Will politics weigh on Europe’s momentum?

% to 99.40

Key data to move markets today

USA: Michigan Consumer Sentiment and Expectations Indices, UoM 1-year and 5-year Inflation Expectations, and a speech by St. Louis Fed President Alberto Musalem

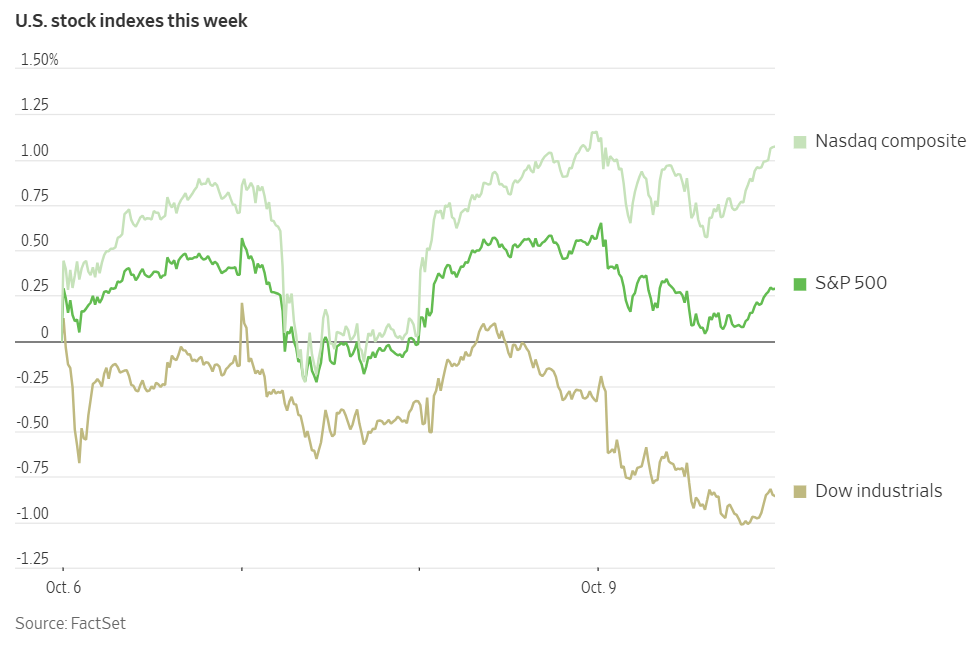

US Stock Indices

Dow Jones Industrial Average -0.52%

Nasdaq 100 -0.15%

S&P 500 -0.28%, with 10 of the 11 sectors of the S&P 500 down

On Thursday, the S&P 500 declined by -0.28% and the Nasdaq Composite fell by -0.08%, following record highs for both indexes on Wednesday. The Dow Jones Industrial Average dropped -0.52%, or 243 points.

With Q3 earnings season set to commence in earnest next week, investors anticipate that corporate results will play a more prominent role in influencing market movements, particularly as major economic data releases remain limited. Analysts project that S&P 500 companies will report an 8% increase in Q3 earnings, which, according to FactSet, would represent the ninth consecutive quarter of y/o/y earnings growth for the index.

In corporate news, US auto safety regulators have launched an investigation into Tesla regarding instances in which vehicles utilising its partial-automation software reportedly drove through red lights and breached other traffic regulations.

UnitedHealth Group announced plans to acquire a Massachusetts medical practice comprising 45 physicians, signalling continued expansion of its Optum division despite recent challenges in the sector.

Delta Air Lines issued an optimistic outlook for sustained robust demand into next year, following Q3 earnings that surpassed expectations, supported by increased spending on premium leisure travel and a rebound in corporate bookings.

Citigroup has declined an offer from Grupo Mexico, led by mining magnate German Larrea, to purchase its Grupo Financiero Banamex unit.

Lyft is collaborating with autonomous vehicle developer Tensor Auto to deploy a fleet of hundreds of robotaxis across Europe and North America beginning in 2027.

Novo Nordisk has also agreed to acquire Akero Therapeutics Inc. for as much as $5.2 billion, aiming to enhance its portfolio in addressing liver diseases associated with obesity.

