How vulnerable is Europe to energy shocks?

Corporate Earnings News

Posted on Thursday, 5th March

CostCo Wholesale quarterly revenue -1.1% to $13.81 bn vs $13.88 bn estimate

Adjusted EPS at $2.61 vs $2.47 expected

During the earnings call, Richard Galanti, CFO of Costco, emphasised the company’s commitment to providing value to members through strategic pricing and innovative solutions. He stated, "Our focus on digital transformation and membership growth continues to yield positive results, positioning us well for future expansion."— see report.

Kroger quarterly revenue -1.5% to $30.45 bn vs $30.48 bn expected

Adjusted EPS $2.44 vs. $2.16 expected

During the earnings call, chairman Ronald Sargent said Kroger delivered “another quarter of strong results” and noted that in the final period of the year the company achieved positive market share growth, which he described as its strongest share performance since 2021. He attributed improved trends to price investments made throughout the year, while also pointing to improved shrink and productivity as factors supporting margins.— see report.

Key data to move markets today

EU: German Factory Orders, Eurozone Employment Change, Eurozone GDP, speeches by ECB President Christine Lagarde and ECB Executive Board Members Piero Cipollone and Isabel Schnabel

US: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, Unemployment Rate, U6 Underemployment Rate, Retail Sales, Fed Monetary Policy Report and speeches by San Francisco Fed President Mary Daly, Philadelphia Fed President Anna Paulson, Cleveland Fed President Beth Hammack and Boston Fed President Susan Collins

Global Macro Updates

Europe faces a perfect storm. The conflict with Iran has affected Europe more than initially anticipated, with repercussions extending far beyond immediate hostilities. European gas prices have surged following Qatar’s suspension of LNG production, elevating the Dutch benchmark to its highest point in over a year. The timing of this disruption is especially harmful as EU gas storage levels are currently at just 30%, markedly below the five-year average of 45%, with Germany’s reserves at a precarious 21%.

According to Goldman Sachs, even under a revised baseline, oil at $71 per barrel and gas at €35/MWh, euro area growth will be reduced by 0.2% and headline inflation will increase by 0.4%. In a more severe scenario, with oil at $100 per barrel and gas at €100/MWh, growth could stagnate entirely and inflation may surge by as much as 3.6%, potentially compelling the ECB to consider interest rate hikes. Europe’s open economies remain highly susceptible to geopolitical shocks, with limited capacity to prevent or absorb these disruptions. Elevated sovereign debt levels across France, Italy, Spain, and now Germany, and the expansion of private credit markets toward $2.2 trillion globally, exacerbate the risk that this conflict may intersect with existing financial vulnerabilities before Europe has fully absorbed previous shocks.

Reuters reports that unnamed ECB policymakers have indicated the Governing Council will avoid characterising the inflationary impact of the Iran conflict as transitory and may maintain a lower threshold for policy intervention compared to past episodes. Policymakers remain cautious after previously describing inflationary shocks as transitory, particularly given the eurozone’s reliance on energy imports.

Market analysts note that the recent surge in energy prices has effectively eliminated the prospect of an ECB rate cut despite headline inflation being below target. The consensus is that ECB policy communication will remain prudent. Several ECB officials (Villeroy, Stournaras, Makhlouf, Kocher, and Kazaks) have cautioned against drawing premature conclusions regarding the overall impact. Sell-side economists observe that with inflation still relatively contained, the ECB can afford to exercise patience, though it must remain vigilant.

Spain and the US. The diplomatic standoff between the US and Spain, prompted by Spain’s refusal to allow US military bases on its territory for operations against Iran, has evolved into a trade dispute, with President Trump threatening to sever all trade relations with Spain.

Spain has steadfastly resisted US pressure at every stage. While the rhetoric has been notably combative, analysts emphasise that real implementation will be considerably more complex. Spain’s former Foreign Minister, González, highlighted the self-defeating nature of such threats, noting that the United States currently maintains a trade surplus with Spain, making punitive measures against a favourable trading partner inherently counterproductive.

Ultimately, Spain’s position within the EU means trade policy is determined collectively in Brussels, rather than unilaterally in Madrid. Any unilateral action by the US would likely prompt EU-wide retaliation, including counter-tariffs, heightened regulatory scrutiny of US entities, and possible action before the WTO. Spanish companies could further mitigate the impact by rerouting final processing through other EU member states, thereby complicating enforcement efforts.

