When will the tariff threats stop?

Corporate Earning Calendar 10 July - 16 July 2025

Thursday: Delta Air Lines

Tuesday: BlackRock, Citigroup, JPMorgan Chase & Co., Wells Fargo & Co. Bank of New York Mellon, State Street Corporation

Wednesday: Bank of America, Goldman Sachs, Johnson & Johnson, Morgan Stanley, PNC Financial Services Group, Prologis, Crown Castle, Las Vegas Sands, United Airlines Holdings

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +0.82% MTD and +8.82% YTD

Dow Jones Industrial Average +0.33% MTD and +3.99% YTD

NYSE +0.87% MTD and +7.91% YTD

S&P 500 +0.94% MTD and +6.49% YTD

The S&P 500 is +0.58% over the past week, with 7 of the 11 sectors up MTD. The Equally Weighted version of the S&P 500 is +0.22% over this past week and +5.48% YTD.

The S&P 500 Energy is the leading sector so far this month, +3.99% MTD and +3.01% YTD, while Communication Services is the weakest sector at -1.01% MTD and +9.51% YTD.

Over this past week, Information Technology outperformed within the S&P 500 at +1.80%, followed by Energy and Industrials at +1.44% and +1.18%, respectively. Conversely, Consumer Staples underperformed at -1.34%, followed by Real Estate and Financials at -0.87% and -0.49%, respectively.

The equal-weight version of the S&P 500 was +0.31% on Wednesday, underperforming its cap-weighted counterpart by 0.30 percentage points.

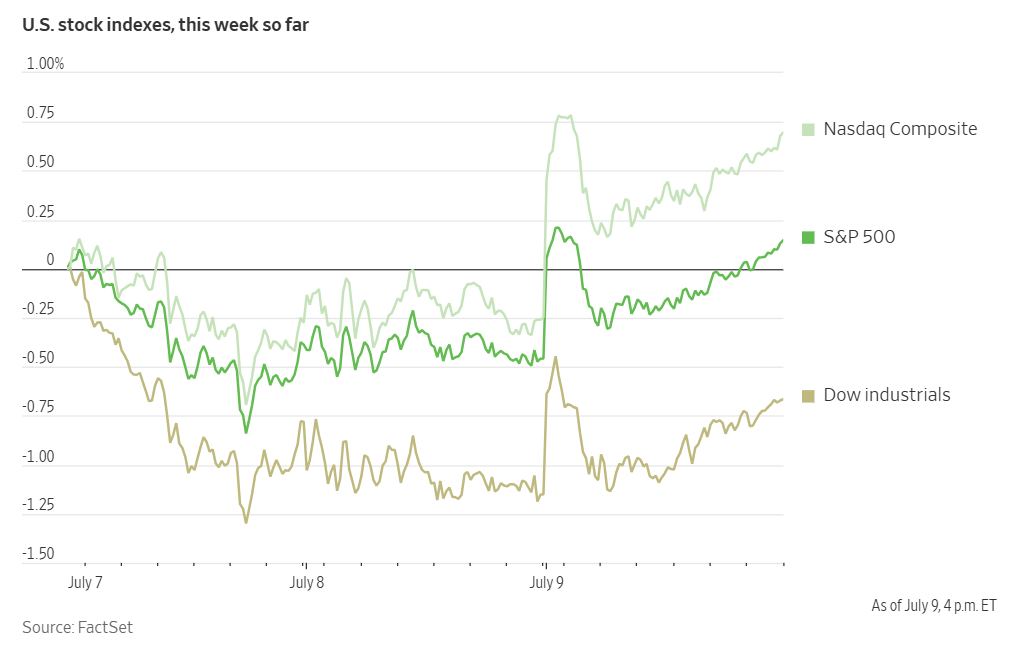

US equities closed higher on Wednesday, with major indices recovering some of their weekly losses. The Dow Jones Industrial Average gained +0.49%, the S&P 500 rose +0.61%, the Nasdaq Composite climbed +0.94%, and the Russell 2000 saw a +1.07% increase.

After Wednesday's advance, the S&P 500 and Nasdaq are now only slightly down for the week, with the S&P 500 sitting approximately 0.3% below its record close.