S&P 500 Best performing sector

Consumer Staples +0.61%, with Kenvue +4.73%, PepsiCo +4.23%, and Costco Wholesale +3.07%

S&P 500 Worst performing sector

Materials -1.52%, with Mosaic -3.88%, Newmont -3.61%, and Ecolab -3.13%

Mega Caps

Alphabet -1.32%, Amazon +1.12%, Apple -1.56%, Meta Platforms +2.18%, Microsoft -0.47%, Nvidia +1.83%, and Tesla -0.72%

Information Technology

Best performer: Oracle +2.89%

Worst performer: Dell Technologies -5.21%

Materials and Mining

Best performer: Albemarle +5.25%

Worst performer: Mosaic -3.88%

European Stock Indices

CAC 40 -0.23%

DAX +0.06%

FTSE 100 -0.41%

Commodities

Gold spot -1.51% to $3,976.92 an ounce

Silver spot +0.48% to $49.12 an ounce

West Texas Intermediate -1.11% to $61.52 a barrel

Brent crude -1.26% to $65.21 a barrel

Gold prices declined by more than 1.5 percentage points on Thursday, falling below the $4,000 per ounce threshold, which had been surpassed for the first time in the previous session. This retreat was driven by a strengthening US dollar and profit-taking by investors in response to the ceasefire agreement between Israel and Hamas.

Spot gold decreased by -1.51%, settling at $3,976.92 per ounce.

The dollar index rose by +0.59%, approaching a two-month high, increasing the cost of dollar-denominated gold for international buyers. Market participants began to scale back their gold holdings as the ceasefire in Gaza took effect, easing tensions in a region historically prone to volatility.

The ceasefire agreement, signed on Thursday by Israel and Hamas, marks the initial phase of President Trump’s initiative to end the conflict in Gaza.

On Wednesday, bullion prices had surged past $4,000 per ounce for the first time, reaching a record high of $4,059.05. The rally has been supported by heightened geopolitical risk, strong purchases by central banks, increased inflows into gold-backed exchange-traded funds, expectations of lower US interest rates, and economic uncertainty related to US tariffs.

Oil prices declined on Thursday following the announcement of a ceasefire agreement between Israel and the Palestinian militant group Hamas in Gaza. Brent crude futures settled lower by $0.83, or -1.26%, at $65.21 per barrel, while US WTI crude decreased by $0.69, or -1.11%, to close at $61.52 per barrel.

In addition, OPEC+ announced on Sunday a smaller-than-anticipated increase in oil production for November, which alleviated concerns about potential oversupply in the market.

The US also imposed sanctions on approximately 100 individuals, entities, and vessels, including an independent Chinese refinery and a crude oil terminal, for facilitating Iran’s oil and petrochemical trade. The Treasury Department specifically targeted Shandong Jincheng Petrochemical Group, an independent teapot refinery in Shandong Province, which has reportedly purchased millions of barrels of Iranian oil since 2023. Furthermore, sanctions were levied on Rizhao Shihua Crude Oil Terminal, a China-based facility operating at Lanshan Port, which has received more than a dozen vessels from Iran’s so-called “shadow fleet” that circumvent sanctions. Among these tankers are Kongm, Big Mag, and Voy, which have transported several million barrels of Iranian oil to Rizhao.

The US government maintains that Iran’s oil networks provide funding for Tehran’s nuclear and missile programmes, as well as support for militant proxies across the Middle East. Iran, however, asserts that its nuclear programme serves peaceful purposes. This marks the fourth round of US sanctions targeting China-based refineries that continue to purchase Iranian oil.

Note: As of 5 pm EDT 9 October 2025

Currencies

EUR -0.55% to $1.1563

GBP -0.76% to $1.3298

Bitcoin -1.43% to $121,524.12

Ethereum -3.68% to $4,358.87

The Japanese yen fell to its lowest level against the dollar since mid-February on Thursday, following market concerns over the newly elected leader of Japan's ruling party, Sanae Takaichi, and her stance on currency policy. Although Takaichi expressed that she did not intend to trigger excessive depreciation of the yen—prompting a brief rally—the currency soon returned to its intraday lows. She acknowledged that ‘there are pros and cons to a weak yen.’

The dollar last traded +0.26% higher at ¥153.02, after reaching an intraday peak of ¥153.23, the highest since 13th February. The yen has come under additional pressure this week amid speculation that Takaichi may pursue more expansionary fiscal policies. However, its decline has moderated as investors assess the extent of her ability to stimulate the economy. Takaichi emphasised that monetary policy decisions rest with the BoJ, but also noted that such decisions must align with the government's objectives.

The euro depreciated following the resignation of French Prime Minister Sébastien Lecornu and his government on Monday, an event that has heightened political uncertainty and posed additional challenges to approving a budget designed to address the country's growing deficit. President Emmanuel Macron’s office announced on Wednesday that a new prime minister would be appointed within 48 hours.

According to minutes from the ECB 10th – 11th September meeting, policymakers agreed that the ECB’s policy framework remains robust and allows for a measured approach until there is greater clarity on inflation prospects. The euro was last down -0.55% at $1.1563, having touched a low of $1.1545, the weakest level since 5th August.

The dollar index climbed +0.59% to 99.40, marking its highest reading since 1st August, supported by more hawkish commentary from Fed officials. Minutes from the FOMC September meeting indicated that while risks to the US labour market have increased sufficiently to justify a potential rate cut, policymakers remain cautious due to persistent inflationary pressures.