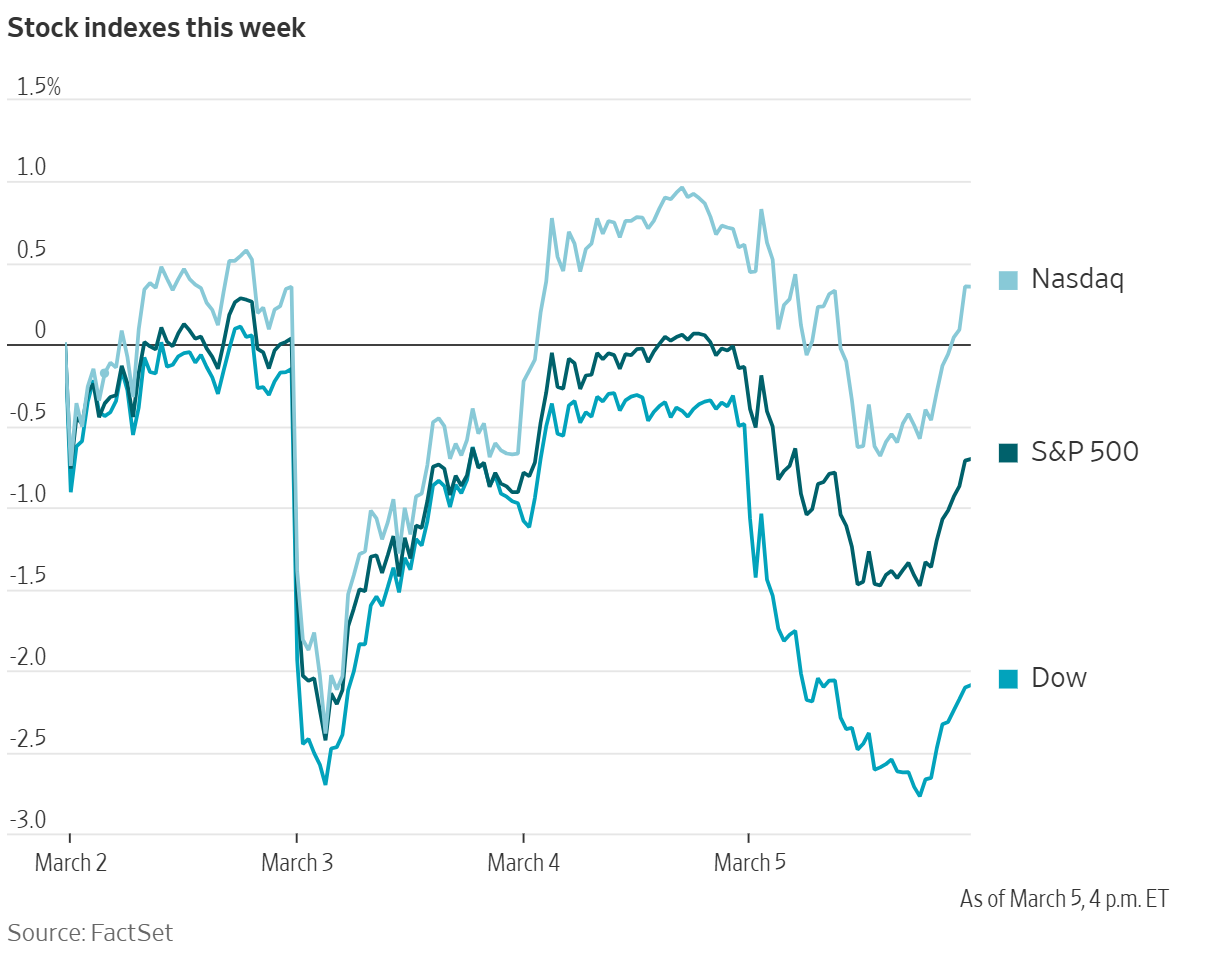

US Stock Indices

Dow Jones Industrial Average -1.61%

Nasdaq 100 -0.29%

S&P 500 -0.56%, with 8 of the 11 sectors of the S&P 500 down

The recent surge in oil prices has driven stock markets lower, further amplifying volatility across global financial markets and raising concerns about potential disruptions to the world economy.