A measure from BNP Paribas indicates that equity positioning among investors, including commodity-trading advisors, volatility-target funds, and hedge funds, has been consistently increasing and is currently just above neutral. This follows a months-long rally that saw the S&P 500 surge to new highs after skirting a bear market. According to the bank, the last time institutions held such a light position in stocks during a sharp recovery was in 2023.

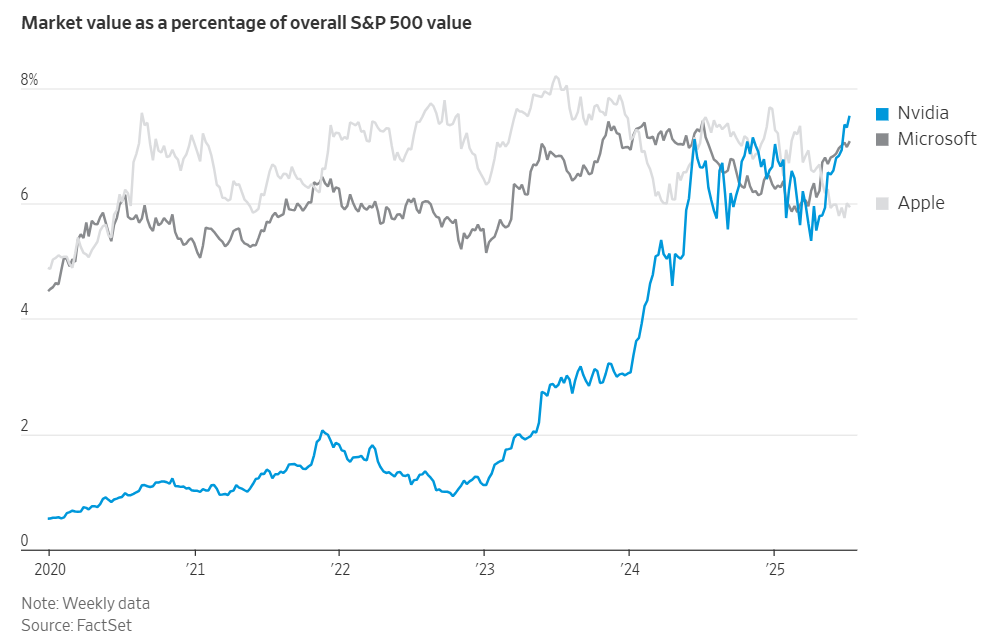

In corporate news, on Wednesday Nvidia became the first company to hit a $4tn market capitalisation. As noted by the Financial Times, Nvidia’s share price has risen by more than 40% since early May after US President Trump agreed a trade deal with China and Nvidia struck a series of multibillion-dollar chip deals in the Middle East.

France's antitrust regulator has reportedly informed Meta Platforms of a potential violation of competition rules concerning the online advertising sector.

Merck has agreed to acquire respiratory drugmaker Verona Pharma for approximately $10 billion. This move is part of Merck's strategy to address the significant revenue gap anticipated in the coming years due to the patent expiration of its cancer immunotherapy drug, Keytruda.

Autodesk is reportedly considering acquiring PTC, a rival engineering-software provider, according to sources familiar with the matter.

Starbucks has received proposals from potential investors for its China business. Bids for Starbucks China have valued it at up to $10 billion, three people familiar with the deal process told CNBC. Starbucks is in the process of evaluating the offers, deal structure proposals and post-sale value creation pitches from bidders.

AES, a provider of renewable power to major tech companies like Microsoft, is exploring various options, including a potential sale, amid takeover interest, according to individuals with knowledge of the matter, as reported by Bloomberg news.

Mega caps: The Magnificent Seven had a mixed performance this week with Tesla shares being particularly hit by increased political risk following its CEO Alon Musk’s decision to create a new political party in the US. This week Nvidia is +3.58%, Microsoft +2.53%, Meta Platforms +2.69%, and Amazon +1.19%, while Apple -0.61%, Alphabet -1.13%, and Tesla -6.26%.

