Another day, another deadline?

Key data to move markets today

EU: HCOB Spanish, Italian, French, German and eurozone HCOB Composite and Services PMIs, and eurozone Sentix Investor Confidence

UK: S&P Global Composite and Services PMIs

US: ADP Employment Change 4-week average, Durable Goods Orders, ex Defence, ex Transportation, Nondefence Capital Goods Orders ex Aircraft and speeches by Chicago Fed President Austan Golsbee, and Fed Governor Philip Jefferson

JAPAN: Labour Cash Earnings and Current Account

Global Macro Updates

No diplomatic off-ramp in Iran talks as Europe prepares for self-sufficiency in defence. Amid substantial headline activity Monday, there was little meaningful progress in ceasefire negotiations. Iranian officials have rejected a 45-day ceasefire proposal from the US, stating that Tehran will only accept a permanent cessation of hostilities with guarantees, echoing previous positions. On Monday, Iran rejected the US plan to end the conflict, issuing a 10-point counterproposal through Pakistan, as reported by Iran’s state news agency IRNA. The US President responded that Iran’s response fell short of the requirements for a cease-fire, yet acknowledged it as ‘a significant step’, but not ‘not good enough,’ according to Axios. The plan reportedly included guarantees for a permanent end to hostilities, reparations and protocols for shipping through the Strait of Hormuz.

On Monday, President Trump used public appearances to emphasise that negotiations are ongoing, expressing confidence in the good faith of the representatives involved. However, he reiterated his threat to begin attacking Iran's bridges and energy facilities starting Tuesday night at 8:00 PM Eastern Time, stating that the strikes could be largely completed by midnight. He underscored that reopening the Strait of Hormuz remains a priority, but conceded that ‘all you need is one terrorist’ to keep it closed. He also stressed that it is highly unlikely the deadline would be extended again.

The speech came after a previous statement in which he expressed that he was contemplating the possibility of withdrawing the US from NATO. Secretary of State Marco Rubio echoed this threat, despite having co-sponsored a 2024 law that requires Congressional approval for any withdrawal from NATO. Despite the remaining legal obstacles, it appears that financial markets are not waiting for constitutional clarity.

Analysts interpret the speech as bearish for risk assets in the near term, noting that no diplomatic resolution is evident, escalation options, including potential strikes on Iranian energy infrastructure, remain viable and a two-to-three week period of heightened military activity is anticipated. While a US exit from NATO is unlikely to pass Congress, it would compel Europe to rapidly increase defence spending and shift procurement decisively toward domestic platforms instead of US imports.

The investment thesis appears to be forming in real time, pushing Europe towards strategic self-sufficiency before it has fully developed the necessary agreements or architecture.