Fears that persistently high oil prices could fuel inflation and dampen global investment have weighed heavily on markets from Tokyo to New York in recent days. On Thursday, stocks and sectors most sensitive to oil prices, interest rates, and overall economic growth experienced the steepest declines, with airlines, banks, industrial firms, and logistics companies particularly affected.

The Dow Jones Industrial Average fell by 785 points, or -1.61%, while the S&P 500 declined -0.56%. The Nasdaq Composite slipped -0.26%.

Major contributors to the Dow's decline included Caterpillar, Goldman Sachs, and Walmart, each falling at least three percent. The Russell 2000 small-cap index, often viewed as a barometer for economic sensitivity, dropped -1.91%.

In corporate news, shares of Nvidia and other semiconductor companies declined after Bloomberg news reported that the Trump administration is drafting regulations that would require US approval for AI chip exports to any destination worldwide. Nvidia recovered by the market's close, finishing up 0.2%, while AMD ended the session more than once percent lower.

Oracle’s shares advanced following news that the company plans to eliminate thousands of jobs to address a cash shortage resulting from its expansion of AI data centres. The software sector outperformed broadly, with Salesforce, Intuit, and ServiceNow each gaining more than four percent.

S&P 500 Best performing sector

Energy +0.59%, with EOG Resources +2.51%, Devon Energy +2.37%, and Chevron +2.08%

S&P 500 Worst performing sector

Consumer Staples -2.43%, with Philip Morris International -5.22%, Walmart -3.52%, and Estee Lauder -3.37%

Mega Caps

Alphabet -0.74%, Amazon +0.98%, Apple -0.85%, Meta Platforms -1.07%, Microsoft +1.35 %, Nvidia +0.16%, and Tesla -0.10%

Information Technology

Best performer: Intuit +6.05%

Worst performer: Corning -6.97%

Materials and Mining

Best performer: LyondellBassell Industries +6.40%

Worst performer: Freeport McMoRan -4.96%

European Stock Indices

CAC 40 -1.49%

DAX -1.61%

FTSE 100 -1.45%

Commodities

Gold spot -1.11% to $5,082.29 an ounce

Silver spot -1.48% to $82.27 an ounce

West Texas Intermediate +5.12% to $78.87 a barrel

Brent crude +1.83 to $84.02 a barrel

Gold fell on Thursday weighed down by a stronger dollar and expectations of higher interest rates.

The US dollar index advanced +0.24%, thereby making dollar-denominated bullion more expensive for international buyers.

Oil prices surged again on Thursday as the de-facto closure of the Strait of Hormuz has left thousands of ships in the Persian Gulf unable to move, meaning Gulf producers are having to slash output as they run out of storage facilities or risk having to close down production.

US WTI crude settled higher by $3.84, or +5.12%, at $78.87 per barrel, marking its highest level since July 2024. Meanwhile, Brent crude finished up $1.51, or +1.83%, at $84.02 per barrel, notching its fifth consecutive session of gains.

The divergence between the two benchmarks was particularly notable around 3:00 PM ET, a departure from their typical synchronised movement, which usually persists unless a specific factor disproportionately affects supply or demand for one of the contracts.

According to a senior White House official, the US Treasury Department is considering action in the oil futures market as part of a broader initiative to counteract rising energy prices, with potential measures set to be announced as early as Thursday.

President Donald Trump, in an exclusive interview with Reuters on Thursday, stated he was not concerned about the spike in US gasoline prices driven by the intensifying Iran conflict, emphasising that the current US military operation remains his top priority. Additionally, President Trump expressed that the US wishes to play a role in the selection of Iran’s next leader.

The conflict has already prompted Iraq and Qatar to halt production of oil and natural gas, respectively, due to maritime gridlock in the Strait of Hormuz. Iraq suspended nearly 1.5 million barrels per day of crude output as storage capacity was exhausted without sufficient tanker traffic, while Qatar ceased its liquefied natural gas (LNG) production for similar reasons. Kuwait and the United Arab Emirates may also be compelled to curtail supply should storage constraints persist.

Tensions heightened further on Thursday as attacks on oil tankers continued in the Gulf. The Bahamas-flagged crude oil tanker Sonangol Namibe reported structural damage following an explosion near Iraq’s Khor al Zubair port.