Energy stocks had a mostly positive performance this week, with the Energy sector itself +1.44%. WTI and Brent prices are +2.05% and +1.45%, respectively, this week. Over this past week Hess +5.13%, APA +4.93%, Occidental Petroleum +3.73%, Chevron +3.41%, Phillips 66 +3.20%, Marathon Petroleum +2.76%, ExxonMobil +2.48%, Halliburton +1.52%, BP +1.34%, Shell +0.44%, and ConocoPhillips +0.10%, while Baker Hughes -1.26%, and Energy Fuels -10.42%.

Materials and Mining stocks had a mixed performance this week, with the Materials sector +0.02%. Over the past seven days, CF Industries +5.22%, Albemarle +4.12%, Yara International +3.20%, Nucor +0.60%, Sibanye Stillwater +0.51%, while Freeport-McMoRan -0.39%, Mosaic -1.30%, and Newmont Corporation -2.18%.

European Stock Indices Price Performance

Stoxx 600 +1.59% MTD and +8.34% YTD

DAX +2.68% MTD and +23.31% YTD

CAC 40 +2.77% MTD and +6.74% YTD

IBEX 35 +1.88% MTD and +22.94% YTD

FTSE MIB +0.98% MTD and +17.54% YTD

FTSE 100 +1.06% MTD and +8.33% YTD

This week, the pan-European Stoxx Europe 600 index is +1.62%. It was +0.78% on Wednesday, closing at 549.96.

So far this month in the STOXX Europe 600, Banks is the leading sector, +3.60% MTD and +33.70% YTD, while Utilities is the weakest at -0.99% MTD and +16.11% YTD.

This week, Banks outperformed within the STOXX Europe 600, at +4.37%, followed by Insurance and Technology at +3.10% and +2.74%, respectively. Conversely, Basic Resources underperformed at -1.52%, followed by Food & Beverages and Utilities at -0.99% and -0.60%, respectively.

Germany's DAX index was +1.42% on Wednesday, closing at 24,549.56. It was +3.19% for the week. France's CAC 40 index was +1.44% on Wednesday, closing at 7,878.46. It was +1.81% over the past week.

The UK's FTSE 100 index was +0.91% over the past week to 8,854.18. It was +0.54% on Wednesday.

In Wednesday's trading session, in the STOXX Europe 600 index, optimism surrounding EU-US trade talks propelled Banks to the forefront as the session's top performers. The energy sector also exhibited robust growth, driven by an uptick in oil prices and favorable corporate announcements. Hunting initiated a $40 million share repurchase program and revised its dividend growth target upwards, while Aker Solutions successfully secured a substantial contract with Equinor.

The Industrial Goods & Services sector experienced an upswing, bolstered by positive momentum within the aerospace, defence, and broader industrial segments. Individual notable performances include Airbus, whose shares rose following the reporting of strong June order figures. Renk Group shares appreciated amidst considerations for the sale of its civilian unit, and Kongsberg Gruppen shares surged after surpassing Q2 EPS expectations.

The Personal & Household Goods sector likewise performed well, with particular attention on EssilorLuxottica after Meta Platforms acquired a 3% stake, interpreted as a vote of confidence in smart glasses technology.

Conversely, Basic Resources is among the most pronounced decliners, adversely affected by the proposed 50% copper tariff. Health Care also under pressure due to prospective US pharmaceutical tariff threats. Media underperformed, with WPP experiencing a considerable decline after it revised its annual guidance downwards.

According to LSEG I/B/E/S data as of 8 July second quarter earnings are expected to decrease 0.2% from Q2 2024. Excluding the Energy sector, earnings are expected to increase 2.4%. Second quarter revenue is expected to decrease 3.0% from Q2 2024. Excluding the Energy sector, revenues are expected to decrease 0.4%.

Four companies in the STOXX 600 have reported earnings to date for Q2 2025 as of 8 July. Of these, 25.0% reported results exceeding analyst estimates. In a typical quarter 54% beat analyst EPS estimates. As of 8 July four companies in the STOXX 600 have reported revenue to date for Q2 2025. Of these, 75.0% reported revenue exceeding analyst estimates. In a typical quarter 58% beat analyst revenue estimates.

The STOXX 600 surprise factor is 6.3%, which is which is below the 5.7% long-term (since 2012) average surprise factor. The estimated earnings growth rate for the STOXX 600 for Q2 2025 is -0.2%. The forward four-quarter price-to-earnings ratio (P/E) for the STOXX 600 sits at 14.2x, slightly below the 10-year average of 14.3x.