Sterling also weakened on Thursday, despite comments from BoE policymaker Catherine Mann suggesting that interest rates could remain elevated for an extended period, noting that inflation expectations in the UK remain too high. Markets are now fully pricing in a 25 bps rate cut by the BoE in April, as concerns grow over the British economy and the upcoming budget. Sterling was last down -0.76% at $1.3298, the lowest since 26th September, and also declined against both the euro and the yen as investors paused after a four-day rally. The pound slipped -0.05% to 86.82 pence per euro and fell -0.35% to ¥204.20, after having reached a 15-month high of ¥205.08 the previous day.

Fixed Income

US 10-year Treasury +1.0 basis points to 4.144%

German 10-year bund +2.0 basis points to 2.702%

UK 10-year gilt +2.8 basis points to 4.749%

US Treasury yields remained relatively stable on Thursday, inching marginally higher as uncertainty surrounding the ongoing federal government shutdown persisted. This continued impasse has contributed to a subdued market environment, with participants largely adopting a wait-and-see approach. Despite a generally well-received auction of long-term bonds, market direction was little affected.

Both two-year and 10-year Treasury yields have been confined to a narrow range since lawmakers failed to reach consensus on spending legislation prior to the 30th September deadline. At the time of this writing, there is scant evidence suggesting a resolution to the stalemate is imminent. The two-year yield increased by +1.2 bps to 3.605%, while the 10-year yield rose by +1.0 bps to 4.144%.

Yields on 30-year Treasury bonds were slightly higher for the day at 4.724%, after a modest increase of +0.2 bps compared to Wednesday. This followed a $22 billion US Treasury sale of 30-year bonds, which demonstrated robust investor demand. The auction attracted record-high interest from end-users, and the proportion allocated to primary dealers reached an all-time low, indicating limited reliance on dealer support amidst strong appetite from investors.

Nevertheless, the bond was priced at a high yield of 4.734%, marginally above the expected rate at the bid deadline. The bid-to-cover ratio was 2.38x, consistent with the previous month's results and the historical average. The yield spread between two- and 10-year Treasury notes narrowed slightly to 53.9 bps, compared with 54.1 bps at the close of trading on Wednesday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in a 94.1% probability of a 25 bps rate cut at October’s FOMC meeting, lower than last week’s 98.3%. Traders are currently anticipating 70.7 bps of cuts by year-end, higher than the 69.1 bps expected last week.

Across the Atlantic, eurozone bond yields displayed a mixed performance on Tuesday, following the unexpected resignation of French Prime Minister Sébastien Lecornu, which has intensified the ongoing political crisis in the region’s second-largest economy.

The yield on Germany’s 10-year bond declined by -1.1 bps to 2.712%, while the French 10-year government bond increased slightly by +0.3 bps to 3.577%.

This movement widened the spread between the safe-haven German Bunds and French 10-year government bonds to 86.5 bps, representing a 1.4 bps expansion from the previous session. Notably, the spread had reached 87.96 bps on Monday, marking its highest level since 13th January.

The yield on the 30-year German bond dipped slightly by -0.2 bps to 3.296%. On the shorter end of the curve, the 2-year German yield rose marginally by +0.5 bps to 2.014%.

Additionally, Italy’s 10-year government bond yield declined by -0.6 bps to 3.540%, narrowing the spread between Italian and German 10-year yields by 0.5 bps to 82.8 bps.

Note: As of 5 pm EDT 9 October 2025

Global Macro Updates

ECB September minutes; flexibility and caution prevail. The minutes from the September ECB meeting offered limited guidance regarding the future direction of monetary policy. The discussion revealed that while several officials expressed concerns about downside risks to inflation, others cautioned about potential upside risks. Nevertheless, all members agreed to maintain the current policy stance.

Given that the outlook remains more uncertain than usual, with risks to both inflation and growth, the Governing Council emphasised the importance of preserving maximum flexibility and remaining ready to respond swiftly to significant shocks. The minutes underscored a careful, neutral, and non-committal approach in official communications.

The ECB reiterated its commitment to a data-dependent strategy, clarifying that policy should not be adjusted merely to moderate short-term fluctuations around the inflation target. With ECB staff projecting that inflation will fall notably below target next year, President Lagarde may face questions regarding the extent of tolerance should inflation deviate further from the goal. It was considered that keeping policy unchanged would provide the necessary time to evaluate tariffs, uncertainties, and other risk factors. At the same time, some members argued that the current rate levels are robust enough to manage shocks.

Eurozone money markets are currently pricing in no policy changes for the remainder of the year and only about 10 bps of easing by June 2026.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.