US Stock Indices

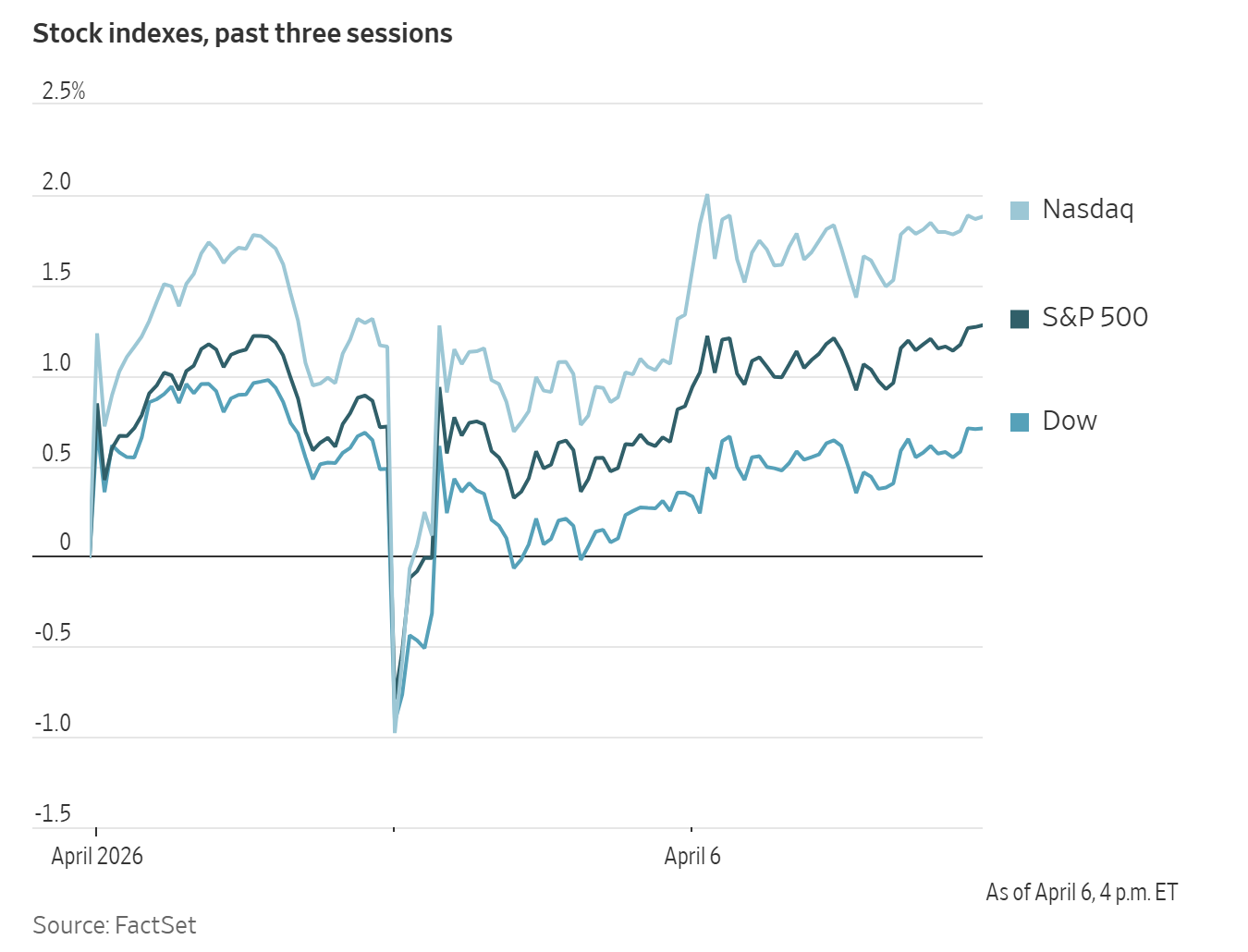

Dow Jones Industrial Average +0.36%

Nasdaq 100 +0.61%

S&P 500 +0.44%, with 8 of the 11 sectors of the S&P 500 up

On Monday, US equities continued to rebound, as investors awaited further clarification around the possibility of ceasefire or if greater escalation was most likely.

During the long Easter weekend, the Trump administration advocated for a possible 45-day cease-fire with Iran, while the US President maintained a tone of escalation on social media. The president declared that the US would target civilian infrastructure in Iran should an agreement to reopen the Strait of Hormuz not be reached by Tuesday evening.

The Dow Jones Industrial Average rose +0.36%, or 165.21 points, on Monday. The Nasdaq Composite was +0.54%, and the S&P 500 advanced +0.44%, with both indices recording their strongest four-day performance since last May.

In corporate news, Oracle appointed Hilary Maxson, formerly an executive at Schneider Electric, as its new CFO. Maxson’s leadership is expected to guide the company through extensive data centre expansion initiatives and address related liquidity challenges.

Neurocrine Biosciences has reached an agreement to acquire Soleno Therapeutics for $2.9 billion. This strategic acquisition will provide Neurocrine access to a treatment for a rare disorder characterised by uncontrollable hunger among patients.

Madison Air Solutions is preparing to raise up to $2.23 billion through its IPO, which could mark the largest US listing of an industrial company in nearly thirty years.

S&P 500 Best performing sector

Energy +0.77%, with APA +2.33%, Exxon Mobil +1.67% and EQT +1.17%

S&P 500 Worst performing sector

Utilities -0.42%, with NRG Energy -1.89%, Sempra -1.20% and Public Service Enterprise -0.94%

Mega Caps

Alphabet +1.09%, Amazon +1.44%, Apple +1.15%, Meta Platforms -0.25%, Microsoft -0.16%, Nvidia +0.14% and Tesla -2.15%

Information Technology

Best performer: VeriSign +5.64%

Worst performer: Super Micro Computer -5.04%

Materials and Mining

Best performer: Smurfit Westrock +2.09%

Worst performer: FMC -3.04%

European Stock Indices

CAC 40 -0.24%

DAX -0.56%

FTSE 100 +0.69%

Commodities

Gold spot -0.60% to $4,647.39 an ounce

Silver spot -0.27% to $72.79 an ounce

West Texas Intermediate +0.49% to $112.61 a barrel

Brent crude +0.58% to $109.69 a barrel

Gold prices declined on Monday, as investors exercised caution while awaiting further developments regarding the ongoing US-Iran conflict and the impending deadline for reopening the Strait of Hormuz.

Spot gold fell -0.60%, reaching $4,647.39 per ounce.

Spot silver also declined, dropping -0.27% to $72.79 per ounce.

Oil prices moved higher amid volatile trading on Monday, as tensions between the US and Iran intensified, even as indirect negotiations between the two nations offered hope for a possible de-escalation.

Brent crude futures rose to $109.69 per barrel, an increase of 63 cents, or +0.58%. US WTI crude futures settled at $112.61, up by 55 cents or +0.49%.

The US and Iran received a framework from Pakistan aimed at ending hostilities; however, Iran rejected the proposal to immediately reopen the strait, following the US President's warning of severe consequences should no agreement be reached by the end of Tuesday.