During the week of 14th July 50 companies are expected to report quarterly earnings.

Other Global Stock Indices Price Performance

MSCI World Index +0.09% MTD and +8.69% YTD

Hang Seng -0.59% MTD and +19.30% YTD

The MSCI World Index was +0.49% over the past 7 days.

The Hang Seng Index was -1.36% over the past 7 days as traders worried about China’s deflationary trend becoming even more entrenched, limiting the nation’s growth prospects. Producer prices in China fell by 3.6% y/o/y in June, marking the 33rd straight month of declines and the steepest drop in more than two years.

Currencies

EUR -0.48% MTD and +13.62% YTD to $1.1722.

GBP -1.04% MTD and +9.92% YTD to $1.3586.

The dollar maintained its position near a two-week high against the yen on Wednesday. This followed the US President announcing new tariffs targeting seven countries, following earlier impositions this week of 25% tariffs on Japan and other trade partners. These new tariff rates are set to take effect on 1 August.

However, the dollar index remains down by -10.57% year-to-date. The dollar index was -0.06% to 97.47 on Wednesday. It is +0.77% this week, and +0.79% so far MTD.

The euro remained stable on Wednesday at $1.1722, as investors cautiously assessed the likelihood of the EU avoiding a tariff imposition and potentially securing exemptions from the baseline US tariff rate of 10%. The euro registered a weekly loss of -0.62% against the US dollar.

Sterling edged +0.01% up against the US dollar on Wednesday, settling at $1.3586. It strengthened +0.17% against the euro to 86.14 pence. For the week, the British pound is -0.49% versus the US dollar.

Analysts suggest the pound has been a notable beneficiary of the US dollar sell-off. This is primarily attributed to the UK's position as the first economy to establish a trade deal framework with the US, thereby diminishing its susceptibility to new tariffs. The British pound is +9.92% against the dollar so far this year and is on track for its most significant annual increase since 2017.

The BoE's half-yearly assessment of financial stability threats highlighted that risks to financial markets remain elevated amidst the backdrop of US tariffs. Furthermore, policymakers eased the cap on lending to riskier borrowers, responding to a government directive for regulators to explore avenues for stimulating economic growth without compromising financial system stability.

The dollar declined by -0.16% to ¥146.30 on Wednesday. This came after touching an intraday high of ¥147.19 earlier in the session. Despite this daily dip, the US currency has recorded a +1.85% gain this week, marking its most substantial weekly rise since mid-December. The Japanese currency is -1.63% MTD and -7.63% YTD.

Export-dependent Japan stands out among major US trading partners as multiple rounds of negotiations have yet to yield a breakthrough, with Japanese policymakers increasingly focused on a critical upcoming election.

Note: As of 5:00 pm EDT 9 July 2025

Cryptocurrencies

Bitcoin +3.67% MTD and +19.04% YTD to $111,102.00.

Ethereum +11.07% MTD and -17.10% YTD to $2,764.30.

Bitcoin is +2.06% and Ethereum +7.48% over the past 7 days. On Wednesday Bitcoin briefly hit a new all-time high of $112,152 before falling back to end the day +2.17% to $111,102.00. Ethereum was +6.15% to $2,764.30.

Bitcoin has benefited this week from an increase in risk appetite as the US administration's new tariff date of 1 August has slightly eased concerns about volatility. It has also been supported by persistent institutional demand.

Spot Bitcoin ETF AUM continues to rise, sitting around $146 billion according to The Block. Interest in these crypto ETFs continues to grow, with even the Trump Media & Technology Group wanting to launch a crypto ETF. The company filed an S-1 form with the SEC this week to launch the "Crypto Blue Chip ETF." This new fund would hold Bitcoin, Ethereum, Solana, and other crypto tokens.

Note: As of 5:00 pm EDT 9 July 2025

Fixed Income

US 10-year yield +11.2 bps MTD and -2.36 bps YTD to 4.340%.

German 10-year yield +6.9 bps MTD and +30.7 bps YTD to 2.676%.