These ongoing attacks, combined with Chinese efforts to limit fuel exports, have contributed to upward pressure on prices. The refined products market is also showing signs of strain due to reduced exports from the Middle East.

Furthermore, several oil refineries across the Middle East, China, and India have suspended their crude processing operations in response to the conflict in the region.

According to ship tracking data from Vortexa and Kpler, which excludes some of the smallest vessels, approximately 300 oil tankers remain stranded within the Strait of Hormuz, following a near standstill in vessel traffic after the onset of hostilities.

Note: As of 4 pm EST 5 March 2026

Currencies

EUR -0.21% to $1.1607

GBP -0.12% to $1.3356

Bitcoin -3.01% to $71,142.21

Ethereum -3.26% to $2,080.54

On Thursday, the US dollar bounced back strongly after a short dip from its three-month peak.

By afternoon trading, the euro had slipped -0.21% to $1.1607, and the British pound was down -0.12%, ending at $1.3356.

The dollar index climbed by +0.24% to reach 99.04. Expectations for rate cuts from the BoE have diminished, while money markets are increasingly anticipating rate hikes from the ECB as soon as this year.

The dollar also gained +0.34% against the yen, with the exchange rate rising to ¥157.57.

Fixed Income

US 10-year Bond +0.1 basis points to 4.139%

German 10-year +8.8 basis points to 2.845%

UK 10-year gilt +10.5 basis points to 4.481%

US Treasuries fell for a fourth day on Thursday. The intensifying conflict in Iran exerted upward pressure on oil prices, fuelling concerns about rising inflation and tempering expectations for potential Fed rate cuts.

The yield on the 10-year US Treasury note remained largely unchanged, edging up +0.1 bps to 4.139%, after reaching a three-week high of 4.150%. The yield on the 30-year bond fell -0.2 bps to 4.754%, after having climbed to 4.772%, its highest level since 12th February. The two-year US Treasury yield, which is closely linked to interest rate expectations for the Federal Reserve, declined -1.0 bps to 3.583%.

The US yield curve, representing the spread between two- and 10-year Treasury notes, stood at 61.1 bps.

Recent economic indicators suggest persistent price pressures alongside a stable labour market, thereby reducing the likelihood that the Fed will opt to lower interest rates.

According to the Labor Department, initial jobless claims for the week ending 28 February held steady at a seasonally adjusted 213,000, marginally below the forecasted 215,000.

Additional data from the Labor Department revealed that import prices rose by 0.2% last month, in line with expectations, following a revised 0.2% increase in December. A drop in energy product costs was offset by a notable rise in capital goods prices.

Furthermore, worker productivity decelerated to an annualised rate of 2.8% in the fourth quarter, down from a revised 5.2% in the third quarter. Unit labour costs rose by 2.8%, reversing a previous decline of 1.8%.

This data precedes the release of today’s key government payrolls report, which will further influence expectations regarding the Federal Reserve’s policy trajectory.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 35.1 bps of cuts in 2026, lower than the 61.9 bps priced in the previous week. Fed funds futures traders are now pricing in a 2.7% probability of a 25 bps rate cut at the 18th March FOMC meeting, down from 7.4% a week ago.

Eurozone government bonds fell on Thursday, driving up yields, as investor concerns grew over the potential inflationary shock from the widening Middle East war.

The German 10-year Bund yield rose +8.8 bps to 2.845%, its highest since 9th February. The two-year yield, sensitive to shifts in inflation expectations, was +8.80 bps for the day at 2.234%. Italian and French 10-year yields were +13.2 bps and +11.9 bps respectively.

With oil and gas prices soaring, traders have rapidly priced out any prospect of the European Central Bank cutting interest rates this year, given Europe's vulnerability to energy price shocks.

Money markets showed traders are attaching a roughly 40% chance to a rate hike by July, according to LSEG data, having last week seen a chance of a cut this year. No rate change is expected at the ECB meeting on 18th-19th March.

ECB policymakers did warn on Thursday that a prolonged conflict could push up inflation and weigh on growth in the eurozone.

The UK's 10-year gilt yield was +10.5 bps higher.

Note: As of 4 pm EST 5 March 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.