The Strait of Hormuz remains largely closed due to Iranian attacks on shipping following the US-Israel-led operations that began on 28 February.

Nonetheless, shipping data indicates that certain vessels, including an Omani-operated tanker, a French-owned container ship and a Japanese-owned gas carrier, have transited the strait since Thursday, reflecting Iran’s selective policy of permitting passage for ships from nations it considers friendly.

Iran reported that it has formulated its positions and demands in response to recent ceasefire proposals communicated through intermediaries.

Iran launched an attack on a 400,000-barrel-per-day (bpd) refining facility in Bahrain, causing a significant fire. Missile strikes also targeted the UAE port of Khor Fakkan.

Drone attacks hit facilities belonging to Kuwait Petroleum, resulting in fires at several locations.

Disruptions to Middle Eastern oil supplies have prompted refiners to seek alternative sources of crude, particularly for physical cargoes from the US and Britain’s North Sea. Spot premiums for US WTI crude have surged to record highs as Asian and European refiners compete for supply.

Indian refiners have also postponed scheduled maintenance shutdowns to help meet rising domestic fuel demand.

On Sunday, OPEC+ agreed to a modest increase in production of 206,000 bpd for May.

Saudi Arabia raised the official selling price for May Arab Light crude oil to Asia to a record premium of $19.50 per barrel above the Oman/Dubai average, marking an increase of $17 from the previous month, according to Aramco.

Recent disruptions to Russian oil supply, caused by Ukrainian drone attacks on Baltic Sea export terminals, impacted operations. Media reports indicate that the Ust-Luga terminal resumed loadings on Saturday following several days of interruptions.

Note: As of 4 pm EDT 6 April 2026

Currencies

EUR +0.03% to $1.1543

GBP +0.13% to $1.3235

Bitcoin +3.83% to $69,512.19

Ethereum +3.92% to $2,139.21

On Monday, the US dollar remained stable, while the Japanese yen hovered near the critical ¥160 per dollar threshold as investors assessed the intensifying conflict involving Iran. Market participants focussed closely on the latest deadline set by the US President regarding the reopening of the Strait of Hormuz.

The euro appreciated +0.03% to $1.1543, and the British pound rose +0.13% to $1.3235. The dollar index declined -0.05% to 99.98. Trading conditions were characterised by limited liquidity as many Asian and European markets were closed on Monday.

The Japanese yen fell -0.06% to ¥159.60 per US dollar, approaching the 21-month low recorded last week. Traders continue to monitor potential intervention by Japanese authorities following firm warnings issued by officials in recent days.

On Friday, Finance Minister Satsuki Katayama cautioned currency traders that the Japanese government is prepared to take action against speculative activity in the foreign exchange markets, noting that volatility has increased substantially.

Despite these warnings, there remains skepticism about the effectiveness of any intervention, particularly as geopolitical instability in the Middle East continues to drive strong demand for the safe-haven US dollar. Since the onset of the conflict, the yen has declined -2.27% against the US dollar.

Additionally, speculative traders have increased their short positions on the yen. The most recent weekly data indicates that short positions have reached $5.7 billion, the highest level since July 2024, when Japan previously intervened in the foreign exchange markets.

Fixed Income

US 10-year Bond +2.4 basis points to 4.344%

UK and European markets were closed in observance of Easter

On Monday, US Treasury securities registered modest gains as investors navigated a landscape marked by cautious optimism following reports of a potential ceasefire in the Middle East. Simultaneously, apprehension persisted due to President Donald Trump's warning of intensified military action against Iran should the critical Strait of Hormuz remain closed.

Trading activity was subdued, with thin volumes prevailing as several European and Asian markets were closed for the Easter holiday.

During afternoon trading, the yield on the 10-year Treasury note increased +2.4 bps to 4.344%.

At the shorter end of the yield curve, the two-year Treasury yield, which is closely tied to expectations for interest rate policy, rose +3.1 bps to 3.864%.

The yield on 30-year Treasury bonds declined -2.8 bps, settling at 4.890%.

The yield curve experienced a bear flattening, with the spread between two-year and 10-year Treasury yields narrowing to 48.0 bps from 48.7 bps observed late Thursday.

A robust US payrolls report for March, released last Friday, further solidified market expectations that the Fed will maintain interest rates at their current levels for an extended period.

Market participants are also closely monitoring economic indicators this week, including the release of the FOMC March policy meeting minutes on Wednesday, US Personal Consumption Expenditures (PCE) data on Thursday and the Consumer Price Index (CPI) on Friday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 0.5 bps of rate cuts in 2026, in contrast with the 2.8 bps of rate hikes priced in a week ago. Fed funds futures traders are now pricing in a 1.6% probability of a 25 bps rate hike at the 29 April FOMC meeting, compared to last week’s 2.1% probability.

Note: As of 4 pm EDT 6 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。