UK 10-year yield +11.8 bps MTD and +3.8 bps YTD to 4.606%.

US Treasury yields declined on Wednesday, following robust demand for a $39 billion auction of 10-year notes. This strong reception suggests that earlier concerns regarding potential investor disengagement from the market may be unfounded.

The 10-year notes were priced with a high yield of 4.362%, approximately half a basis point below their trading level prior to the sale. The bid-to-cover ratio registered at 2.61x, marking its highest level since April.

In contrast, a $58 billion auction of three-year notes conducted on Tuesday garnered somewhat softer interest. The Treasury is scheduled to offer $22 billion in 30-year bonds today.

The yield on benchmark US 10-year notes ended Wednesday -7.0 bps, settling at 4.340%. The yield on the interest rate-sensitive two-year note was -5.4 bps to 3.849%, while the 30-year yield was -5.9 bps to 4.871%.

For the week, the yield on the 10-year Treasury note is +5.6 bps. The yield on the 30-year Treasury bond is +6.0 bps. On the shorter end, the two-year Treasury yield is +5.2 bps this week.

The US President issued final tariff notices to seven minor trading partners on Wednesday, as his administration moved closer to a potential trade agreement with its largest trading partner, the EU. The prospect of elevated price pressures stemming from these tariffs is likely to keep the Fed from cutting rates, particularly given the relatively solid condition of the labour market.

Minutes from the FOMC 17th - 18th June meeting, released on Wednesday, indicated that only ‘a couple’" of officials believed that interest rates could be lowered as early as this month. The majority of policymakers, however, continued to express some degree of concern regarding inflationary pressures that could arise from the tariffs, as well as slower economic growth going forward.

Fed funds futures traders are now pricing in a 6.7% probability of a July cut, down from 23.8% last week, according to CME Group's FedWatch Tool. A rate cut at September’s Fed meeting now is seen as the next most likely, with a 69.0% probability. Traders are currently pricing 53.1 bps of cuts by the end of the year, less than last week’s 64.4 bps.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt was -3.0 bps to 4.606%. The UK 10-year yield is -1.1 bps over the past 7 days.

Eurozone government bond yields exhibited minimal change on Wednesday, as investors appeared to largely absorb the US President's intentions for additional import levies, on a day that also marked the scheduled expiration of his initial 90-day tariff pause. Late on Tuesday, President Trump broadened his trade agenda, threatening a 50% tariff on imported copper and new levies on the pharmaceutical and semiconductor industries.

In response, the EU stated on Wednesday that it anticipates reaching an outline trade framework with the US in the coming days. Despite this, the US President further indicated that he would issue additional tariff notices to unnamed countries, leaving bond investors in Europe (and the rest of the world) in a ‘wait-and-see’ mode.

Germany's 10-year bond yield experienced a modest decline of -1.6 bps, settling at 2.676%. It had reached its highest level since 16th May on Tuesday, at 2.668%. The 30-year yield was marginally lower by -0.1 bps at 3.165%, while the German 2-year yield was -1.9 bps to 2.858%.

For the week, the German 10-year yield is +4.9 bps. Germany's two-year bond yield is -1.3 bps, and on the longer end of the curve, Germany's 30-year yield is +6.7 bps this week.

The spread between US 10-year Treasuries and German Bunds is now 166.4 bps, 0.7 bps higher than last week’s 165.7 bps.

Similarly, Italy's 10-year yield, which serves as the benchmark for the eurozone's periphery, also fell by -1.6 bps to 3.522%. This movement maintained the spread between Italian and German 10-year yields at approximately 84.6 basis points, a 3.8 bps contraction from the preceding week. Italian 10-year yields are up +1.1 bps over the past 7 days.

Monetary policy expectations within the eurozone have remained stable, subsequent to the ECB’s indication that it would pause its rate-cutting cycle. This follows 200 bps of easing implemented since the middle of last year.

Market participants do not anticipate the ECB to lower rates at its upcoming policy meeting on 24th July, with only 23 bps of easing currently priced in by the end of the year, implying one additional quarter-point reduction.

Commodities

Gold spot +0.33% MTD and +26.43% YTD to $3,313.35 per ounce.

Silver spot +0.78% MTD and +25.98% YTD to $36.37 per ounce.

