concern, would depend on both the intensity and the duration of the hostilities.

German 10-year government bond yields increased by +1.5 bps to 2.963%, just one basis point below their highest level since 2011. At the longer end of the curve, the 30-year German yield declined by -1.7 bps to 3.457%.

The spread between Italian and German 10-year yields widened noticeably, reaching 81.3 bps, the highest level since October, up from 2.2 bps on Wednesday. Italy’s 10-year BTP yield advanced by +3.7 bps to 3.776%.

Italian bonds have shown heightened volatility, reflecting the country’s higher debt burden and its greater dependence on oil and gas within its energy portfolio.

Note: As of 4 pm EDT 19 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.