West Texas Intermediate crude +5.18% MTD and -4.92% YTD to $68.25 a barrel.

Brent crude +3.70% MTD and -5.96% YTD to $70.13 a barrel.

Gold prices are -1.27% this week and +26.43% YTD. On Wednesday, gold prices increased slightly as investors kept a close eye on ongoing trade negotiations between the US and its global partners. Spot gold climbed +0.39% to reach $3,313.35 per ounce.

Spot gold +0.39% on Wednesday to $3,313.35 per ounce, recovering after hitting its lowest point since 30th June earlier in the day. This modest rise occurred even as the US dollar remained near a two-week high, which typically makes gold less appealing to international buyers.

This week, WTI and Brent are +2.05% and +1.45%, respectively. Oil prices remained stable on Wednesday as market participants assessed robust US gasoline demand data and renewed attacks on shipping in the Red Sea, while potential US copper tariffs heightened uncertainty.

Brent crude futures concluded the trading session with a modest increase of 13 cents, or +0.19%, settling at $70.13 per barrel. Similarly, WTI crude saw a slight rise of 7 cents, or +0.10%, closing at $68.25 per barrel.

According to the US Energy Information Administration (EIA) report released on Wednesday, US crude oil inventories experienced an increase last week, while gasoline and distillate stockpiles declined.

After a period of relative calm, attacks in the critical Red Sea global shipping lane have re-emerged over the past week. On Wednesday, rescue efforts successfully recovered six crew members from the Red Sea, though fifteen remain missing from the second of two vessels recently sunk in attacks claimed by Yemen's Iran-aligned Houthi militia.

Further support for oil prices stemmed from an EIA forecast issued on Tuesday, which indicated that US oil production in 2025 is anticipated to be lower than previously projected, as declining prices have led US producers to scale back their operations.

On Tuesday, the US President announced the intention to impose a 50% tariff on copper imports. This announcement coincided with the President's decision to extend the deadline for certain tariffs to 1st August, a move that has generated some hope among major trade partners regarding potential agreements to alleviate duties.

OPEC+ oil producers are poised for another substantial output increase for September. This aligns with the complete unwinding of voluntary production cuts by eight member countries and the United Arab Emirates' transition to a larger quota. On Saturday, OPEC+ had approved a supply increase of 548,000 barrels per day (bpd) for August.

EIA weekly report. US crude oil stockpiles experienced an unanticipated increase last week, while gasoline inventories saw a draw-down, driven by robust driving demand in anticipation of the 4th July holiday weekend.

According to the EIA report, crude inventories rose by 7.1 million barrels, reaching 426 million barrels in the week concluding 4th July. This increase encompassed a w/o/w adjustment figure of 1.8 bpd, which accounts for ‘unaccounted for crude oil’ and serves as a balancing item for the EIA's data.

Conversely, gasoline stocks registered a decrease of 2.7 million barrels during the same week, settling at 229.5 million barrels. This decline in gasoline inventories was accompanied by a 6% rise in gasoline demand, which reached 9.2 million bpd last week.

At Cushing, Oklahoma, the primary delivery hub for WTI crude, stockpiles increased by 464,000 barrels. Distillate stockpiles, encompassing both diesel and heating oil, also saw a reduction, falling by 825,000 barrels to 102.8 million barrels for the week.

Refinery crude runs declined by 99,000 bpd, and refinery utilisation rates experienced a slight decrease of 0.2 percentage points, reaching 94.7% of total capacity. Furthermore, net US crude imports decreased by 1.36 million bpd, as reported by the EIA.

Note: As of 5:00 pm EDT 9 July 2025

Key data to move markets

EUROPE

Thursday: German Harmonised Index of Consumer Prices and speeches by ECB Executive Board member Piero Cipollone and Bank of Spain Governor José Luis Escrivá.

Friday: French CPI and speeches by Bank of Italy Governor Fabio Panetta and ECB Executive Board member Piero Cipollone.

Monday: Eurogroup Meeting and German Bundesbank Monthly Report.

Tuesday: Econfin Meeting, Spanish Harmonised index of Consumer Prices, German ZEW Current Situation and Economic Sentiment Surveys, Eurozone Industrial Production and Eurozone ZEW Economic Sentiment Survey.

Wednesday: Italian CPI.

UK

Thursday: A speech by BoE Deputy Governor for Financial Stability Sarah Breeden.

Friday: GDP, Industrial Production and Manufacturing Production.

Monday: BRC Like-For-Like Retail Sales.

Tuesday: A speech by BoE Governor Andrew Bailey.

Wednesday: CPI, Core CPI and RPI.

USA

Thursday: Initial and Continuing Jobless Claims and speeches by St Louis Fed President Alberto Musalem, Federal Reserve Governor Christopher Waller, and San Francisco Fed President Mary Daley.

Friday: Monthly Budget Statement.

Tuesday: A speech by Dallas Fed President Lorie Logan, CPI and Core CPI, and NY Empire State Manufacturing Index.

Wednesday: PPI, Industrial Production. Fed’s Beige Book, and speeches by Cleveland Fed President Beth Hammack and New York Fed President John Williams.

CHINA

Monday: Imports, Exports and Trade Balance.

Tuesday: GDP, Industrial Production and Retail Sales.

JAPAN

Wednesday: Exports, Imports, Merchandise Trade Balance, and Adjusted Merchandise Trade Balance.

Global Macro Updates

Trump’s tariff war continues and the Fed remains cautious. On Monday, after firing off numerous letters to heads of several countries including Japan’s Prime Minister Shigeru Ishiba and South Korea’s President Lee Jae-myung, informing them of their new tariff rates, US President Donald Trump extended the deadline for the tariffs to go into effect from 9 July to 1 August. However, this delaying tactic was just, it seems, to force countries to the negotiating table. On Tuesday he announced a new 50% tariff on copper and said that at least two other sectors, including pharmaceuticals, were still under review and that more tariffs would be coming.

He had posted those earlier letters on his Truth Social media platform warning countries that they would face even higher tariffs if they retaliated by increasing their own import taxes. He has continued to increase the number of letters threatening new tariff rates on at least seven countries. Countries receiving the second batch of letters included the Philippines, Brunei, Moldova, Algeria, Iraq and Libya while Brazil, which had not previously been a target for tariff increases, has been hit with a 50% tariff. In a letter posted to his social media account, Trump said he was making the change “due in part to Brazil’s insidious attacks on Free Elections, and the fundamental Free Speech Rights of Americans.” As noted by Bloomberg news, the announcement came just days after Trump threatened to impose additional tariffs on members of the BRICS bloc of nations over its supposed “Anti-American policies” in the midst of the group’s leaders summit in Rio de Janeiro.

This renewed tariff attack came shortly before the Fed’s Open Market Committee (FOMC) released its minutes from its 17-18 June meeting. The Fed, whose chair Jerome Powell has been under increasing pressure from President Trump to cut rates, has been hesitant due to the uncertain effects these tariffs would have on inflation. The minutes revealed that although policymakers believed that the risks from tariffs had decreased compared to their meeting in May, there was a split in terms of the longer term impact of these tariffs. While some believed that the levies would only result in a one-off price increase, the majority of Fed policymakers warned that the tariffs would have persistent effects on inflation. Officials noted tariffs were likely to push up prices to some extent, but “there was considerable uncertainty about the timing, size, and duration of these effects”.The minutes stated, “Some participants noted that tariffs would only cause a temporary increase in prices and would not affect long-term inflation expectations, but most participants mentioned the risk that tariffs could have a more sustained impact.”

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Ten artykuł jest publikowany wyłącznie w celach informacyjnych i nie powinien być traktowany jako oferta lub zachęta do kupna lub sprzedaży jakichkolwiek inwestycji lub powiązanych usług, do których można się tu odwołać. Obrót instrumentami finansowymi wiąże się ze znacznym ryzykiem strat i może nie być odpowiedni dla wszystkich inwestorów. Wyniki osiągnięte w przeszłości nie są wiarygodnym wskaźnikiem wyników w przyszłości.

Zarejestruj się i otrzymuj informacje rynkowe

Zarejestruj się i otrzymuj

informacje

rynkowe

Subskrybuj teraz

Stworzone przez profesjonalistów. Dla profesjonalistów.